The "Affordable Growth" investment strategy works to find companies that show good growth possibility while keeping fair prices, steering clear of the problems of costly momentum stocks. This method concentrates on businesses with sound basic wellness and earnings, making certain they have the monetary steadiness to support growth. By choosing stocks with growth scores above 7 and price scores over 5, along with satisfactory earnings and wellness measures, investors try to gain upside possibility without paying too much for future profits.

Atour Lifestyle Holdings-ADR (NASDAQ:ATAT) appears as a strong candidate in this structure. The Chinese hotel company, based in Shanghai with more than 834 properties in 151 cities, has shown good operational growth since its November 2022 IPO. Its varied brand collection, including Atour, Atour Light, and theme-based hotels, places it favorably in China's changing hospitality industry.

Growth Path

ATAT shows very good growth features that are the center of its investment charm:

- Revenue jumped 55.34% over the last year, with a five-year average yearly growth rate of 35.84%

- Earnings per share increased 36.58% year-over-year, with a notable 138.03% average yearly growth over recent years

- Future estimates show continued force with anticipated EPS growth of 22.98% and revenue growth of 24.40% each year

These numbers show the company's effective growth across China's smaller cities, taking advantage of increasing local tourism and spending habits. The growth score of 9/10 highlights ATAT's place in the leading group of growth companies in the hotels and leisure field.

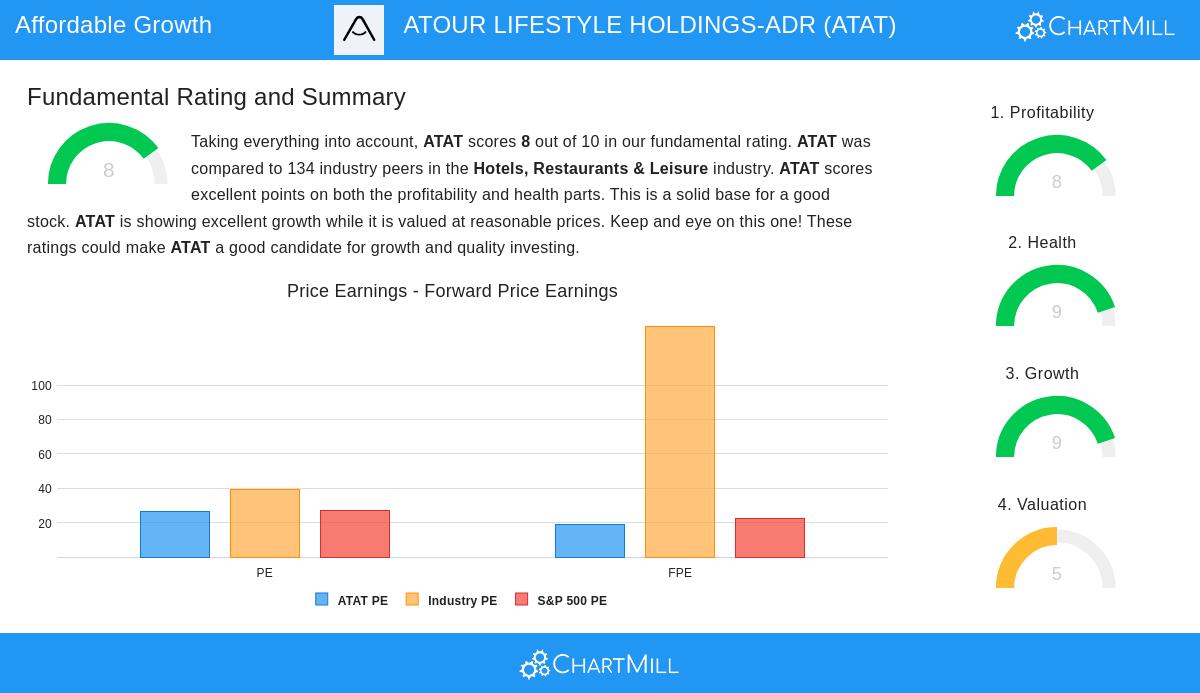

Price Evaluation

While growth is notable, price stays fair, a key mix for affordable growth plans:

- P/E ratio of 26.20 matches the field average and is near the S&P 500's 26.84

- Forward P/E of 18.81 is under both field averages and the wider market

- PEG ratio shows payment for growth, hinting the present price might be fair given expansion chances

- Price/Free Cash Flow ratio is lower than 68.66% of field competitors

The price score of 5/10 shows a even review, not low-cost nor overly expensive, which is exactly what affordable growth investors look for: companies growing quickly without needing high multiples.

Earnings and Monetary Wellness

Beyond growth and price, ATAT shows basic force that backs lasting growth:

- Return on invested capital of 22.51% is better than 93.28% of field competitors

- Profit margin of 16.41% is in the top ten percent of the field

- Operating margin of 21.51% is higher than 80.60% of rivals

- Very good monetary wellness score of 9/10 backed by very little debt (Debt/Equity ratio of 0.02)

- Current ratio of 2.29 and quick ratio of 2.23 show good cash position

These earnings and wellness measures (scored 8/10 and 9/10 in turn) supply the base for ongoing growth, making sure the company can pay for expansion without too much borrowing or monetary pressure.

Investment Points

ATAT's mix of forceful growth, fair price, and sound basics makes it especially interesting for investors looking for affordable growth chances. The company's place in China's healing hospitality field gives extra support as local travel keeps improving after the pandemic. Still, investors ought to watch China's economic situation and customer spending habits, which might affect the hospitality field.

The company's fairly brief dividend history (scored 4/10) shows its new IPO status, though the present yield of 2.10% with a maintainable payout ratio gives income creation next to growth possibility.

For investors wanting to find similar affordable growth chances, more screening outcomes are available through our Affordable Growth Stock Screener.

Disclaimer: This analysis uses basic data and scores from our fundamental analysis report and is not investment advice. Investors must do their own research and think about their risk comfort before making investment choices. Past results do not ensure future outcomes.