How to measure a company's Financial Health?

Investing in stocks can be done in many different ways but besides the known quality requirements which are aimed at profitability, growth, value and quality of management, there is also the question of the financial health of the company in which you want to invest.

After all, the idea is that the company in which you're going to invest is sufficiently viable to continue operating in the near future so that your investment can pay off.

How you can use ChartMill to screen companies on the basis of valuation, growth or the extent to which they pay out dividends has been discussed before. You can read more about this via the links below.

- How to find Growth Stocks that could become tomorrow's leaders?

- How to screen and select the best value stocks?

- How to screen and select the best dividend stocks?

In this article we will take a closer look at a number of financial ratios that give you a better insight into the financial health of a company and how you can set up these ratios as filters in ChartMill. Overall, there are three indicators that contribute significantly to a company's financial picture.

Solvency

Solvency represents the ratio of equity capital to the capital that comes from third parties (contributed debt capital). To what extent is the company able to meet its debt obligations on a long-term basis?

You can find an answer to this by calculating the debt-to-equity ratio. As can be seen from the name, this measures exactly the debt to equity ratio. A lower D/E ratio is preferable because it means that a larger portion of the company's business is funded by shareholders and not by creditors. This is not only good for shareholder trust, it also means that the company owes less interest to lenders.

Keep in mind, however, that you should only use this ratio to compare companies within the same sector. Capital-intensive sectors will logically have a higher D/E ratio (sometimes even higher than 2) than companies that require little capital to carry out their activities (1 to 1.5). By the way, never base your decision only on the pure figure. You can of course take a standard value as an upper limit, but at least as important is the evolution of the debt. If it shows a downward trend, that is a good sign in any case.

A too low D/E is not ideal either. After all, it means that the company is making hardly any use of outside capital and is therefore perhaps missing out on opportunities to expand its activities and realize even greater added value.

Example of a D/E screening filter based on the following parameters:

Operating Efficiency

How efficiently does a company manage its resources? What operating costs are necessary to achieve the desired result? If company A, a sector colleague of company B, achieves the same result as company B but does so with fewer costs (read 'more efficiently'), then the operating return of company A is significantly better than that of company B.

As an investor, you are naturally looking for firms that manage to minimize operating costs. A commonly used ratio for this is the operating margin (to be compared between competitors). This reflects the operating margin of a company and shows to what extent a company is able to generate profits from its activities. The operating margin is calculated by dividing the operating result by net sales after factoring in variable costs but without interest or taxes. Because only operating costs are taken into account, this ratio is very suitable for mapping the profitability of the pure core business.

The higher the margin the better the company succeeds in effectively turning sales into profit (higher efficiency). In the context of the purpose of this article, it also means that a company is better armed against economic crises or specific temporary events with a potentially negative impact.

An operating margin of 15% is considered 'healthy' by default. But here again, the evolution of the ratio is especially important to have a broader view of the company in question.

Example of an operating margin screening filter based on the following parameters:

Liquidity

To what extent can a company meet its short-term liabilities? If it can meet those obligations, the company is "liquid. This is one of the foundations of a financially sound company. If a company fails to meet its obligations even in the short term then there is no future for that company either.

A company that is illiquid will eventually cease to exist. To measure the degree of liquidity, cash and cash equivalents (cash available in the company + easily convertible assets of the company) are taken into account. To measure liquidity, two ratios are used, more precisely the Current Ratio and the Quick Ratio.

The Current Ratio shows whether the company can pay off its short-term debts (short-term borrowed capital) with the available cash and current assets. If the Current Ratio is greater than or equal to 1 then the company is considered liquid. However, a ratio of at least 1.5 is maintained to be considered 'healthy'.

The difference with the Quick ratio lies in the fact that for its calculation - unlike with the Current Ratio - the company's inventories are not taken into account. Here, too, 1 is taken as the standard before the company is considered liquid. This is sufficient since the inventories were already disregarded.

The Quick Ratio is also known as the 'Acid test' and is a lot more conservative and realistic than the Current Ratio because stocks cannot always be converted into cash just like that. The Quick Ratio gains importance in companies whose inventories have a high turnover rate or where the value of those same inventories is volatile or uncertain.

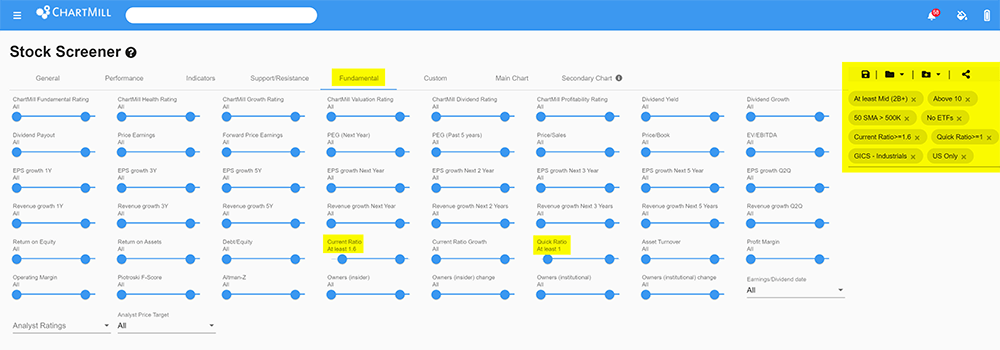

Example of an Current and Quick Ratio screening filter based on the following parameters:

Profitability

The profitability of a business is important for the viability and continuity of a company. Too low a level of profitability hampers further growth and development and therefore new investments. In the long term, this implies a risk for the continuity of the company. Especially in case of negative profitability figures, the company can get into trouble in the short term.

Profit in itself says little, however, it is mainly the net profit margin that is important. Company A whose profit is $2,000,000 may look a lot more impressive than company B whose profit is $400,000, but if it turns out that the total turnover to arrive at that profit for company A is $50,000,000 and for company B it is $3,000,000, then that gives a much more nuanced picture.

Company A's net margin in that case is only 4% while that for Company B is over 13%. A larger net margin provides a greater financial safety cushion and it also allows the company to continue to grow or pay dividends to shareholders.

The Net Profit Margin is one of the most important indicators to assess the financial stability of a company. Moreover, this ratio does take into account the effect of interest payments and tax expenditures, unlike the Operating Margin discussed earlier in this article.

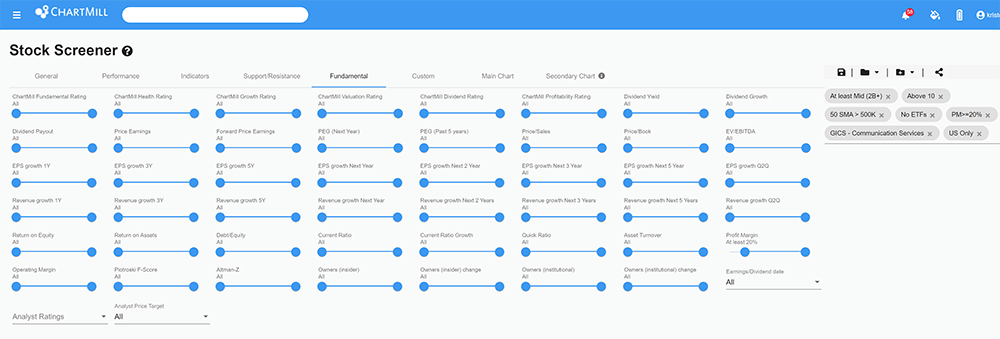

Example of an Profit Margin screening filter based on the following parameters:

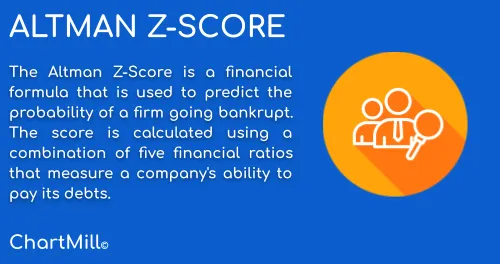

Altman Z-score

The Altman Z-score is not a ratio in itself but a mathematical model that can be used to determine the creditworthiness of a company, both public and private. The model of the Altman Z-score is aimed at predicting the probability of bankruptcy of a company. To do this, it uses business figures that are easy to find for most companies.

Keep in mind that this score does not automatically mean that the selected companies will actually go bankrupt. The formula used for the original score is very general, meanwhile there are also variants available that distinguish more between the type of company. In this article you can read some more information about the Z-score.

Nevertheless, it is a good tool to use in your analysis that tries to assess the financial stability of a company.

Example of an Altman-Z screening filter based on the following parameters: