The investment philosophy developed by Peter Lynch has long served as a guide for investors seeking growing companies at reasonable prices. His methodology, detailed in One Up on Wall Street, emphasizes fundamental analysis and a long-term buy-and-hold approach. Lynch focused on identifying companies with sustainable earnings growth, strong financial health, and valuations that don't exceed their growth prospects. This strategy, often categorized as Growth at a Reasonable Price (GARP), avoids both speculative high-flyers and stagnant value traps, instead targeting businesses with consistent, measurable expansion.

Meeting Lynch's Growth Criteria

Fluor Corp (NYSE:FLR) demonstrates several characteristics that align with Peter Lynch's investment parameters. The company's historical earnings growth particularly stands out when evaluated against Lynch's requirements for sustainable, measurable expansion.

The engineering and construction firm shows strong fundamental metrics:

- EPS Growth (5-Year): 27.7% annually, exceeding Lynch's 15% minimum threshold

- PEG Ratio: 0.78, well below Lynch's maximum of 1.0

- Debt/Equity Ratio: 0.18, significantly better than Lynch's preferred 0.25 maximum

- Current Ratio: 1.62, indicating strong short-term financial health

- Return on Equity: 69.5%, far surpassing the 15% minimum requirement

These metrics reflect Lynch's emphasis on companies that grow at a sustainable pace rather than explosive but potentially unstable rates. The PEG ratio below 1.0 suggests the market may be undervaluing Fluor's growth prospects relative to its earnings multiple, a key Lynch valuation indicator.

Financial Health and Profitability

Fluor's balance sheet strength aligns with Lynch's preference for financially secure companies. The minimal debt-to-equity ratio of 0.18 indicates the company operates with little financial leverage, reducing risk during economic downturns. This conservative financial structure allows Fluor to operate in the cyclical nature of the engineering and construction industry without excessive debt burdens.

The company's exceptional return on equity of 69.5% demonstrates efficient use of shareholder capital, far exceeding Lynch's 15% threshold. This high ROE, combined with a current ratio of 1.62, presents a picture of a company that maintains strong liquidity while generating substantial returns on invested capital. These characteristics are crucial for long-term investors seeking companies that can compound value over extended periods.

Valuation and Growth Prospects

From a valuation perspective, Fluor presents an interesting case for GARP investors. While the company's P/E ratio of 21.50 might appear elevated in isolation, the PEG ratio of 0.78 tells a different story. This metric, which Lynch heavily emphasized, compares the price/earnings multiple to the company's growth rate. A reading below 1.0 typically indicates potential undervaluation relative to growth prospects.

The company's diversified operations across energy solutions, urban infrastructure, and government contracts provide multiple growth drivers. This business diversity helps mitigate sector-specific risks while maintaining exposure to long-term infrastructure spending trends. For Lynch-style investors, this operational breadth supports the case for sustainable growth rather than dependency on a single market segment.

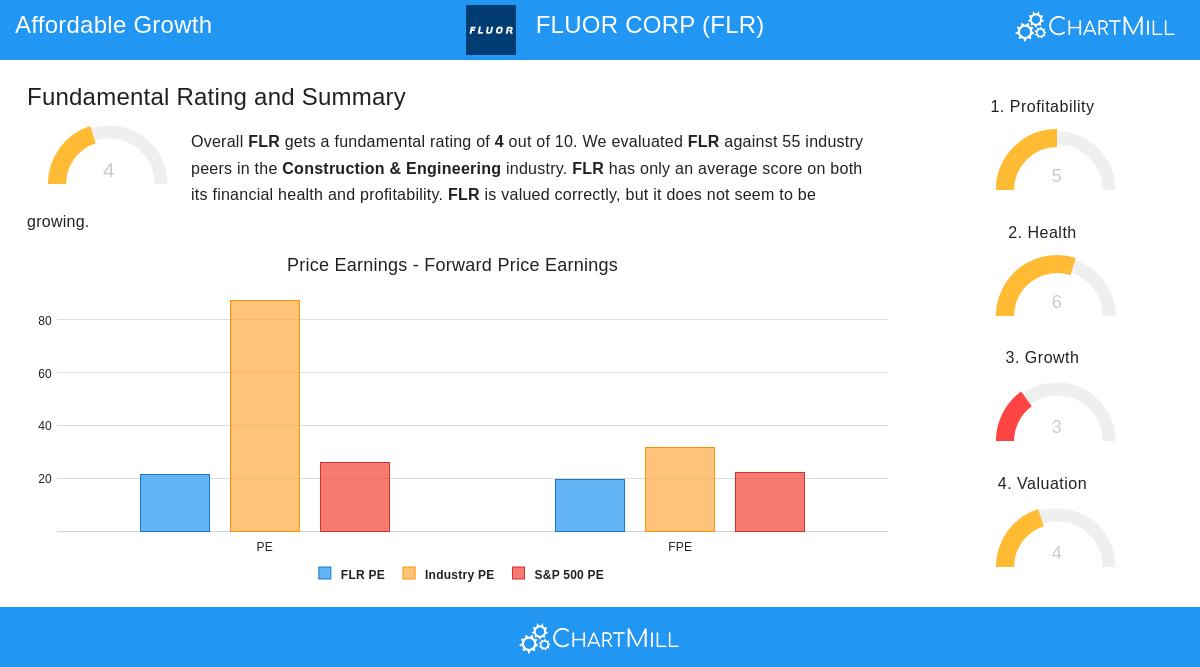

Fundamental Assessment Overview

According to ChartMill's detailed fundamental analysis, Fluor receives an overall rating of 4 out of 10. The analysis highlights several strengths including exceptional return metrics compared to industry peers, strong solvency ratios, and improving operational margins. However, the report also notes challenges in recent earnings performance and mixed growth indicators.

The fundamental assessment reveals a company with solid financial foundations but facing some headwinds in consistent growth execution. This mixed picture is not uncommon for companies in cyclical industries, and for long-term investors following Lynch's philosophy, such periods can sometimes present opportunities when the underlying business strength remains intact.

Investment Considerations

For investors employing Lynch's methodology, Fluor represents the type of established, financially sound company that can form the foundation of a long-term portfolio. The company's reasonable valuation relative to its growth history, combined with strong balance sheet metrics, aligns well with the GARP approach. Lynch often emphasized that investors should understand the businesses they own, and Fluor's straightforward engineering and construction services fit this requirement of operational transparency.

While past performance doesn't guarantee future results, the company's historical growth combined with current valuation metrics suggests potential for patient investors. The Lynch strategy specifically avoids timing market movements, instead focusing on business quality and reasonable valuation, both areas where Fluor shows promising characteristics.

Investors interested in discovering additional companies that meet Peter Lynch's investment criteria can explore the complete screening results for further research opportunities.

Disclaimer: This article presents factual information and analysis for educational purposes only and should not be construed as investment advice, recommendation, or endorsement of any security. Investors should conduct their own research and consult with financial advisors before making investment decisions. Past performance does not guarantee future results.