There are days when the market reminds you it is not easily rattled, and Monday, March 2nd, was one of them.

Joint U.S. and Israeli strikes on Iran over the weekend - with reports that Supreme Leader Ayatollah Ali Khamenei had been killed - sent futures tumbling before the opening bell. By mid-morning, Wall Street looked like it was bracing for a storm. By the closing bell, the storm had largely passed.

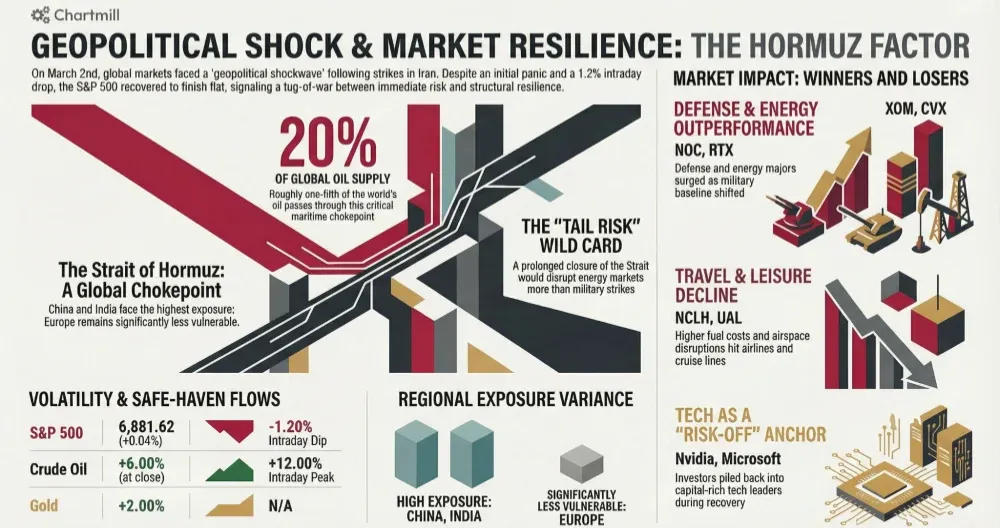

The S&P 500 SPX | +0.04% recovered all of its intraday decline of up to 1.2% to finish essentially flat at 6,881.62. The Nasdaq Composite COMP | +0.36% closed at 22,748.86, while the Dow Jones Industrial Average DJIA | -0.15% shed a modest 73 points to settle at 48,904.78. On its own, the closing snapshot looks almost boring. What happened in between was anything but.

A Geopolitical Shockwave

President Trump framed the military operation as "our last, best chance" to neutralize the threat posed by Iran, citing goals to destroy its missile and drone capabilities, neutralize its navy, and prevent nuclear armament. Markets, as they tend to do with geopolitical shocks, initially panicked and then reconsidered. That reconsidering was swift, triggered by a partial pullback in oil prices from their session highs and a flood of buyers into beaten-down tech names.

Still, I wouldn't dismiss the risk entirely.

Barclays analyst Ajay Rajadhyaksha sounded a note of caution that deserves attention: investors may have become too conditioned to rapid de-escalation cycles from prior Middle East flare-ups in 2024 and 2025. The situation remains fluid, reports of explosions in Dubai and Abu Dhabi fueled fears of a broader regional chain reaction, and the Strait of Hormuz remains blocked.

If that chokepoint stays closed for any meaningful length of time, the knock-on effects for energy and LNG markets could be far more disruptive than what we saw on Monday.

Oil, Energy & the Hormuz Wild Card

Crude oil initially surged as much as 12% intraday before cooling to around a 6% gain by session's end. Iran is OPEC's fourth-largest producer, and the closure of the Strait of Hormuz - through which roughly 20% of the world's oil supply passes - is the market's single biggest near-term tail risk.

China and India are the two countries most exposed to any prolonged disruption, with Europe far less so (only around 3% of Hormuz oil is destined for European shores).

There are some structural offsets worth noting. The UAE has a dedicated pipeline to the Gulf of Oman that bypasses the strait, while Saudi Arabia operates an east-west pipeline to the Red Sea.

Qatar, however, has no such escape valve for its LNG exports and it announced Monday it had temporarily halted gas production following a drone strike. That matters enormously for Asian energy markets.

To dampen fears of a supply crunch, OPEC+ announced a stronger-than-expected production increase: 206,000 barrels per day starting April 1, well above the 137,000 barrels the market had anticipated.

On the equity side, the energy majors were clear beneficiaries. ExxonMobil XOM | +1.13% and Chevron CVX | +1.52% both moved higher, while ConocoPhillips COP | +4.21% saw a more pronounced gain.

Tech Leads the Comeback

Once it became clear that the market wasn't heading into freefall, buyers piled back into technology.

Nvidia NVDA | +2.99% - whose chips power the AI infrastructure that investors remain structurally committed to - was a key engine of the recovery, adding nearly 3% to close at $181.41.

Microsoft MSFT | +1.48% settled at $396.21. Both companies are viewed as capital-rich enough to weather geopolitical turbulence, which makes them reliable anchors in a "risk-off" mood that doesn't fully commit to selling.

Palantir Technologies PLTR | +5.82% was the S&P 500's top performer, and the logic isn't hard to follow: the data analytics firm is deeply embedded with U.S. defense and intelligence agencies, as well as Israeli security services. When conflict escalates, Palantir's revenue outlook brightens almost by definition.

CrowdStrike CRWD | +3.46% also had a strong session, as elevated geopolitical risk tends to sharpen the appetite for cybersecurity spend.

Meanwhile, Nvidia made headlines beyond its stock price: the company announced a $2 billion investment in two optics-focused companies, Lumentum | LITE | +11.75% and Coherent COHR | +15.44%, as part of a multiyear partnership centered on advanced optics for AI infrastructure. Both stocks surged sharply on the news.

Defense Stocks: The Other Side of the Coin

It's not lost on anyone that for every airline that falls in a war scenario, a defense contractor rises.

Northrop Grumman NOC | +6.02%, maker of the B-2 Spirit stealth bomber and other advanced weapons systems, was one of the session's standout performers. RTX RTX | +4.71%, L3Harris LHX | +3.82%, and Lockheed Martin LMT | +2.83% all participated in the rally. In an environment where military escalation seems to be the new baseline, these names may continue to find support.

The flip side of that equation hit airlines and cruise lines hard. Higher fuel costs, disrupted Middle Eastern airspace, and weaker travel sentiment formed a triple headwind.

Norwegian Cruise Line NCLH | -10.53%, Carnival CCL | -7.64%, and Royal Caribbean RCL | -3.25% all saw steep declines, as did American Airlines AAL | -4.21%, United Airlines UAL | -2.91%, and Delta Air Lines DAL | -2.21%.

The Buffett Effect... and Its Limits

Perhaps the most symbolically striking decline of the day was Berkshire Hathaway BRK.B | -4.91%. In uncertain times, Berkshire has long been treated as a fortress, cash-rich, diversified, and with Warren Buffett's imprimatur as the ultimate backstop. Monday revealed something important: that protection was never really about the balance sheet alone. It was about Buffett himself.

The Q4 2025 update - Buffett's last as CEO - disappointed on multiple fronts.

Operating earnings came in at $10.2 billion, down more than 29% year-over-year, dragged lower by insurance underwriting profits that collapsed 54% to $1.56 billion. The conglomerate repurchased no shares.

New CEO Greg Abel's first shareholder letter was detailed and earnest, and he pledged to preserve Berkshire's culture of "financial conservatism and disciplined investing" in perpetuity, but investors wanted more. The lack of a dividend policy update and the still-limited investor communication left many underwhelmed.

As Bloomberg Intelligence analysts put it bluntly: investors are less forgiving of Abel than they were of his legendary predecessor. The market is essentially asking Abel to prove himself from day one, and Monday's 5% haircut was the opening bid in that negotiation. Capital generation in 2026 should remain solid, but the profit growth is expected to be modest at best. Worth monitoring closely.

Macro Undercurrents: Inflation Fears Resurface

Two U.S. manufacturing PMI readings for February both signaled a slowdown.

The ISM Manufacturing Index slipped to 52.4 from 52.6 in January, better than feared, but the S&P Global Manufacturing PMI told a more cautious story, declining from 52.4 to 51.6. S&P Global economist Chris Williamson noted it was the weakest growth reading since July 2025.

More worrying from a monetary policy standpoint: the ISM Manufacturing Prices Paid subindex jumped to 70.5, re-igniting inflation concerns.

The 10-year Treasury yield rose 9 basis points to 4.05%, reflecting that inflation expectations are back in the conversation. This complicates the Federal Reserve's path, higher energy prices from a Middle East conflict could feed into CPI, making rate cuts harder to justify even as growth softens. The dollar strengthened, pushing the euro back toward 1.17 from 1.18 on Friday.

Gold rose roughly 2% on safe-haven demand, while bitcoin added around 6% to trade near $69,000, an interesting combination that reflects both traditional and digital hedging impulses.

Strategy MSTR | +6.29%, the largest corporate bitcoin holder, gained in tandem after disclosing a fresh purchase of 3,015 BTC last week for $204.1 million.

Silver, for its part, bucked the safe-haven narrative, falling 5.5%, perhaps reflecting concerns about industrial demand given a weaker manufacturing outlook.

One to Watch: uniQure

Away from the geopolitical noise, gene therapy company uniQure QURE | -32.82% suffered one of the session's most brutal single-stock moves. The FDA deemed the company's clinical trial data for its Huntington's disease treatment insufficient, sending the stock into freefall.

My Take

Monday's session demonstrated something markets have done reliably for decades: they price bad news faster than most humans process it, then move on.

The recovery from over 1% intraday losses to near-flat is a testament to that muscle memory. But I'd caution against complacency. The Strait of Hormuz situation, the unresolved Qatar LNG exposure, and the slow creep of inflation back into the data all represent live wires.

Structurally, I continue to see defense, energy, and AI infrastructure as the sectors best positioned for what looks like an increasingly complex geopolitical backdrop.

For the portfolio: review your airline and cruise line exposure, keep an eye on Berkshire under Abel's watch, and don't ignore what rising energy prices could mean for the Fed's next move.

ChartMill Market Desk