QUALCOMM INC (NASDAQ:QCOM): A GARP Investment Opportunity

By Mill Chart

Last update:

QUALCOMM INC (NASDAQ:QCOM) is a leading developer of foundational technologies for mobile devices and wireless products. The company operates in three segments: Qualcomm CDMA Technologies (QCT), Qualcomm Technology Licensing (QTL), and Qualcomm Strategic Initiatives. With a strong presence in semiconductors and wireless communication, QCOM presents an interesting case for investors seeking a balance between growth and value—often referred to as Growth at a Reasonable Price (GARP).

Growth vs. Value: The GARP Approach

Investing strategies often fall into two broad categories: growth and value. Growth investors focus on companies with strong earnings expansion, while value investors seek undervalued stocks with solid fundamentals. The GARP strategy blends these approaches, targeting companies with sustainable growth at reasonable valuations. QUALCOMM INC fits this profile, combining steady growth metrics with attractive valuation ratios.

Why QUALCOMM INC Meets GARP Criteria

Strong Historical Growth

QUALCOMM INC has demonstrated robust earnings growth, with a 5-year EPS growth rate of 23.53%. This exceeds the 15% threshold often used in GARP strategies, indicating consistent profitability. Revenue growth has also been healthy, averaging 14.76% annually over the past five years.

Attractive Valuation Metrics

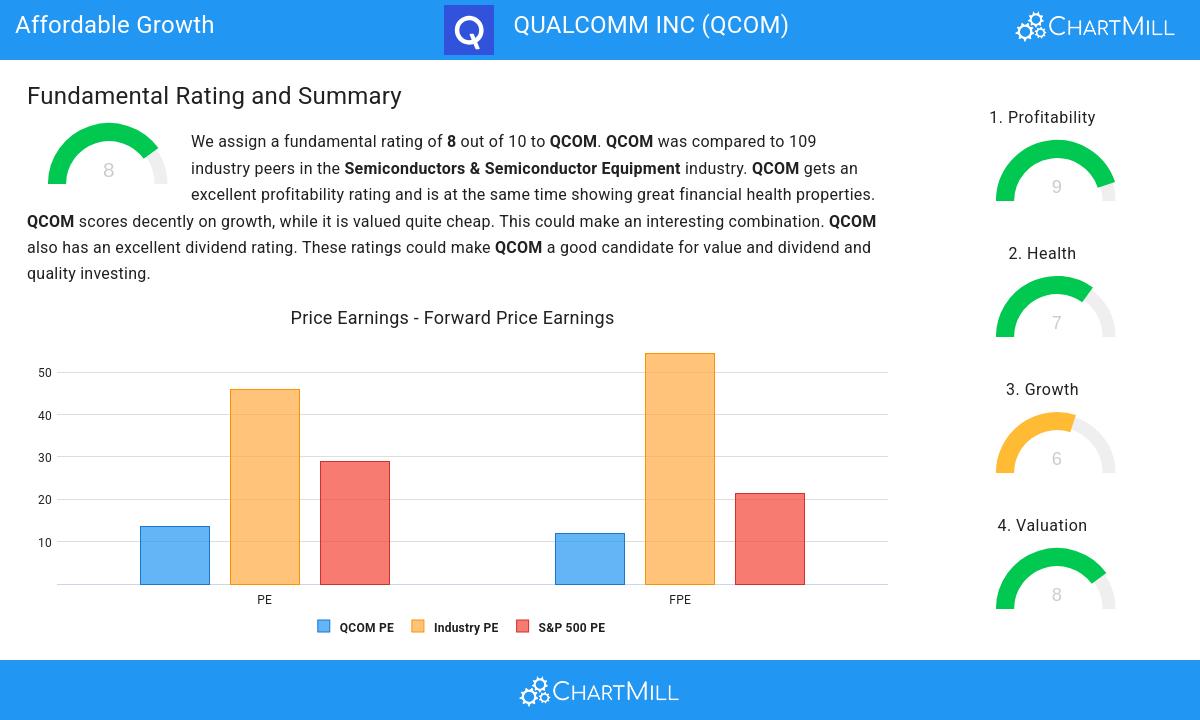

Despite its strong growth, QCOM trades at a P/E ratio of 13.47, well below both the industry average (45.82) and the S&P 500 (28.98). The PEG ratio (5Y) of 0.77—which adjusts the P/E for growth—suggests the stock is undervalued relative to its earnings expansion.

Solid Financial Health

The company maintains a debt-to-equity ratio of 0.49, indicating manageable leverage. Its current ratio of 2.62 reflects strong liquidity, ensuring it can meet short-term obligations. Additionally, QUALCOMM boasts a return on equity (ROE) of 39.27%, highlighting efficient capital use.

Dividend Stability

QUALCOMM offers a dividend yield of 2.42%, slightly below the industry average but with a reliable payout history. The company has maintained or increased its dividend for at least 10 years, supported by a sustainable payout ratio of 35.38%.

Fundamental Analysis Summary

Our fundamental analysis report assigns QCOM a rating of 8 out of 10, reflecting strong profitability, financial health, and valuation. Key strengths include high ROE, solid margins, and a low PEG ratio. While future revenue growth is expected to slow slightly, earnings growth remains steady.

For investors interested in similar opportunities, explore our Peter Lynch Strategy screen for more high-quality GARP stocks.