The investment philosophy created by Peter Lynch focuses on finding companies that show solid, lasting growth while being traded at fair prices, a method often called Growth at a Reasonable Price (GARP). This method steers clear of the far ends of pure growth or deep value investing, instead concentrating on businesses with strong foundations that are not excessively promoted by the market. The process uses particular filters to locate companies with good earnings growth, stable financial condition, and appealing valuation measures, making them appropriate for long-term, buy-and-hold investment portfolios.

Meeting the Lynch Criteria

EQUINOR ASA-SPON ADR (NYSE:EQNR) appears as a candidate from a filter built on Peter Lynch's method. The company's financial data matches several important parameters that Lynch viewed as vital for long-term investment success.

- Sustainable Earnings Growth: The filter looks for a 5-year earnings per share (EPS) growth between 15% and 30%. Equinor's EPS has increased at an average yearly rate of 16.82% over this time. This is important to the Lynch process, as it aims for companies with a confirmed history of growth, but leaves out those with very high growth rates above 30% that are frequently not maintainable.

- Reasonable Valuation (PEG Ratio): A fundamental part of the method is the Price/Earnings to Growth (PEG) ratio, which should be less than or equal to 1. Equinor's PEG ratio, calculated from its past five-year growth, is an attractive 0.48. This shows that the stock's price is low compared to its historical earnings growth, a main indicator for Lynch that an investor is not paying too much for that growth.

- Strong Profitability (ROE): Lynch preferred companies that effectively produce profits from shareholder equity. Equinor's Return on Equity (ROE) of 19.60% easily passes the filter's 15% minimum, showing good management effectiveness and profitability.

- Solid Financial Health: The method highlights financial steadiness. Equinor satisfies two significant condition checks:

- Its Debt-to-Equity ratio of 0.58 is under the filter's limit of 0.6, showing a careful use of borrowed money and a reduced chance of financial trouble.

- A Current Ratio of 1.23 indicates the company has enough short-term resources to pay for its upcoming obligations, confirming operational reliability.

Fundamental Analysis Overview

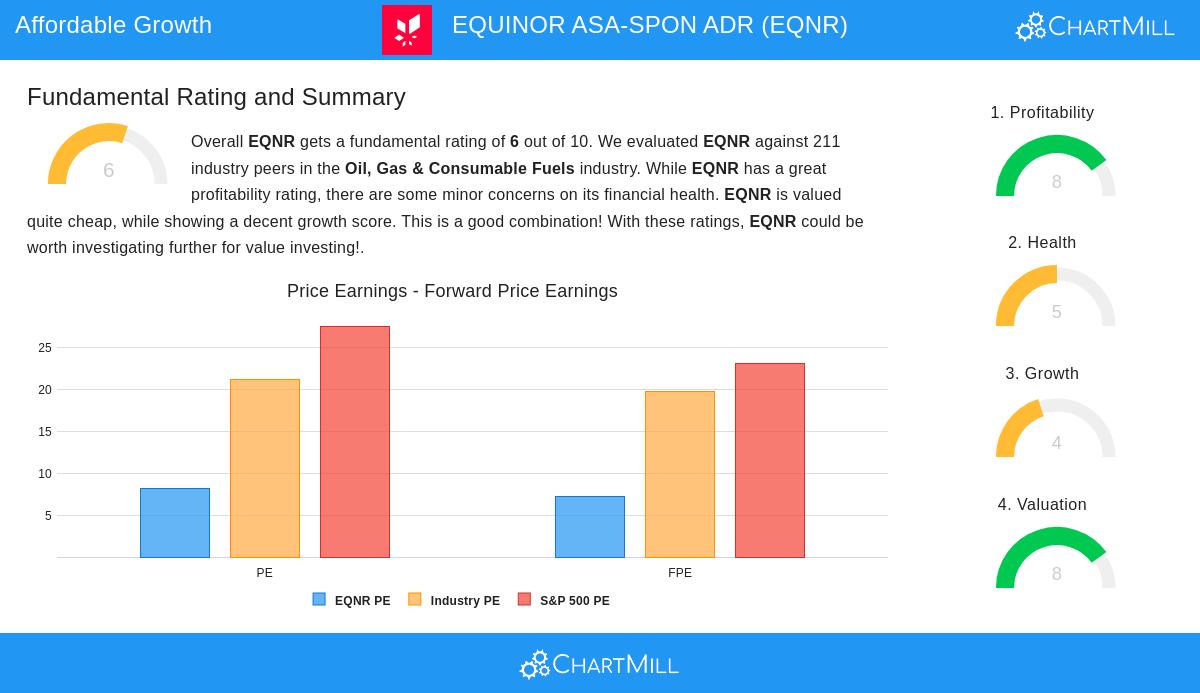

A full fundamental analysis report for Equinor gives it an overall score of 6 out of 10, pointing to a varied but mostly favorable situation. The company's biggest asset is in its profitability, where it gets an 8. It has very good returns on invested capital and equity, performing much better than most of its competitors in the Oil, Gas & Consumable Fuels industry. From a valuation standpoint, Equinor scores an 8, seeming inexpensive on a number of measures including P/E and Price/Forward Earnings ratios when looked at next to both the wider S&P 500 and its industry.

The analysis does mention some points to think about. The financial condition score is a neutral 5, with a Debt-to-Equity ratio that, while acceptable, shows some use of debt financing. The dividend, while appealing with a yield over 6%, has a sustainability score of 6 because of a high payout ratio. The growth score is a 4, showing a solid past EPS growth rate that is, however, predicted to slow down in the coming years along with an estimated small drop in revenue.

Investment Considerations for the Long Term

For an investor following the GARP philosophy, Equinor offers an attractive case. It is a well-known participant in the energy sector with a history of profitability and shareholder returns. Its valuation measures indicate it is not expensive, giving a safety buffer. The company's ventures into offshore wind and carbon capture fit with the worldwide shift in energy, possibly providing new long-term growth paths aside from its traditional hydrocarbon operations. While the expected decrease in growth and the high dividend payout are items to watch, the main financial figures of profitability, acceptable debt, and a good valuation relative to earnings growth align nicely with the structure of a long-term, Lynch-style investment.

For investors wanting to find other companies that match this systematic method, the Peter Lynch Strategy stock screen offers a changing list of possible candidates for more study.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The opinions expressed are based on current analysis and data, which are subject to change. Investors should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.