For investors looking for a systematic, long-term method to assemble a portfolio, few strategies are as respected as Peter Lynch’s. The famous leader of Fidelity’s Magellan Fund supported a "growth at a reasonable price" (GARP) idea, concentrating on firms with durable, steady expansion, good financial condition, and prices that do not overestimate that future promise. His system, explained in One Up on Wall Street, stresses basic examination instead of predicting market movements, urging investors to locate clear companies with good futures that are frequently missed by Wall Street. A filter using Lynch’s main principles lately highlighted Dorman Products Inc (NASDAQ:DORM) as a possible choice for more study.

A Business Plan Made for Consistent Need

Dorman Products works in the automotive aftermarket, providing replacement parts, fasteners, and improvement pieces. Based in Pennsylvania, the firm assists a varied client group through its Light Duty, Heavy Duty, and Specialty Vehicle divisions. This plan fits Lynch’s liking for clear companies in fundamental, if ordinary, fields. The need for vehicle repair and upkeep is fairly steady, offering a reliable base for lasting expansion despite economic changes. For an investor using Lynch’s style, this "ordinary" but required service is usually a good trait, indicating a business with a lasting advantage and foreseeable need.

Matching the Lynch Investment Standards

A Peter Lynch filter looks for companies that display a particular mix of expansion, earnings, and careful finance. Dorman Products seems to fit these strict needs according to the given information:

- Steady Earnings Expansion: Lynch wanted companies increasing earnings per share (EPS) between 15% and 30% each year over five years, thinking growth outside this band was either too little or unsteady. DORM states a five-year EPS expansion rate of 21.83%, putting it directly within Lynch’s preferred band. This shows a record of reliable, solid growth that is not too low or risky.

- Fair Price via PEG: To prevent overpaying for expansion, Lynch used the Price/Earnings to Growth (PEG) ratio, aiming for a figure of 1 or lower. A PEG under 1 implies the stock’s cost may not completely match its expansion path. DORM’s PEG ratio, using past five-year expansion, is 0.64, hinting the market could be pricing its historical expansion rate low compared to its present cost.

- High Earnings (ROE): A minimum Return on Equity (ROE) of 15% was a Lynch standard for finding well-run companies that produce good profits from owner investments. DORM’s ROE of 16.70% easily passes this mark, showing effective use of money and good earnings.

- Careful Financial Condition: Lynch favored companies with good balance sheets. Two main filters in the screen are a Debt-to-Equity figure under 0.6 and a Current Ratio over 1.

- DORM’s Debt-to-Equity figure of 0.28 is not only well under the screen’s ceiling but also matches Lynch’s own choice for a figure under 0.25. This shows very little use of debt funding.

- The company’s Current Ratio of 2.94 indicates good cash availability, showing it can readily meet its near-term duties, a mark of operational steadiness.

Top-Level Basic Evaluation

A wider view of Dorman’s basic condition supports the image shown by the Lynch filter. The company’s total basic rating is a good 7 out of 10. Its top qualities are in very high Earnings and Condition scores, where it places with the top in the Automobile Components field. Margins are solid and getting better, and the balance sheet is good with little chance of money trouble.

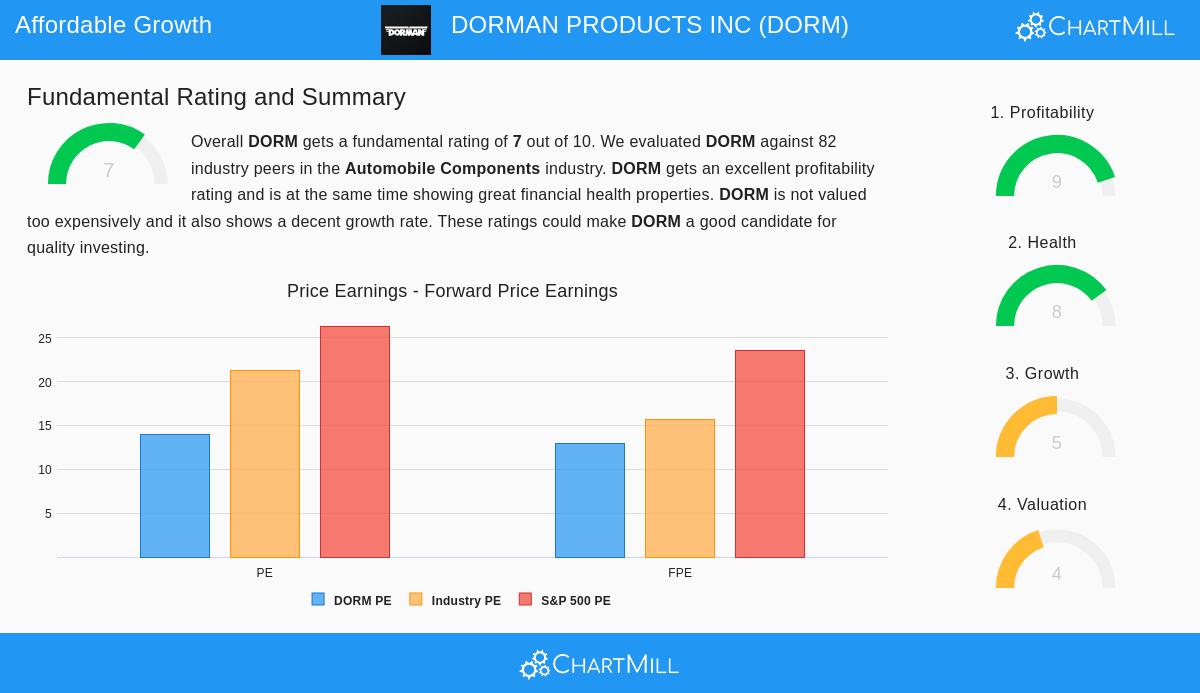

The Price view is varied but tends positive from a GARP angle. While some business value measures seem high next to field equals, the normal P/E figure of 14.01 is viewed as fair and is clearly lower than the wider S&P 500 average. This, paired with the low PEG ratio, backs the "reasonable price" point. The Expansion study confirms strong past results but notes that future expansion forecasts, while good, are expected to be more measured. For a Lynch investor, this change from very high to more steady expansion rates can be okay, if the price stays interesting. A full list of these scores is in the complete basic analysis report.

Is DORM a Lynch-Style Possibility?

Using the number-based filters of the Peter Lynch method, Dorman Products makes an interesting case for lasting investors. It shows a record of solid, steady earnings expansion, trades at a fair price when expansion is considered, and is built on a base of high earnings and a very strong balance sheet. The company works in a needed, clear field, which fits Lynch’s rule of investing in what you understand.

Still, as Lynch would state, a filter is only the first step for more study. Investors should examine the causes behind DORM’s past expansion, the competitive setting of the automotive aftermarket, and leadership’s plan for handling supply lines and technology changes in vehicles.

For investors wanting to review other companies that pass the Peter Lynch filter, you can locate the full, current list of outcomes here.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or a deal to buy or sell any security. All investments carry risk, including the possible loss of original money. Investors should do their own study and talk with a registered financial advisor before making any investment choices.