DORMAN PRODUCTS INC (NASDAQ:DORM) has been identified as a potential candidate for quality investors based on the Caviar Cruise screening strategy. The company, which supplies automotive replacement and upgrade parts, demonstrates strong profitability, financial health, and efficient capital allocation—key traits sought by long-term investors.

Key Strengths

- High Return on Invested Capital (ROIC): DORM’s ROIC (excluding cash and goodwill) stands at 21.36%, well above the 15% threshold for quality stocks. This indicates efficient use of capital to generate profits.

- Strong EBIT Growth: The company has delivered a 22.59% annual EBIT growth over the past five years, reflecting improving operational efficiency.

- Healthy Debt Management: With a Debt-to-Free Cash Flow ratio of 2.42, DORM could repay its debt in under three years using current cash flows, signaling financial stability.

- Profit Quality: A five-year average Profit Quality of 84.08% shows that most net income is converted into free cash flow, a sign of reliable earnings.

Fundamental Analysis Summary

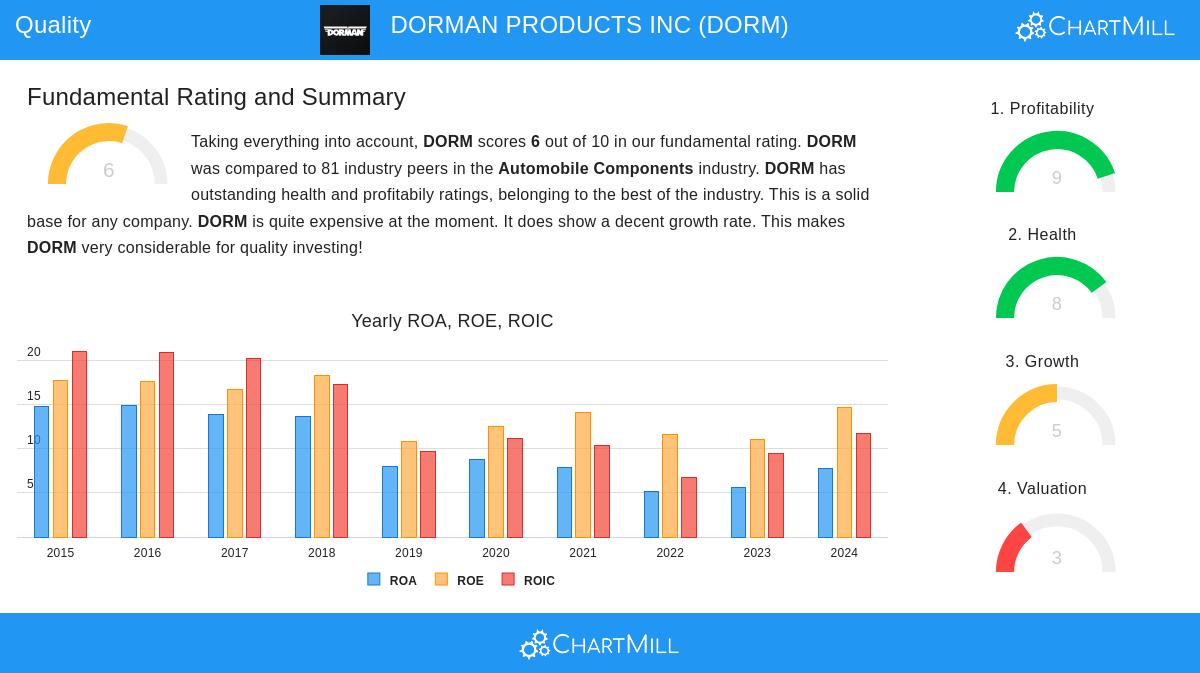

DORM scores 6 out of 10 in our fundamental rating, with standout performance in profitability and financial health. Key takeaways:

- Profitability (9/10): High margins (Operating Margin: 15.55%, Profit Margin: 10.48%) place DORM near the top of its industry.

- Financial Health (8/10): Solid liquidity (Current Ratio: 2.62) and manageable debt levels reduce bankruptcy risk.

- Valuation (3/10): While not cheap, DORM trades at a P/E of 16.31, slightly below the S&P 500 average, suggesting reasonable pricing for its quality.

Why Quality Investors Should Take Note

DORM’s consistent earnings growth, high ROIC, and strong cash flow generation align with the principles of quality investing. Its position in the automotive aftermarket—a stable industry—adds resilience.

For more quality stock ideas, explore our Caviar Cruise screener.

Disclaimer

This is not investment advice. Always conduct your own research before making investment decisions.