Dorman Products Inc (NASDAQ:DORM) appears as a notable candidate for quality investors following the Caviar Cruise screening methodology, a systematic way to find companies with lasting competitive strengths, sound financial condition, and consistent growth potential. This strategy focuses on long-term ownership of businesses that show better operational efficiency, profitability, and capital use, instead of looking for short-term discounted chances. The framework highlights measurable numbers that show a company's capacity to increase revenue and earnings steadily, produce high returns on invested capital, keep low debt amounts compared to cash flow, and change accounting profits into real cash, all signs of enterprises made to endure economic shifts and build value over time.

Several important numbers place Dorman Products well within the Caviar Cruise standards. The company shows a notable EBIT growth rate of 22.59% over the last five years, much higher than the screen’s lowest requirement of 5%. This large growth in operating earnings points to not only increasing revenues but better operational efficiency and possible pricing strength, important qualities for quality companies trying to provide building returns. Also key is the firm’s return on invested capital (leaving out cash, goodwill, and intangibles), which is at 20.96%, above the 15% mark needed by the screen. A high ROIC means that management is efficiently using capital for projects that produce good returns, a central part of quality investing as it shows both operational strength and strategic care.

Debt management is another field where Dorman does very well, with a debt-to-free-cash-flow ratio of 3.31, easily under the screen’s highest point of 5. This shows that the company could pay off all its existing debt in a little more than three years using its present free cash flow, highlighting a solid balance sheet and lower financial risk. This kind of careful leverage is important for quality investors, as it offers strength during economic declines and freedom to seek growth chances without heavy dependence on outside funding. Also, Dorman’s five-year average profit quality, measured as free cash flow compared to net income, is at 84.08%, above the 75% minimum. This number shows the company’s capacity to change accounting earnings into real cash production, lowering the risk of earnings distortion and making sure that reported profits are supported by real liquidity.

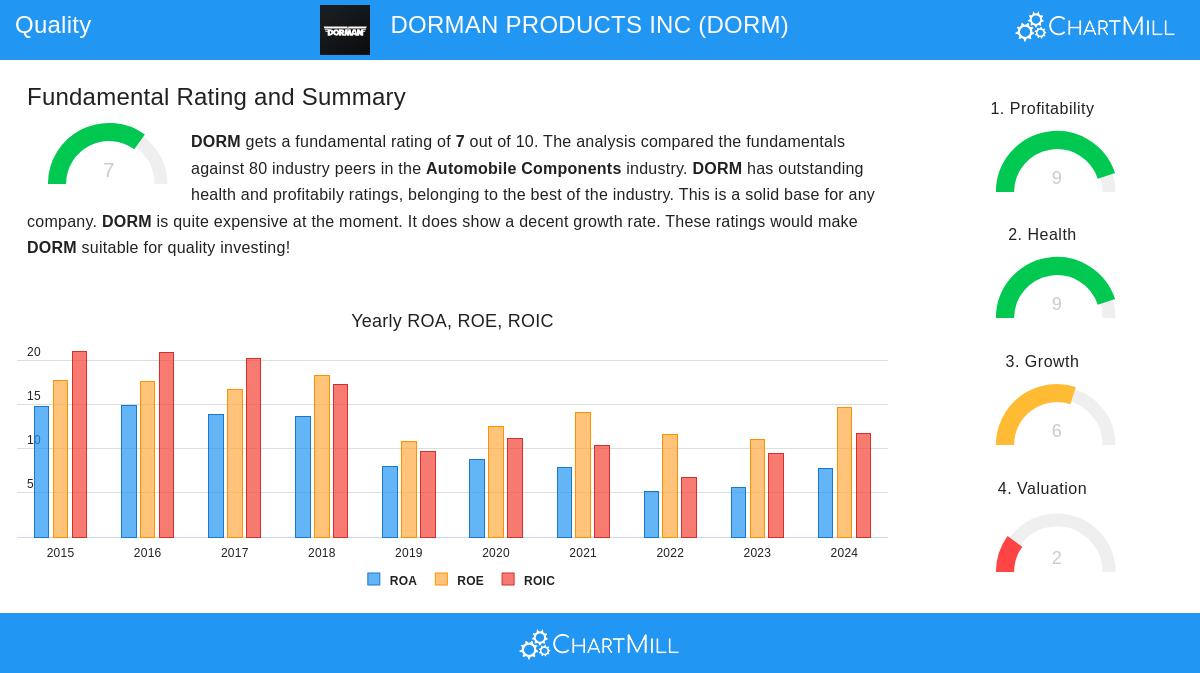

A look at the detailed fundamental analysis report further supports Dorman’s fit. The report gives the company a good rating of 7 out of 10, with especially high marks in profitability (9/10) and financial condition (9/10). Dorman does better than most industry competitors in key areas like profit margin (10.83%), operating margin (15.75%), and return on equity (16.14%). Its solvency and liquidity numbers are strong, featured by a good Altman-Z score and sound current ratio. While the valuation seems somewhat high compared to industry averages, a typical feature of high-quality businesses, the outstanding profitability and growth picture may support the premium for long-term investors concentrated on lasting compounders.

For investors wanting to look into other companies that satisfy the strict Caviar Cruise standards, the screen is available here, providing a selected list of possible quality investment candidates.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consider their financial objectives and risk tolerance before making any investment decisions.