Peter Lynch’s investment strategy, described in One Up on Wall Street, centers on finding companies with steady growth at fair prices, commonly known as the Growth at a Reasonable Price (GARP) method. The approach highlights key financial measures like earnings growth, profitability, and sound finances, steering clear of overpriced or heavily indebted businesses. By looking for firms with stable but not extreme growth, reasonable PEG ratios, and solid financial positions, investors can spot long-term opportunities that match Lynch’s ideas.

A company that fits this model is D.R. Horton Inc (NYSE:DHI), a top U.S. homebuilder. The stock aligns with many of Lynch’s criteria, making it worth considering for investors focused on GARP.

Why D.R. Horton Matches the Peter Lynch Approach

-

Consistent Earnings Growth

Lynch preferred firms with steady earnings growth, usually between 15% and 30%. DHI’s five-year EPS growth is 27.63%, fitting this range. While recent earnings have dropped (-16.25% YoY), the long-term trend stays positive, and analysts predict a recovery with 9.99% annual EPS growth ahead. -

Fair Valuation Based on PEG Ratio

A crucial measure in Lynch’s method is the PEG ratio (P/E divided by earnings growth), which should be below 1 to show the stock is priced fairly relative to growth. DHI’s PEG ratio of 0.41 suggests it trades at a notable discount to its historical growth rate, matching Lynch’s preference for reasonably valued growth stocks. -

Solid Profitability and Financial Strength

- Return on Equity (ROE) of 16.48% surpasses Lynch’s 15% benchmark, showing effective use of investor funds.

- Debt-to-Equity ratio of 0.30 is well under the screener’s 0.6 cap (and Lynch’s stricter sub-0.25 preference), reflecting a cautious financial approach.

- Current Ratio of 4.91 indicates strong liquidity to meet short-term needs, further supporting financial stability.

-

Leading Industry Position

DHI’s financials compare well with others in the Household Durables sector. Its profit margin (11.46%) and operating margin (15.48%) rank among the industry’s best, while its Altman-Z score (5.51) points to minimal bankruptcy risk.

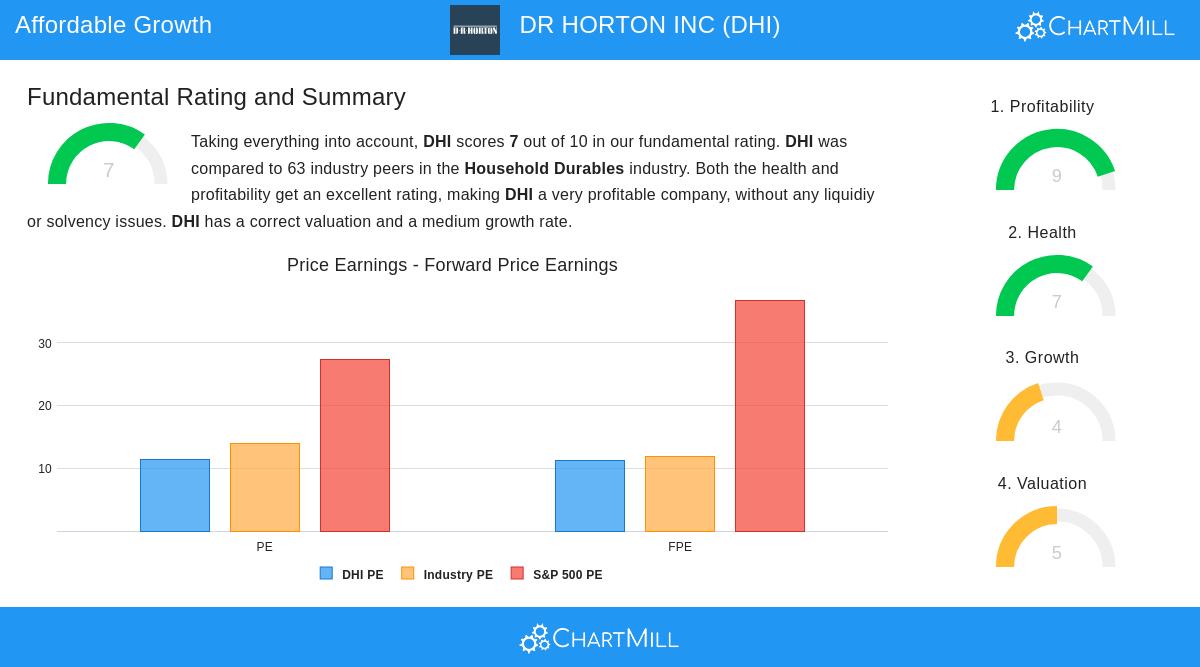

Fundamental Report Overview

Our full fundamental analysis gives DHI a 7/10 rating, emphasizing strengths in profitability and financial health. Key points include:

- Strong ROIC (12.73%) and reliable cash flow.

- Fair valuation with a P/E of 11.45, below the S&P 500 average (27.25).

- Growing dividends (14.84% CAGR over 10 years), though the yield (1.09%) is low.

Other Factors to Watch

While DHI’s recent revenue and EPS declines need attention, its long-term growth, careful financial management, and industry standing align with Lynch’s principles. Investors should also note:

- Limited institutional ownership (a Lynch positive) and ongoing share repurchases.

- Exposure to housing market cycles, which may require patience during slower periods.

For investors interested in more Peter Lynch-style picks, check our pre-built screen for additional options.

Disclaimer: This article is not investment advice. Do your own research or consult a financial advisor before making investment decisions.