The investment philosophy developed by Peter Lynch during his tenure managing Fidelity's Magellan Fund emphasizes identifying companies with sustainable growth trajectories trading at reasonable valuations. His approach combines elements of both growth and value investing, focusing on businesses that demonstrate strong fundamentals without excessive speculation. Lynch's methodology systematically evaluates earnings growth, valuation metrics adjusted for growth, and financial health indicators to find companies positioned for long-term success. This disciplined framework helps investors avoid overhyped stocks while identifying enterprises with durable competitive advantages and sound financial footing.

Meeting Lynch's Growth Criteria

Baker Hughes Co (NASDAQ:BKR) demonstrates several characteristics that align with Lynch's investment principles. The company's earnings per share have grown at an average annual rate of 23.35% over the past five years, comfortably within Lynch's preferred range of 15-30% growth. This threshold is important in Lynch's methodology as it identifies companies expanding at a sustainable pace rather than those experiencing explosive but potentially temporary growth spurts. The consistency of this earnings growth suggests Baker Hughes has established a durable business model capable of generating increasing profits over multiple economic cycles.

The company's profitability metrics further reinforce its appeal to GARP investors:

- Return on Equity of 17.22% exceeds Lynch's 15% minimum threshold

- Return on Invested Capital stands at 11.38%, ranking among the top performers in the energy equipment sector

- Profit margin of 11.04% places the company in the industry's upper quartile

These metrics indicate efficient capital allocation and strong operational execution, both hallmarks of companies Lynch would classify as having "stalwart" characteristics.

Valuation Assessment

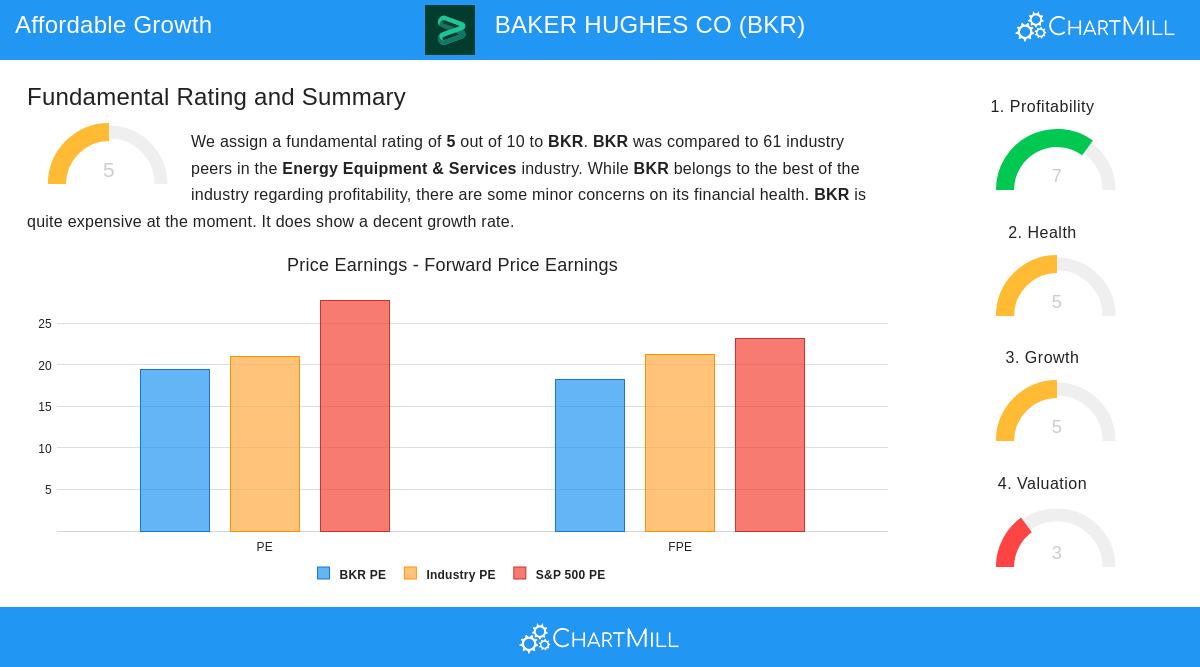

Baker Hughes presents an interesting valuation case when examined through Lynch's preferred metrics. The company's PEG ratio of 0.83 falls below Lynch's threshold of 1.0, indicating the stock may be reasonably priced relative to its historical growth rate. This metric was particularly important to Lynch as it helps investors avoid overpaying for growth. While the standard P/E ratio of 19.41 appears elevated compared to some value opportunities, the growth-adjusted valuation suggests the market may not be fully recognizing the company's earnings power.

The valuation picture contains several noteworthy elements:

- Forward P/E ratio of 18.18 compares favorably to the S&P 500 average

- Enterprise value to EBITDA multiple appears rich relative to industry peers

- Current valuation reflects expectations for continued but moderated earnings growth

Financial Health and Stability

Baker Hughes maintains a financial profile that aligns with Lynch's emphasis on balance sheet strength. The company's debt-to-equity ratio of 0.34 falls well below the screener's maximum threshold of 0.6 and even undercuts Lynch's more stringent preference for ratios below 0.25. This conservative leverage approach provides financial flexibility and reduces risk during industry downturns. The current ratio of 1.41 indicates sufficient short-term liquidity, though it ranks in the lower half of industry peers.

Additional financial health indicators include:

- Positive operating cash flow maintained throughout the past five years

- Reduced debt-to-assets ratio compared to prior year

- Share count reduction through buybacks in recent periods

Fundamental Analysis Overview

According to ChartMill's fundamental analysis, Baker Hughes receives an overall rating of 5 out of 10. The company demonstrates particular strength in profitability metrics, ranking among industry leaders in return measures and margins. The analysis notes some concerns regarding financial health, primarily related to liquidity ratios, while characterizing the current valuation as somewhat expensive despite decent growth rates. The dividend program appears sustainable with a 10-year track record of consistent payments and a payout ratio below 30% of earnings.

Investment Considerations

For investors employing a GARP strategy, Baker Hughes represents a company operating in the essential energy services sector with demonstrated ability to grow earnings at an above-average pace. The company's focus on both traditional oilfield services and emerging energy transition technologies provides exposure to multiple growth vectors. While the energy equipment sector faces cyclical challenges, Baker Hughes' financial discipline and technological capabilities position it to manage industry volatility.

The company's alignment with several Lynch principles—sustainable growth, reasonable valuation relative to that growth, and financial resilience—makes it worthy of consideration for long-term portfolios. As with any investment, prospective investors should conduct their own thorough research and consider how Baker Hughes fits within their overall portfolio strategy and risk tolerance.

For investors interested in finding additional companies that meet Peter Lynch's investment criteria, you can access the complete stock screener to explore more potential opportunities.

Disclaimer: This article presents objective analysis based on specified investment criteria and should not be considered investment advice. All investment decisions should be made after thorough personal research and in consultation with financial professionals. Past performance does not guarantee future results, and all investments carry risk of loss.