The investment philosophy of Peter Lynch, the legendary manager of Fidelity's Magellan Fund, centers on identifying companies with strong growth prospects that are trading at reasonable valuations, a strategy often referred to as Growth at a Reasonable Price (GARP). Lynch emphasized sustainable growth, financial health, and understandable business models, favoring firms that an average investor could recognize and appreciate from everyday life. His approach combines elements of both growth and value investing, focusing on long-term holdings rather than short-term market timing.

Key Criteria and D.R. Horton’s Alignment

D.R. Horton Inc. (NYSE:DHI) emerges as a candidate that aligns well with Lynch’s strategy, based on a screen modeled after his principles. Here’s how DHI measures up against Lynch’s key metrics:

- Earnings Per Share Growth: Lynch sought companies with EPS growth between 15% and 30% over five years to ensure sustainable expansion. DHI’s five-year EPS growth stands at 27.63%, indicating strong, above-average growth that remains within Lynch’s preferred range, neither too sluggish nor dangerously high.

- PEG Ratio: A critical Lynch metric, the PEG ratio (P/E divided by growth rate) should be 1 or lower, signaling that the stock is reasonably priced relative to its growth. DHI’s PEG ratio of 0.52 suggests it is undervalued given its historical growth, a positive sign for GARP investors.

- Debt-to-Equity Ratio: Financial stability was paramount to Lynch, who preferred companies with low debt. DHI’s debt-to-equity ratio of 0.30 is not only below the screen’s threshold of 0.60 but also aligns with Lynch’s stricter preference for ratios under 0.25, reflecting a conservative capital structure.

- Current Ratio: Lynch valued liquidity, and DHI’s current ratio of 4.91 far exceeds the minimum requirement of 1, indicating strong short-term financial health and an ability to meet obligations comfortably.

- Return on Equity: Profitability is gauged through ROE, with Lynch targeting at least 15%. DHI’s ROE of 16.48% meets this criterion, showing effective use of shareholder equity to generate earnings.

Fundamental Health and Performance Overview

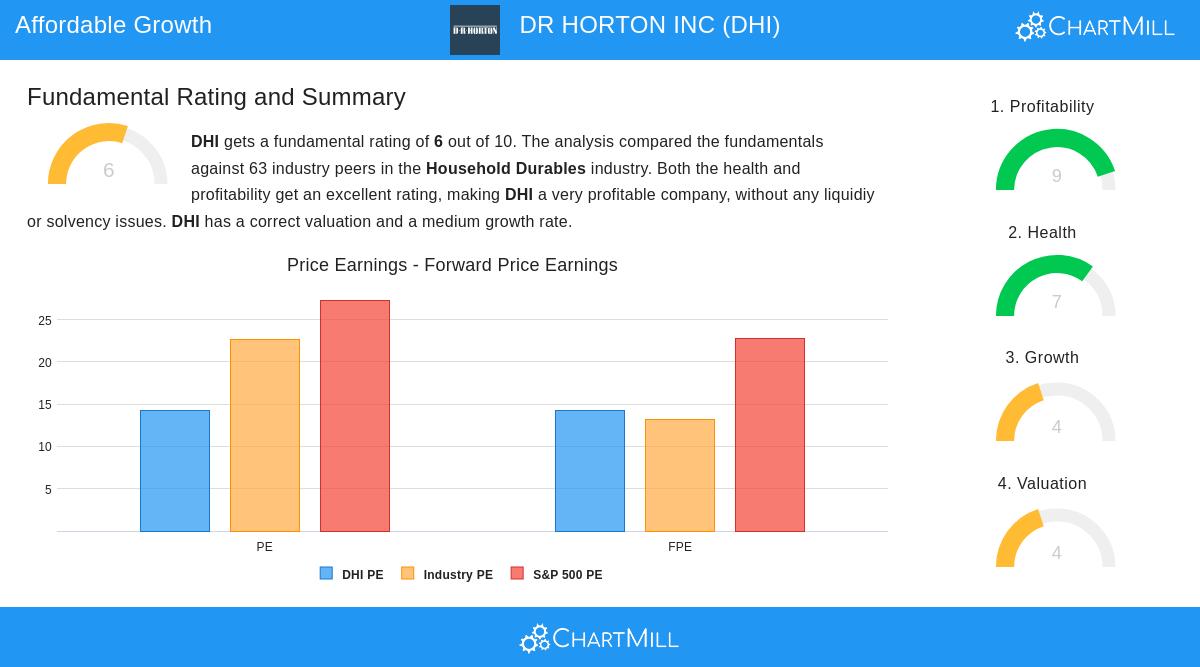

A deeper look into D.R. Horton’s fundamentals reinforces its appeal. The company holds a solid overall rating of 6 out of 10 in its industry, with particular strengths in profitability and financial health, areas Lynch prioritized. Its profit margins and returns on assets and invested capital rank among the top performers in the household durables sector. While recent earnings and revenue have seen some contraction, the long-term growth trajectory remains strong, and the company’s valuation metrics, such as P/E ratios, are reasonable compared to both industry peers and the broader S&P 500.

DHI also demonstrates disciplined capital management, with a history of share buybacks and a manageable dividend payout ratio. Its business model, focusing on single-family home construction, is straightforward and cyclical, yet DHI has maintained profitability and operational cash flow positivity over multiple years, fitting Lynch’s emphasis on durable, understandable enterprises. For a detailed breakdown, readers can review the full fundamental analysis report.

Contextual Considerations and Risks

Investors should note that homebuilding is sensitive to economic cycles, interest rates, and housing demand. DHI’s recent dip in yearly earnings and revenue reflects these broader pressures. However, its strong balance sheet, low debt, and consistent historical growth suggest resilience. Lynch might view such a company as a "stalwart", able to perform relatively well across cycles, and its current valuation could offer a reasonable entry point for long-term holders willing to endure sector volatility.

Conclusion

D.R. Horton represents a strong case for GARP investors following a Lynch-inspired strategy. It combines above-average growth with reasonable valuation, financial stability, and a clear business model. While not without cyclical risks, its fundamental strengths and alignment with key Lynch criteria make it a stock worth further research for those building a long-term, diversified portfolio.

For those interested in exploring other companies that match Peter Lynch’s investment criteria, you can view the full screen results here.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consider their financial situation and risk tolerance before making any investment decisions.