For investors looking for a disciplined, long-term way to build wealth, few strategies are as respected as Peter Lynch’s method. The famous manager of Fidelity’s Magellan Fund supported investing in what you understand, concentrating on companies with clear operations, lasting growth, and fair prices. His thinking, often called Growth at a Reasonable Price (GARP), stays away from speculation for sound basics. It stresses locating companies that are increasing earnings at a good rate but are not priced too high by the market, all while keeping a good financial position. A filter using Lynch’s main rules recently pointed to Dorman Products Inc (NASDAQ:DORM) as a possible name for more study.

A Match for the Lynch Method

Dorman Products works in the automotive aftermarket, providing replacement parts, fasteners, and improvements. This matches Lynch’s liking for clear, even ordinary, companies that sell needed products. The company operates in a consistent market, vehicles require maintenance and repair despite economic conditions, which fits the method’s attention to lasting, long-term business instead of temporary fads. For Lynch, the initial move is finding a logical company; the next is carefully examining the figures.

How Dorman Matches Important Lynch Rules:

- Lasting Earnings Growth: Lynch wanted companies increasing earnings per share (EPS) between 15% and 30% each year, quick enough to be interesting, but slow enough to be continued. Dorman’s five-year EPS growth rate of 21.8% falls inside this range, showing a record of good, but not excessive, increase.

- Fair Price (The PEG Ratio): Maybe the central part of the GARP method is the Price/Earnings to Growth (PEG) ratio. Lynch preferred a PEG of 1 or lower, meaning the stock price is fair compared to its earnings growth. Dorman’s PEG ratio, using its past five-year growth, is about 0.65, hinting the market might be pricing its growth path too low.

- Good Financial Condition: Lynch required companies with strong balance sheets.

- Debt/Equity Ratio: Dorman’s ratio of 0.28 is not only much below the filter’s limit of 0.6 but also matches Lynch’s own preference for a ratio under 0.25. This shows the company is mainly funded by ownership, not debt, lowering risk.

- Current Ratio: At 2.94, Dorman is well above the needed minimum of 1, showing it has enough cash to meet short-term bills.

- High Profitability (Return on Equity): A minimum ROE of 15% makes sure owner money is used well. Dorman’s ROE of 16.7% meets this mark, showing management’s skill at making profits from ownership.

Basic Condition Review

A wider basic analysis of Dorman supports the view from the Lynch filter. The company gets a good total score, with special high marks for profitability and financial condition.

- Profitability is a clear positive, with high scores for profit, operating, and gross margins. The company does better than most of its competitors in the Automobile Components industry on measures like Return on Assets and Return on Invested Capital.

- Financial condition is good. The company’s low debt amount and strong current ratio add to a sound money profile. Importantly, the analysis notes that Dorman has been lowering its count of outstanding shares, a positive signal Lynch specifically liked, as buybacks can raise per-share value.

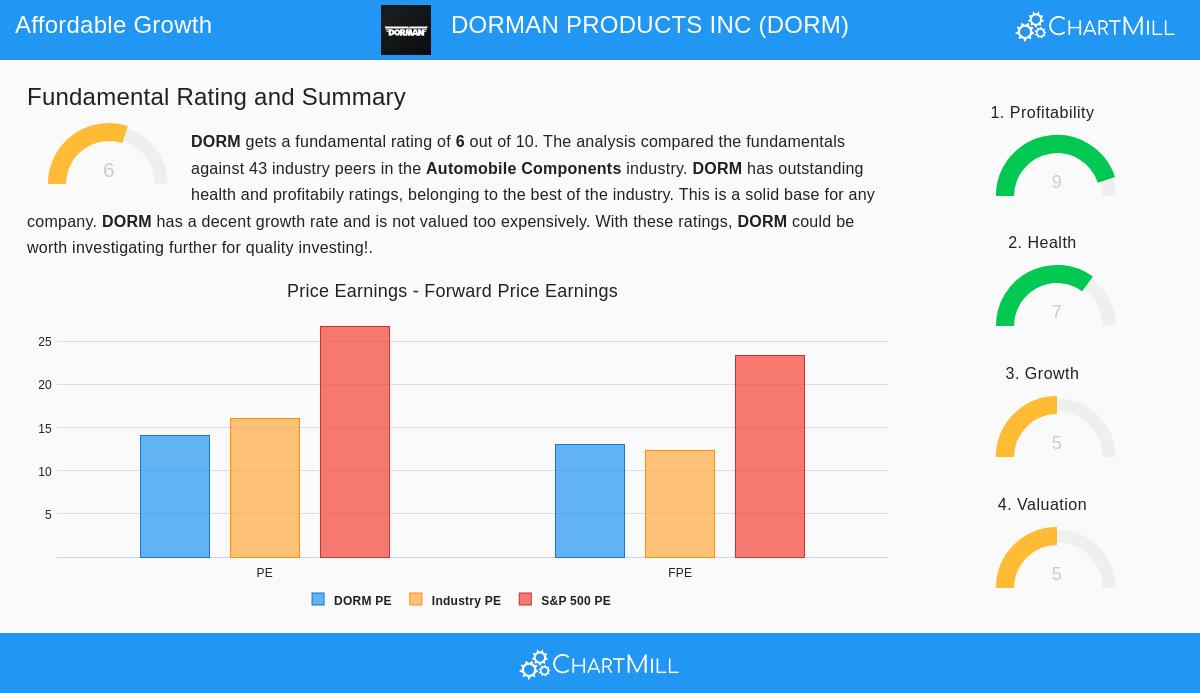

- Price looks fair. While the normal Price-to-Earnings ratio is similar to the industry, the analysis agrees that the PEG ratio suggests a rather low price. This payment for growth is key to the Lynch idea.

Points for the Long Term

While the Lynch filter shows interesting traits, it is a beginning for more detailed checking. The basic report states that Dorman’s future earnings and sales growth are expected to slow next to its good past results. This is not unusual as companies get older, but it highlights the need to judge whether the company can keep growing at an acceptable speed. Also, Dorman does not give a dividend, which might matter for some investors focused on income, though this is not a bad point in the pure Lynch method, which puts earnings growth and price gains first.

Looking for More

Dorman Products acts as a real case of how Peter Lynch’s ideas can find companies that mix growth with price and steadiness. For investors wanting to find other companies that pass this classic GARP check, you can see the present results of the Peter Lynch method filter here.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. The Peter Lynch method is one of many investment approaches, and past results of a filtering way do not promise future outcomes. Investors should do their own complete study and think about their personal money situation and risk comfort before making any investment choices.