In the world of long-term investing, few strategies have demonstrated the enduring appeal and practical effectiveness of Peter Lynch’s approach, as detailed in his seminal work One Up on Wall Street. Lynch, who famously achieved a 29.2% average annual return while managing the Magellan Fund, advocated for a method that blends growth and value investing, often termed GARP, or Growth at a Reasonable Price. His philosophy centers on identifying companies with sustainable earnings growth, strong financial health, and reasonable valuations, all while emphasizing the importance of investing in businesses that are understandable and often overlooked by Wall Street. This strategy avoids speculative trends and market timing, focusing instead on fundamental strength and long-term potential.

D.R. Horton Inc. (NYSE:DHI) emerges as a noteworthy candidate when evaluated through the lens of Lynch’s criteria. As one of the largest homebuilders in the United States, the company operates in a sector that, while cyclical, is foundational to the economy, a characteristic Lynch might appreciate for its tangibility and relative predictability. The screening process based on his principles highlights several key metrics where DHI performs well, aligning closely with the strategy’s core requirements.

-

Earnings Growth and Sustainability: Lynch emphasized that earnings per share (EPS) should grow steadily but not at an unsustainable pace. DHI’s five-year EPS growth rate of 27.63% exceeds Lynch’s minimum threshold of 15%, reflecting strong historical performance. Although this is above his ideal upper bound of 30%, it is supported by a solid operational history and a diversified business model across homebuilding, rentals, and financial services. Importantly, analysts project future EPS growth at around 11.11%, indicating a moderation toward more sustainable levels, which Lynch would view favorably to avoid overextension.

-

Valuation Compensated for Growth: The PEG ratio, which adjusts the price-to-earnings ratio for growth, is a key part of Lynch’s approach to identifying reasonably priced growth stocks. With a PEG ratio of 0.50, well below the maximum threshold of 1, DHI appears undervalued relative to its growth trajectory. This suggests that the market may not be fully pricing in the company’s earnings potential, offering a margin of safety that Lynch considered critical for long-term investors.

-

Financial Health and Profitability: Lynch prioritized companies with strong balance sheets and high returns on equity. DHI’s debt-to-equity ratio of 0.30 is not only below the screen’s limit of 0.60 but also aligns with Lynch’s preference for ratios under 0.25, indicating conservative leverage and reduced financial risk. The current ratio of 4.91 far exceeds the required minimum of 1, demonstrating ample liquidity to meet short-term obligations. Additionally, the return on equity (ROE) of 16.48% surpasses the 15% benchmark, reflecting efficient use of shareholder capital and consistent profitability, a hallmark of Lynch’s ideal investments.

-

Business Model and Market Position: Beyond the numbers, Lynch encouraged investors to consider whether a company operates in a familiar, understandable industry with a durable competitive advantage. DHI’s focus on single-family homebuilding, complemented by its rental and financial services segments, fits this mold. The housing market’s long-term fundamentals, driven by demographic trends and urbanization, provide a tailwind that aligns with Lynch’s preference for businesses with enduring demand. Its scale and geographic diversification across 36 states further mitigate regional risks, supporting sustained growth.

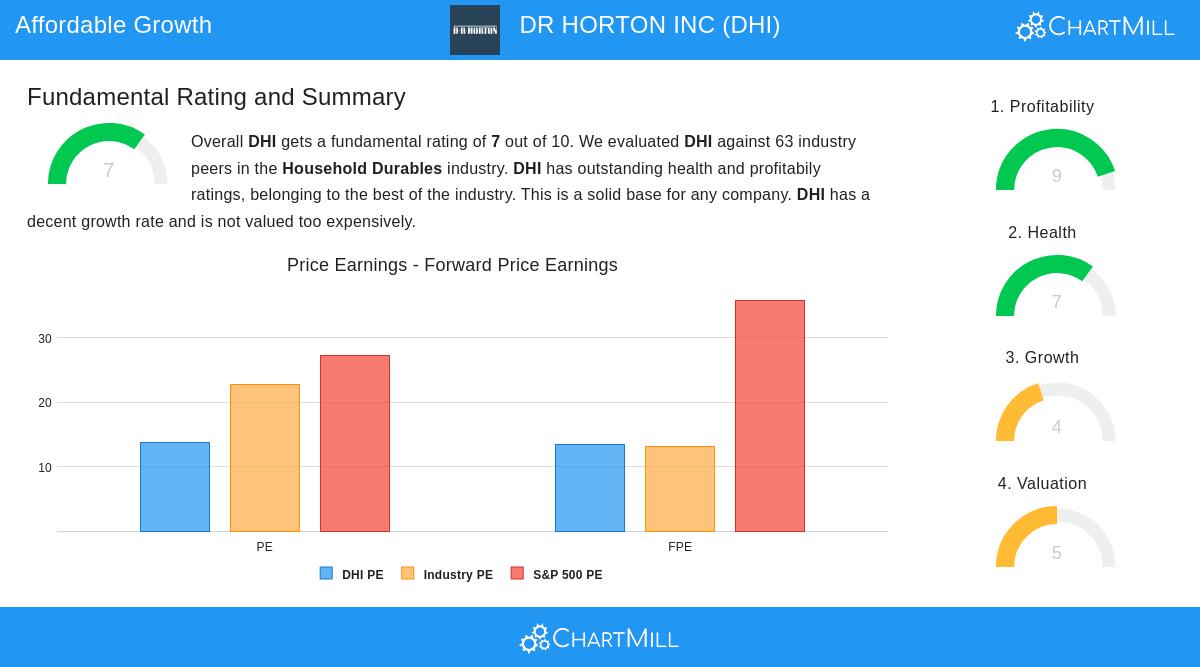

A review of DHI’s fundamental analysis report reinforces these observations, awarding the company an overall rating of 7 out of 10. The report highlights excellent profitability and health scores, with strong margins, high returns on invested capital, and a solid solvency profile. While recent earnings and revenue have faced short-term pressures, common in cyclical industries, the long-term growth trajectory and valuation metrics remain attractive. The company’s share buybacks and manageable dividend payout ratio also resonate with Lynch’s emphasis on shareholder-friendly practices.

For investors interested in exploring other companies that meet Peter Lynch’s criteria, the stock screener provides a dynamic list of potential candidates, updated regularly based on market conditions and fundamental data.

In summary, D.R. Horton represents a noteworthy example of a Lynch-style investment, a company with demonstrated growth, reasonable valuation, and financial resilience operating in a comprehensible industry. While no investment is without risk, particularly in sectors sensitive to economic cycles, the alignment with Lynch’s principles suggests a solid foundation for long-term investors seeking growth at a reasonable price.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consider their financial situation and risk tolerance before making any investment decisions.