The investment philosophy made famous by well-known fund manager Peter Lynch centers on finding companies with good growth potential that are available at fair prices, a method frequently called Growth at a Reasonable Price (GARP). This method prioritizes steady business growth, solid financials, and earnings, while steering clear of highly promoted stocks with very high prices. By looking for firms with stable profit growth, healthy financial statements, and good value measures, investors aim to create a varied collection of sound businesses set up for lasting positive results.

Fitting the Lynch Standards

EOG RESOURCES INC (NYSE:EOG) displays a number of traits that match Peter Lynch's investment ideas. The company's basic measures meet important filter criteria that Lynch saw as necessary for finding good growth companies at fair costs.

The filter settings and EOG's matching numbers are:

- EPS Growth (5-Year): 18.45% compared to needed >15%

- PEG Ratio: 0.53 compared to needed ≤1

- Debt/Equity Ratio: 0.12 compared to needed <0.6

- Current Ratio: 1.79 compared to needed ≥1

- Return on Equity: 19.60% compared to needed >15%

These numbers reflect Lynch's focus on maintainable growth, fair pricing, financial soundness, and effective operations. The profit growth fits within Lynch's favored 15-30% band, showing an increase that is significant while still possibly maintainable. The low PEG ratio indicates the market might be pricing the company's growth potential low relative to its earnings multiple.

Financial Condition and Earnings

EOG Resources shows very good financial condition that fits with Lynch's attention to company steadiness. The basic analysis report gives EOG a health rating of 8 out of 10, putting it in the group of stronger participants in the Oil, Gas & Consumable Fuels field. The company's debt-to-equity ratio of 0.12 not only meets Lynch's basic condition but also does better than his stricter liking for ratios under 0.25. This careful financial setup lowers money risk and offers room to handle field cycles.

Earnings measures are especially strong, with EOG reaching:

- Return on Equity of 19.60%, above the 15% level

- Return on Invested Capital of 14.62%, doing better than 91.90% of field rivals

- Profit Margin of 25.22%, above 81.90% of competitors

- Operating Margin of 33.84%, placed with field front-runners

These solid earnings numbers point to effective operations and good use of capital, both traits Lynch considered important when judging management skill and business caliber.

Pricing Factors

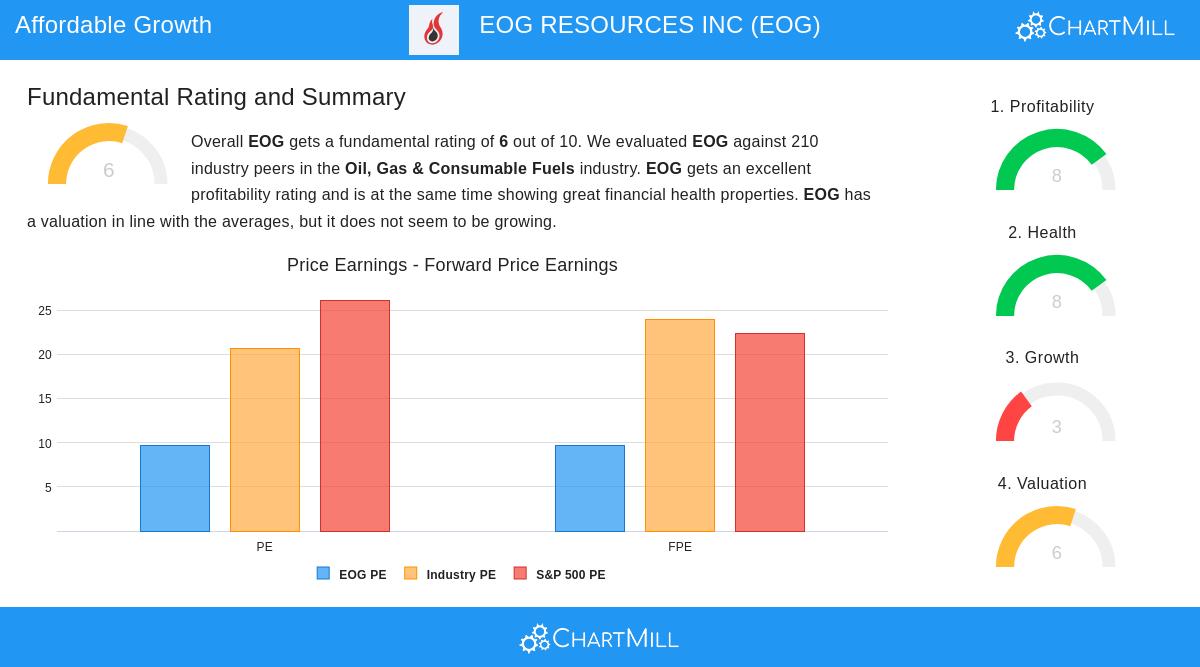

The pricing situation shows a varied but mostly positive picture for investors focused on value. EOG sells at a P/E ratio of 9.72, much lower than the S&P 500 average of 26.13 and less expensive than 80% of field rivals. This earnings multiple seems appealing considering the company's strong earnings and financial condition.

Still, the growth path deserves close watching. Recent results show a 13.37% drop in EPS over the last year and a 7.74% fall in income, although five-year averages stay positive. Future estimates point to moderate growth expectations, with analysts predicting about 6% yearly rises in both EPS and income. This slower growth view might account for the careful pricing multiples, possibly creating a chance if the company does better than predicted.

Dividend and Money Use

EOG's returns to shareholders show management's dedication to creating value, another Lynch focus. The company provides a 3.87% dividend yield with a notable 29.36% yearly increase rate over recent years. While the dividend growth has been faster than profit expansion, bringing up some questions about lastingness, the present payout ratio of 36.78% stays workable. The company has also lowered shares available through repurchases, matching Lynch's liking for companies that give capital back to shareholders.

Field Standing and Prospects

As a company focused on finding and producing oil and gas, mainly in U.S. areas including the Wolfcamp, Bone Spring, and Eagle Ford sites, EOG holds an important place in main energy regions. The company's large land holdings and operational knowledge provide a base for continued performance. While the energy field deals with change-related tests, EOG's financial control and operational effectiveness place it to handle field changes successfully.

View the full basic analysis report for a detailed review of EOG's financial numbers and field comparisons.

For investors wanting to find more companies that fit Peter Lynch's investment standards, look at the Peter Lynch filter to find other possible choices that match this established investment method.

Disclaimer: This review is for information only and is not investment guidance, a suggestion, or a support for any security. Investors should do their own study and talk with money advisors before making investment choices. Past results do not ensure future outcomes, and all investments have risk, including possible loss of the original amount invested.