DORMAN PRODUCTS INC (NASDAQ:DORM) has been identified by a screening process based on Peter Lynch's investment methodology, which highlights finding companies with lasting growth paths trading at fair prices. Lynch's approach, described in his book One Up on Wall Street, centers on fundamental analysis instead of market timing, looking for businesses with good profitability, controlled debt, and earnings expansion that is strong and lasting, typically between 15% and 30% each year. This method matches what is frequently called GARP (Growth at a Reasonable Price) investing, combining parts of both growth and value strategies.

Alignment with Peter Lynch Criteria

Dorman Products satisfies a number of important filters from the Lynch-based screen, which are necessary for finding companies with lasting competitive benefits and financial soundness. These measures help confirm that expansion is not reached through too much risk or practices that cannot continue.

- EPS Growth (5-Year Average): 21.83% – This is inside Lynch's target of 15–30%, showing firm, controlled increase without the warnings of very fast growth that might be hard to keep up.

- PEG Ratio (Past 5 Years): 0.91 – Under the level of 1, this indicates the stock is fairly valued compared to its past earnings expansion, a key part of Lynch's valuation method.

- Debt-to-Equity Ratio: 0.31 – Much lower than the screen's top limit of 0.6 and even Lynch's favored 0.25, showing a careful capital structure with little financial risk.

- Current Ratio: 2.74 – Much higher than the least needed of 1, showing good short-term liquidity and capacity to meet responsibilities.

- Return on Equity: 16.14% – Above the 15% mark, showing effective use of equity and high profitability, both of which Lynch saw as important for long-term achievement.

Fundamental Health and Performance

Beyond the screen-specific measures, Dorman Products shows fundamental positives that back its fit for a GARP-focused portfolio. The company works in the automotive replacement parts area, supplying necessary parts across light-duty, heavy-duty, and specialty vehicle categories. This business model gains from steady demand, as vehicle upkeep and fixes are required for most owners.

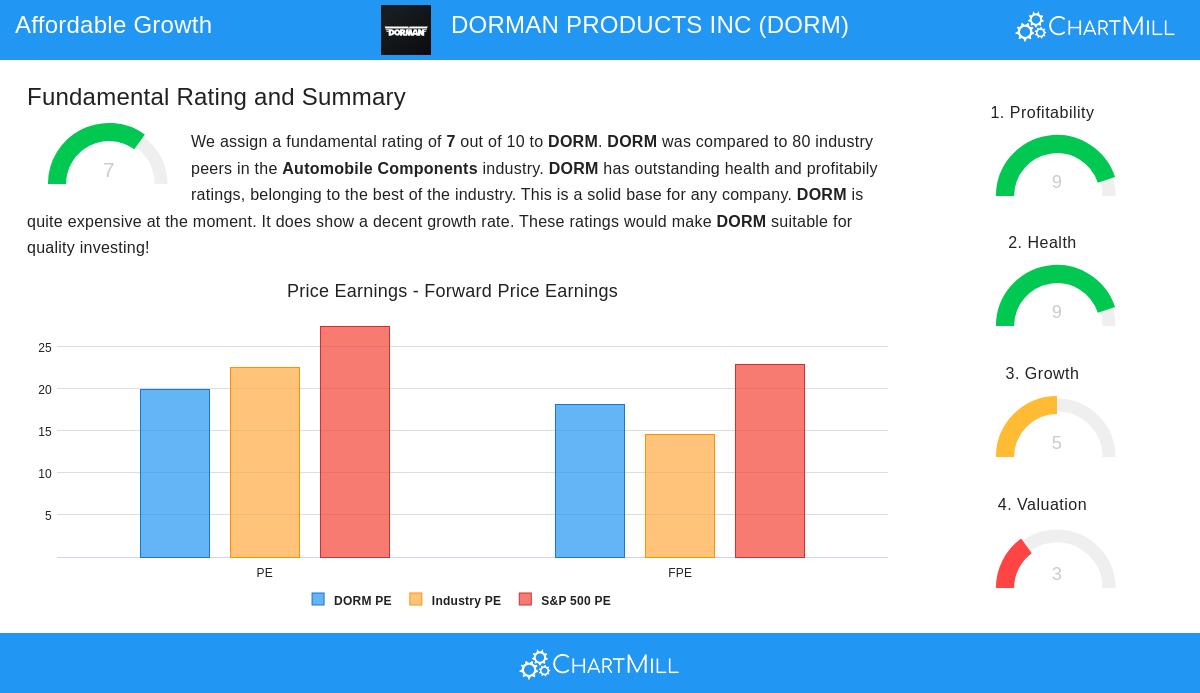

A detailed fundamental analysis scores Dorman well in profitability and financial soundness, with a rating of 7 out of 10 compared to industry competitors. Important features include very good margins, solid returns on invested capital, and a firm balance sheet with an Altman-Z score showing low bankruptcy risk. Even though the stock trades at a higher price on some valuation measures like P/E, this is partly reasonable due to its better profitability and growth profile.

Growth Prospects and Industry Position

Dorman’s strategic place within the automotive aftermarket industry gives a defensive growth nature, as need for replacement parts stays fairly constant even in economic declines. The company has shown its ability to increase revenue and earnings steadily over the last five years, and while future growth forecasts are more measured, they stay positive. This fits with Lynch’s liking for companies that are expanding regularly but not extremely, lowering the chance of a sudden drop.

Also, the company’s attention on product development and distribution effectiveness has let it gain market share and keep competitive margins. With good cash flow creation and a background of share buybacks, Dorman also matches Lynch’s regard for businesses that give value to shareholders through careful capital use.

Conclusion

Dorman Products presents a strong case for investors looking for growth at a fair price, as described by Peter Lynch’s measures. Its solid past performance, good financials, and fair valuation compared to growth make it a notable option for long-term portfolios. Investors using like strategies might find more ideas by reviewing the Peter Lynch screen, which often updates with companies meeting these factors.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consult with a financial advisor before making any investment decisions.