Peter Lynch’s investment strategy, described in One Up on Wall Street, emphasizes finding companies with steady growth, fair prices, and strong financials, commonly known as the Growth at a Reasonable Price (GARP) method. This approach steers clear of overly popular, high-growth stocks, instead favoring businesses with reliable profits, manageable debt, and a strong position in their market. By looking for firms with a PEG ratio under 1, earnings growth between 15-30% over five years, and solid metrics like high return on equity (ROE) and low debt-to-equity (D/E) ratios, investors can find stocks that match Lynch’s ideas.

Dorman Products Inc (NASDAQ:DORM) stands out as a potential match for this strategy. The company, which provides automotive replacement and upgrade parts, works in the steady yet often ignored motor vehicle aftermarket sector, an area Lynch might appreciate for its consistent, repeat demand.

Why Dorman Products Matches the Lynch Approach

-

Consistent Earnings Growth

- Lynch liked companies with stable, but not extreme, earnings growth. Dorman’s EPS has increased by an average of 21.83% annually over the last five years, fitting within Lynch’s preferred 15-30% range. This shows the company is growing without taking on too much risk.

- Future EPS growth is estimated at 10%, suggesting a slower pace but still reflecting solid profitability.

-

Fair Valuation (PEG Ratio ≤ 1)

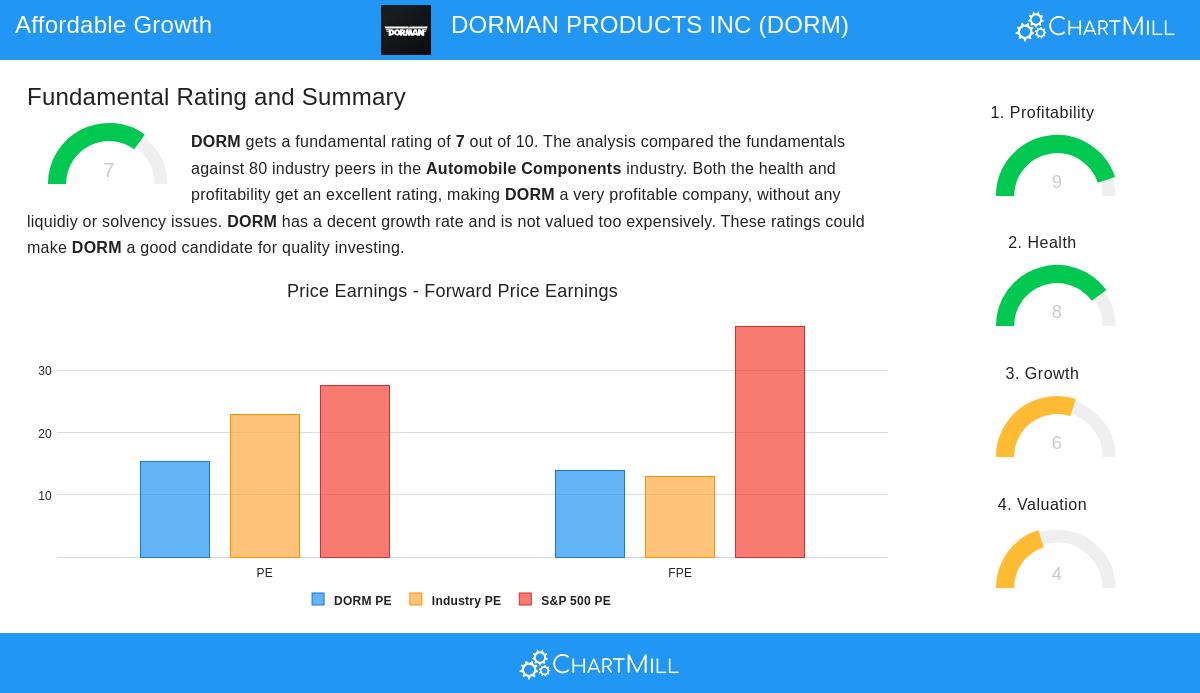

- A key Lynch measure, the PEG ratio (which accounts for growth when evaluating price), is 0.70 for Dorman, well under the 1 threshold. This indicates the stock may be priced below its growth potential.

- The company’s P/E of 15.37 is also lower than the S&P 500 average (27.61), reinforcing its reasonable price.

-

Solid Financial Condition

- Debt/Equity of 0.33: Lynch preferred firms with little debt, and Dorman’s ratio is below the screen’s 0.6 limit (and Lynch’s stricter sub-0.25 standard).

- Current Ratio of 2.62: This shows the company has enough liquidity to meet short-term needs, matching Lynch’s focus on stability.

- ROE of 16.05%: Above Lynch’s 15% target, this reflects effective use of shareholder funds.

-

Market Position

- Dorman’s focus on automotive aftermarket parts, a sector with steady demand, aligns with Lynch’s preference for reliable but unexciting industries. The company’s profit margins (10.48%) and operating margins (15.55%) rank among the best in its field, highlighting its efficiency.

Key Strengths in the Report

The full fundamental analysis gives Dorman a 7 out of 10, with high marks in profitability (9/10) and financial health (8/10). Main points:

- Strong profitability metrics: ROE, ROIC, and margins all beat industry averages.

- Better financials: Reduced debt, share repurchases, and steady free cash flow.

- Valuation: While slightly high on an EV/EBITDA basis compared to peers, the PEG ratio and earnings multiples suggest a fair price overall.

What Investors Should Consider

For those looking to find more stocks that fit Peter Lynch’s criteria, the screen results offer a list of companies with similar growth and value traits.

Disclaimer: This article is not investment advice. Do your own research or consult a financial advisor before making investment decisions.