The search for growth stocks at reasonable prices represents a cornerstone of disciplined investing. This approach, often called Growth At Reasonable Price (GARP) or affordable growth, seeks to identify companies demonstrating strong expansion potential without demanding excessive valuation premiums. By focusing on firms with solid growth trajectories, healthy financials, and attractive profitability, all while trading at sensible valuations, investors aim to participate in upside potential while mitigating the risk of overpaying for future expectations. One stock that recently surfaced through such a screening methodology is Dynatrace Inc (NYSE:DT).

Growth Trajectory

The core tenet of any affordable growth strategy is identifying companies with a demonstrable and sustainable growth path. Dynatrace exhibits this characteristic strongly, earning a high growth rating of 8 out of 10. The company's historical performance and future projections reveal a positive expansion story.

- Revenue Growth: Over the past year, revenue increased by 18.70%. More impressively, the average annual revenue growth over recent years stands at 25.49%.

- Earnings Per Share (EPS) Growth: EPS grew by 18.25% in the last year, with a significant 35.19% average annual growth rate over recent years.

- Future Expectations: Analysts project this momentum to continue, with EPS expected to grow by 17.62% and revenue by 15.30% on average annually in the coming years.

This solid and consistent growth across key financial metrics is precisely what investors look for in a GARP strategy, as it provides a fundamental basis for future share price appreciation.

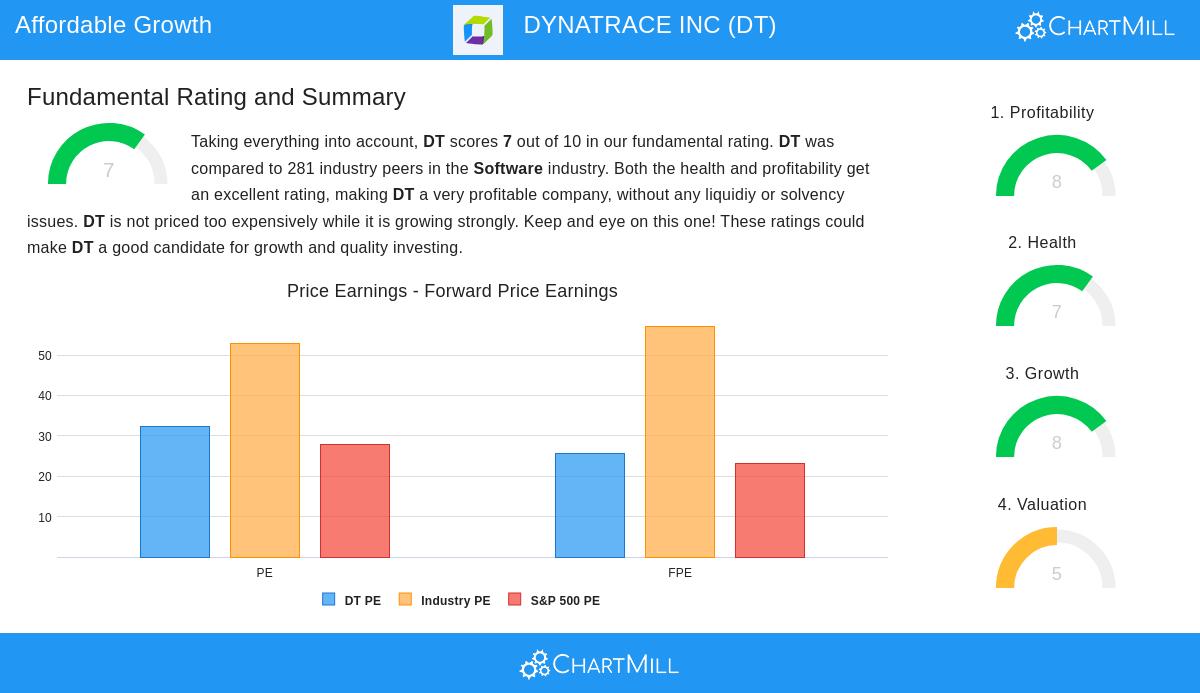

Valuation Assessment

A critical filter in an affordable growth screen is valuation, ensuring that the identified growth is not already fully priced into the stock. Dynatrace receives a valuation rating of 5, indicating a reasonable, if not outright cheap, price point relative to its prospects. The valuation picture is nuanced, blending premium metrics with relative value.

- The company's Price/Earnings (P/E) ratio of 32.30 is considered expensive in isolation but is cheaper than 65% of its software industry peers, whose average P/E is significantly higher.

- Similarly, its Price/Forward Earnings ratio of 25.58 is more favorable, placing it as cheaper than 67% of the industry.

- The PEG ratio, which adjusts the P/E for growth, suggests the current valuation is correct, indicating the growth rate may justify the earnings multiple.

- Positive comparisons are also seen in Enterprise Value/EBITDA and Price/Free Cash Flow ratios, where Dynatrace is more affordable than a majority of its competitors.

This balanced valuation is crucial for the strategy, as it suggests the market has not yet extrapolated the company's growth to an unsustainable degree, leaving potential room for multiple expansion or growth realization.

Profitability and Financial Health

While growth and value are the headline criteria, the affordable growth approach also demands a solid foundation of profitability and financial health to reduce investment risk. Dynatrace performs well in these areas, with a profitability rating of 8 and a health rating of 7. Strong profitability ensures that growth is of high quality and sustainable, while a healthy balance sheet provides resilience.

The company's profitability is supported by excellent margins and returns. Its Profit Margin of 27.75% and Gross Margin of 81.39% outperform the vast majority of the software industry. Furthermore, its Return on Equity of 18.27% and Return on Assets of 12.08% are also top-tier. From a financial health perspective, Dynatrace holds no debt, placing its solvency metrics among the best in its sector. Its Altman-Z score of 7.19 indicates a very low near-term risk of financial distress. These factors collectively provide a margin of safety, ensuring the company is well-positioned to fund its growth initiatives and weather economic downturns.

Conclusion

Dynatrace presents a strong case study for the affordable growth methodology. The company's notable and consistent growth in revenue and earnings forms the core of its investment appeal. This growth is not paired with a prohibitive valuation, as several key metrics show it trading at a reasonable, and in some cases, a discount, multiple relative to its industry. This combination is further strengthened by exceptional profitability and a solid, debt-free balance sheet. For investors seeking companies with strong expansion potential that are not priced for perfection, Dynatrace warrants closer examination. A more detailed fundamental analysis is available in the full Dynatrace fundamental report.

This analysis of Dynatrace was identified using a specific screening process for affordable growth stocks. Investors looking to discover other companies that fit similar criteria of strong growth, reasonable valuation, and sound fundamentals can explore more results through this Affordable Growth stock screen.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The information presented should not be used as the sole basis for making any investment decision. Investors should conduct their own independent research and consult with a qualified financial advisor before making any investment.