DORMAN PRODUCTS INC (NASDAQ:DORM) has been identified by our Peter Lynch-inspired stock screener as a potential candidate for long-term growth at a reasonable price (GARP) investors. The company, which supplies automotive replacement and upgrade parts, demonstrates solid financial health, profitability, and sustainable growth—key traits favored by Lynch’s investment philosophy.

Why DORM Fits the Peter Lynch Strategy

- Earnings Growth: DORM has delivered a five-year average EPS growth of 21.83%, comfortably within Lynch’s preferred range of 15% to 30%. This indicates steady, sustainable expansion rather than overheated growth.

- Reasonable Valuation: The stock’s PEG ratio (5Y) of 1.46 suggests it is fairly valued relative to its earnings growth, aligning with Lynch’s preference for PEG ratios below 1. While slightly above the ideal threshold, the company’s strong profitability may justify this premium.

- Strong Profitability: With a return on equity (ROE) of 16.05%, DORM outperforms most peers in the automobile components industry, reflecting efficient use of shareholder capital.

- Healthy Balance Sheet: A debt-to-equity ratio of 0.33 and a current ratio of 2.62 indicate financial stability, with ample liquidity to meet short-term obligations.

Fundamental Strengths

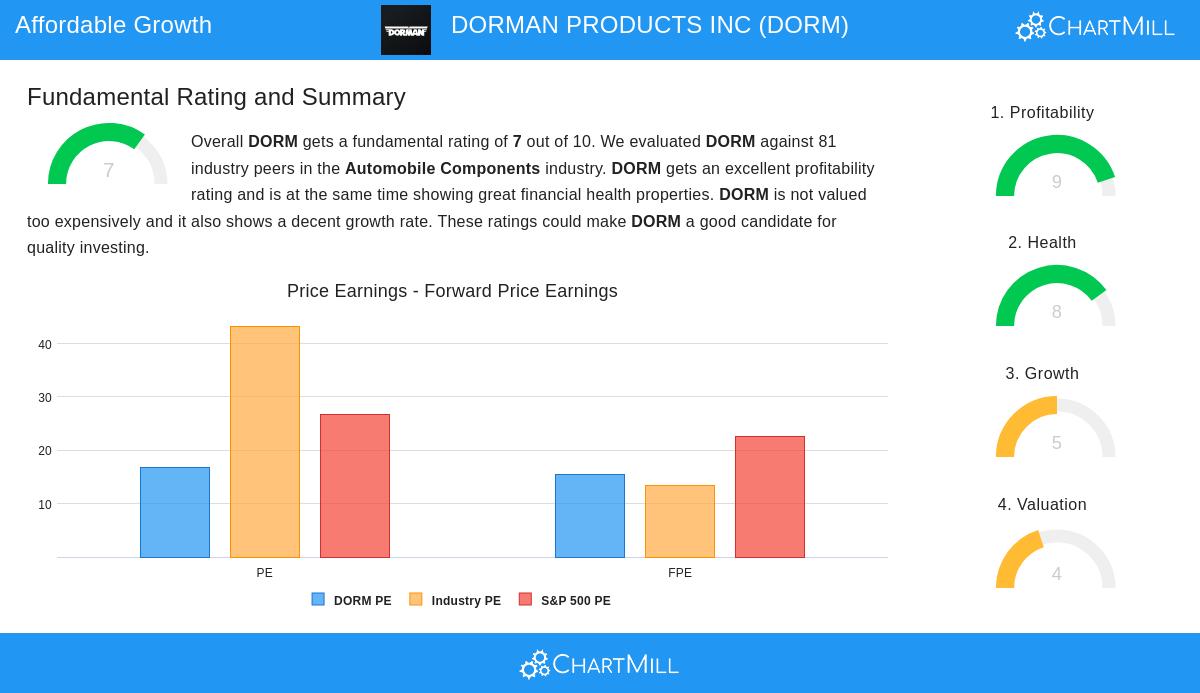

Our fundamental analysis report rates DORM a 7 out of 10, highlighting:

- High Profitability: The company boasts industry-leading margins, including a 10.48% net profit margin and 15.55% operating margin.

- Financial Health: DORM maintains a strong Altman-Z score of 4.62, signaling low bankruptcy risk, and has reduced its outstanding shares over time—a positive sign for shareholders.

- Growth Prospects: While revenue growth is expected to moderate, earnings are projected to grow at nearly 9.5% annually, supported by efficient capital allocation.

Final Thoughts

DORMAN PRODUCTS INC presents a compelling case for investors seeking a balance of growth and value. Its consistent earnings expansion, robust profitability, and prudent financial management make it a noteworthy candidate for long-term portfolios.

For more stocks that fit the Peter Lynch criteria, explore our Peter Lynch Strategy screener.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should always conduct your own analysis before making investment decisions.