Market Monitor News June 26 BMO (QuantumScape, BlackBerry UP - Torrid Holdings, General Mills DOWN)

By Kristoff De Turck - reviewed by Aldwin Keppens

Last update: Jun 26, 2025

S&P500 Inches Toward Record Highs

Despite a cocktail of headwinds - rate uncertainty, political tension, and the U.S. debt load - markets have shown remarkable resilience. The S&P500 is now less than 1% away from its all-time high of 6,144 points. That’s quite the statement after a bumpy first half of the year. The index didn’t move much on Wednesday, but the broader trend remains bullish.

While the Dow Jones slipped 0.3%, the Nasdaq managed a modest 0.3% gain, mostly thanks to Nvidia (NVDA | +4.33%) hitting a fresh high of $154.31. Investors continue to pile into anything AI-related, and Nvidia, the poster child of that craze, is still leading the charge.

According to strategists at JPMorgan Chase, we may well end 2025 with new records on the board, citing AI and tech as fundamental tailwinds. And frankly, with cash still flowing in on every dip, it’s hard to disagree.

Fed Caution, Trump Pressure, and Powell’s Tightrope Walk

Federal Reserve Chair Jerome Powell spent the last two days defending his stance in front of Congress. He’s being pressed hard by Donald Trump for rate cuts, but Powell isn’t biting. In fact, he made it clear that Trump’s aggressive new tariffs, especially on Chinese imports, pose a real inflation risk.

A one-time price bump? Maybe. But the potential for stickier inflation means no hasty rate cuts.

Of course, Trump is not taking this lightly. The Wall Street Journal reports he’s considering replacing Powell by September, even though his term runs through 2026. That move would shake Fed credibility, to say the least.

Markets, however, are now betting on faster rate cuts regardless. The dollar dipped 0.2% against the euro, hitting its lowest level since September 2021. The euro/dollar closed at 1.1663.

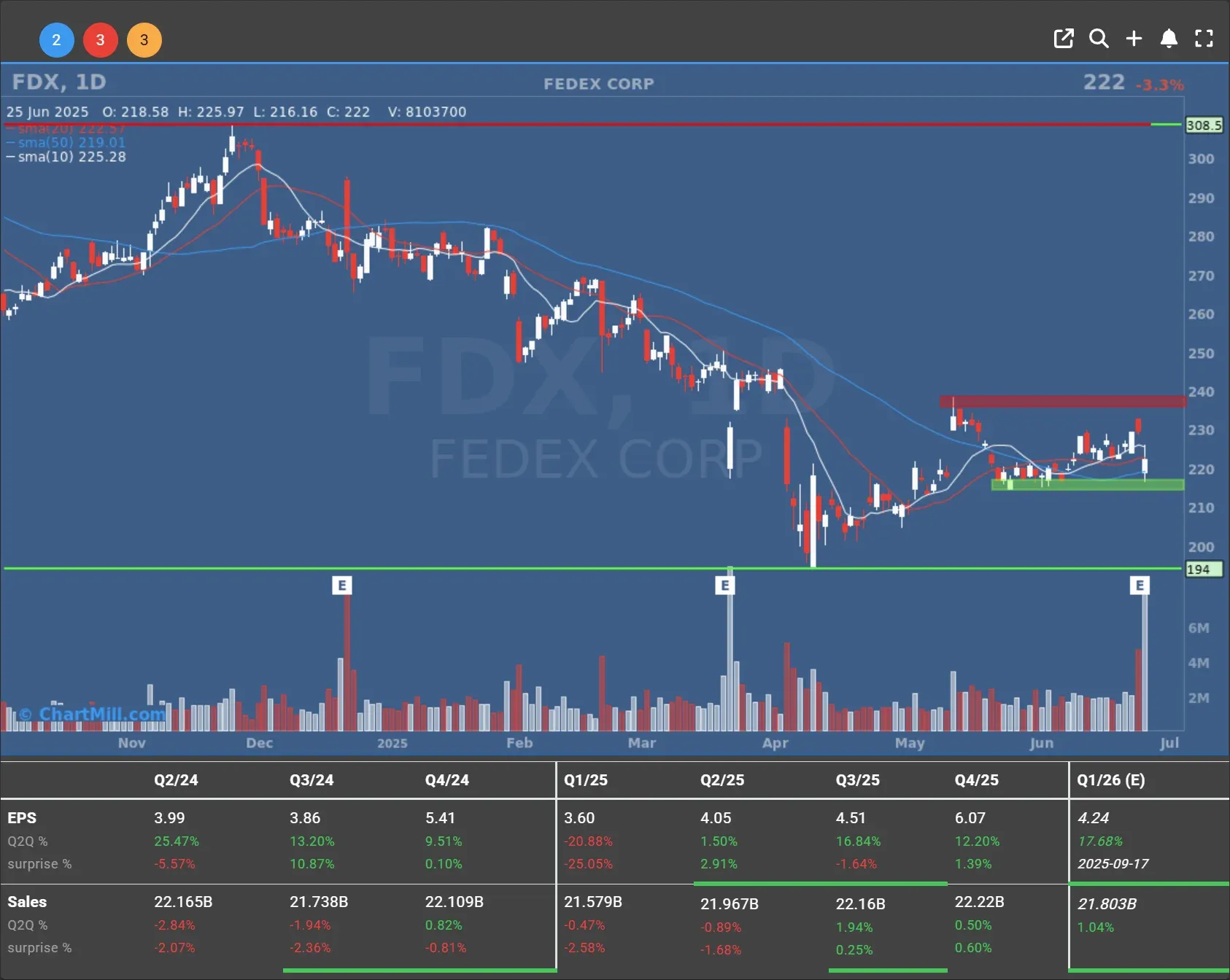

FedEx, General Mills and the Cost of Uncertainty

In the corporate trenches, FedEx (FDX | -3.27%) came under pressure. While Q4 earnings per share of $6.07 beat expectations, the outlook for Q1 was soft, $3.40 to $4.00 EPS and there’s now radio silence on full-year guidance.

A volatile demand environment and, let’s be honest, ongoing tariff drama, are to blame. Adding to the cloud: founder Fred Smith passed away over the weekend at age 80.

General Mills (GIS | -5.11%) also disappointed. The packaged food giant expects adjusted earnings to fall 10–15% this fiscal year, far worse than the 5% drop analysts had forecast.

CEO Jeff Harmening cited weak demand and rising marketing costs as consumers tighten their belts in an unpredictable macro landscape.

QuantumScape Steals the Show

There was, however, one stock that stole the spotlight: QuantumScape (QS | +30.95%). The solid-state battery pioneer said it hit a “major milestone” in development. These batteries promise better energy density, faster charging, and greater safety, basically everything the EV world dreams of. No wonder investors went wild.

This is one to keep on the radar. The shift to solid-state could be a game-changer if the tech scales.

A Fragile Macro Backdrop

Zooming out, macro data added some wrinkles. Sales of new single-family homes in the U.S. dropped 13.7% in May to 623,000, well below expectations. Still, mortgage applications were up slightly (+1.1%), so not all is doom and gloom.

Oil inched up 0.9% to $64.92 a barrel after the EIA reported another drawdown in crude inventories.

Meanwhile, geopolitical anxiety continues to simmer. The Israel-Iran ceasefire is holding, for now. Trump was busy at the NATO summit in The Hague, where member states committed to boosting defense spending to 5% of GDP by 2035.

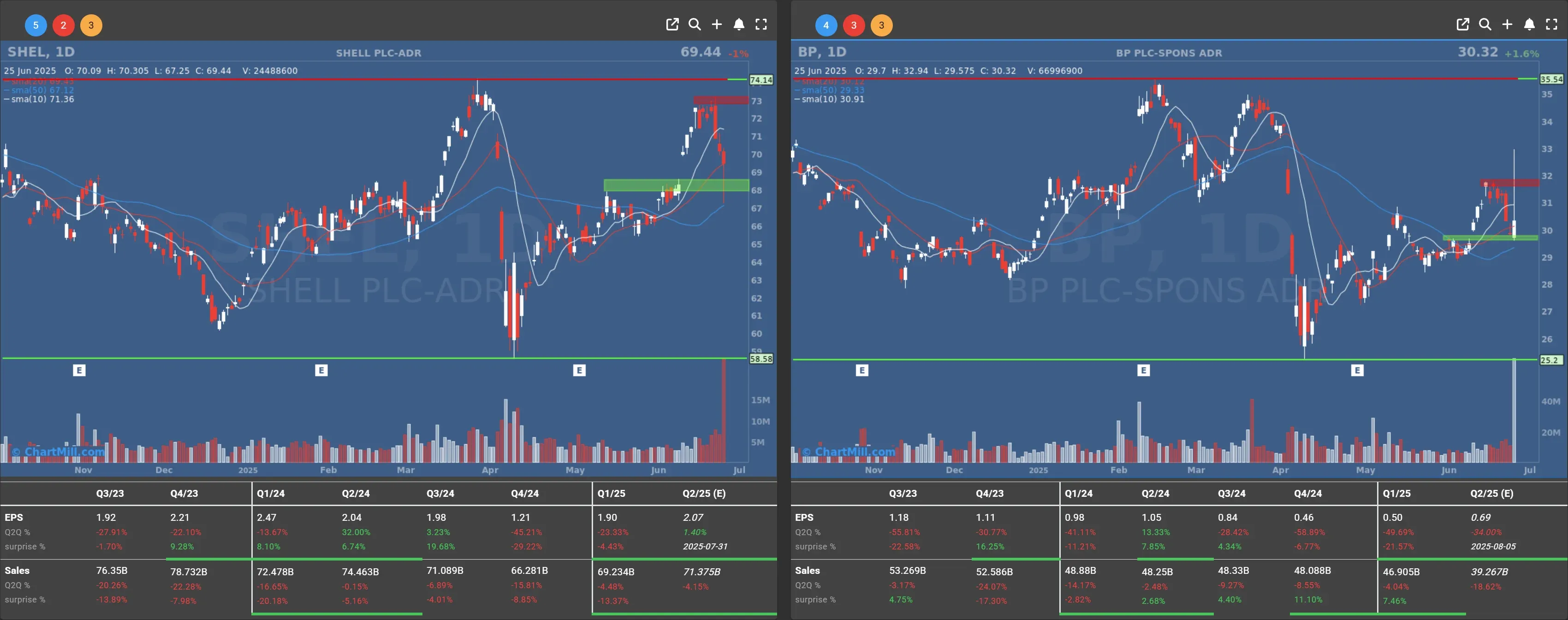

M&A Rumors and Stock Movers

Shell (SHEL | -1.0%) and BP (BP | +1.64%) grabbed headlines amid takeover chatter. Reports swirled about Shell eyeing BP in a potential $80 billion deal, though Shell denies it. Still, this type of rumor doesn’t just pop out of nowhere.

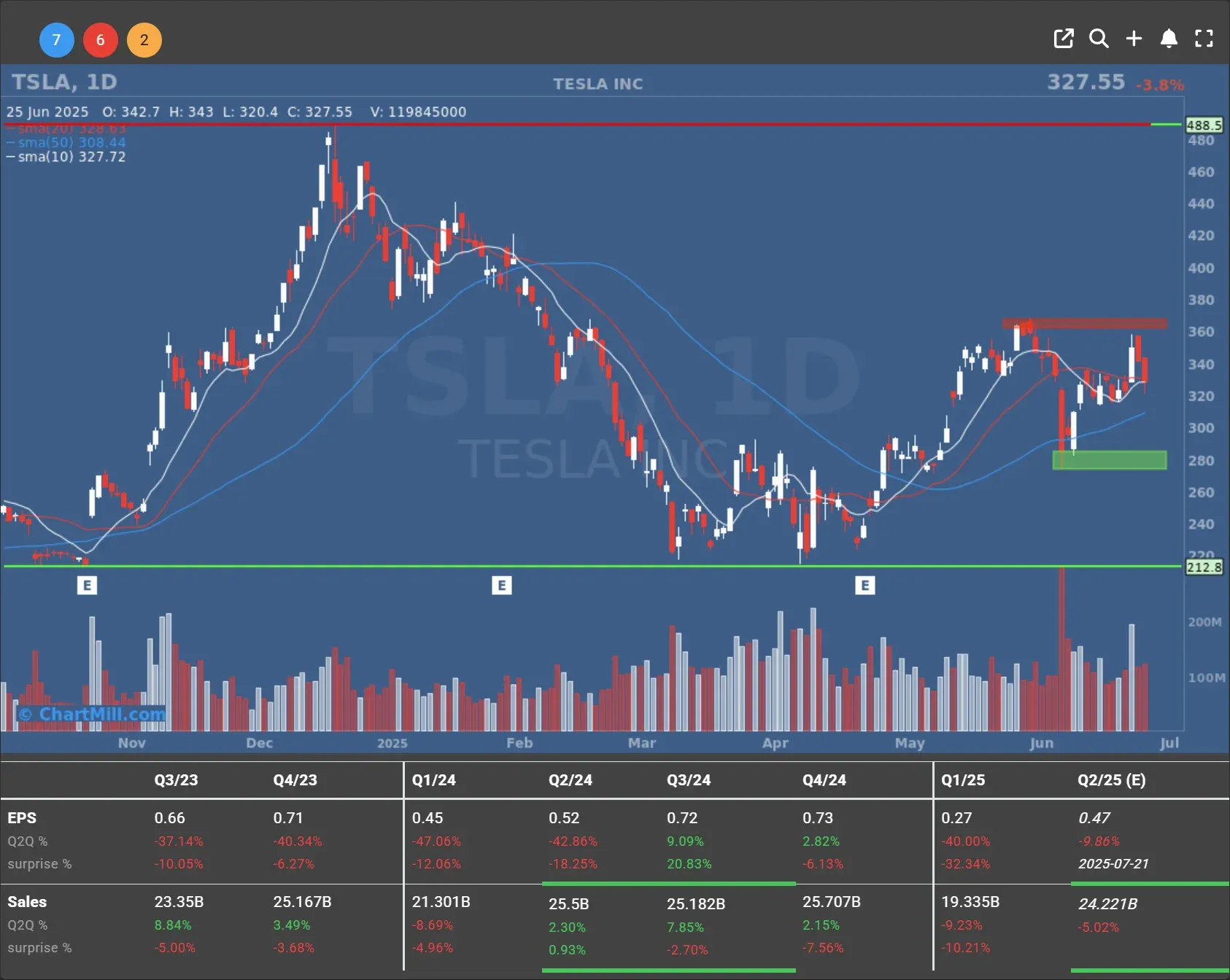

On the downside, Tesla (TSLA | -3.79%) took another hit, with European revenue declining.

Torrid Holdings (CURV | -38.24%) cratered on plans to issue more stock.

Meanwhile, BlackBerry (BB | +12.47%) got a rare boost after raising revenue guidance on better-than-expected quarterly results.

Bottom line: The AI boom is real, the rate cut debate is heating up, and earnings season is about to test everyone's nerves. As always, stay sharp and don't let the headlines distract you from the bigger picture.

Kristoff - Co-Founder ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, June 26

30.29

-0.03 (-0.1%)

50.37

-0.31 (-0.61%)

221.07

-0.93 (-0.42%)

155.02

+0.71 (+0.46%)

51.04

-0.07 (-0.14%)

11.57

+0.08 (+0.7%)

7.65

+1.98 (+34.92%)

3.27

+0.12 (+3.81%)

Find more stocks in the Stock Screener

BP Latest News and Analysis

18 hours ago - ChartmillMarket Monitor News June 26 BMO (QuantumScape, BlackBerry UP - Torrid Holdings, General Mills DOWN)

18 hours ago - ChartmillMarket Monitor News June 26 BMO (QuantumScape, BlackBerry UP - Torrid Holdings, General Mills DOWN)Wall Street Edges Closer to Records While Volatility Looms in the Background