The search for undervalued companies remains a cornerstone of value investing, a strategy pioneered by Benjamin Graham and later popularized by Warren Buffett. This approach focuses on identifying stocks trading below their intrinsic value, determined through fundamental analysis of financial health, profitability, and growth prospects. By targeting companies with strong underlying metrics that the market has overlooked, value investors aim to capitalize on eventual price corrections. One such candidate emerging from a systematic screen for decent value stocks is Zoom Communications Inc (NASDAQ:ZM), which demonstrates several characteristics that may appeal to value-oriented investors.

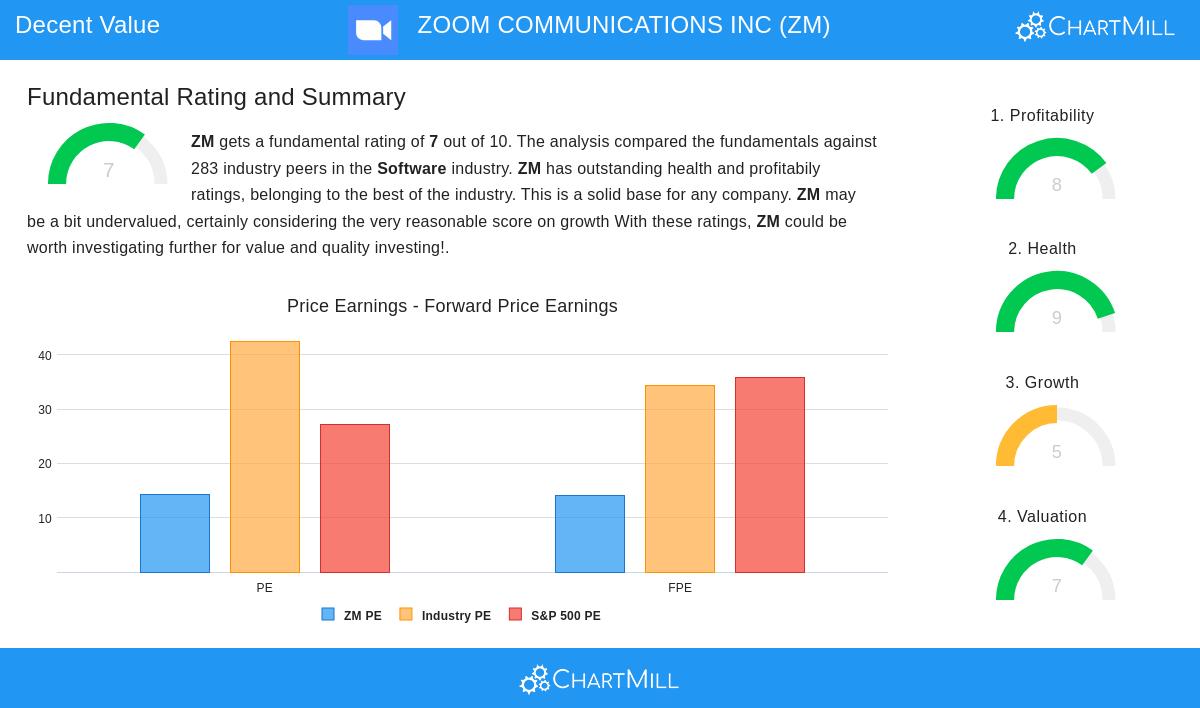

Valuation Metrics Suggest Undervaluation Zoom's valuation metrics present a notable case for potential undervaluation. The company trades at a Price/Earnings ratio of 14.34, significantly below both the S&P 500 average of 27.24 and the software industry average of 42.54. This discount becomes more pronounced when examining forward-looking measures, with 88% of industry peers showing higher Price/Forward Earnings ratios. The Enterprise Value to EBITDA and Price/Free Cash Flow ratios further support this valuation advantage, placing Zoom in the cheapest quartile of software companies. For value investors, these metrics signal that the market may be underestimating Zoom's true worth, creating a potential opportunity if the valuation gap closes.

Exceptional Financial Health Provides Stability The company's financial health rating of 9/10 reflects remarkable balance sheet strength. Zoom operates with zero debt, eliminating interest expense concerns and providing flexibility during economic uncertainty. The current ratio of 4.57 and quick ratio of 4.57 demonstrate substantial liquidity, outperforming 87% of industry peers in short-term obligation coverage. This financial strength aligns with value investing principles that prioritize companies capable of weathering market volatility without jeopardizing their operational continuity. The Altman-Z score of 8.43 indicates minimal bankruptcy risk, offering investors confidence in the company's financial stability.

Strong Profitability Supports Business Quality Zoom achieves an impressive profitability rating of 8/10, with metrics that surpass most software competitors. The company maintains a 22.31% profit margin, exceeding 89% of industry peers, while its 18.13% operating margin outperforms 86% of comparable companies. These margins have shown improvement in recent years, indicating efficient cost management and pricing power. The Return on Assets of 9.57% and Return on Equity of 11.78% both rank in the top quartile for the software sector. For value investors, sustained high profitability suggests a durable competitive advantage and the ability to generate consistent returns on invested capital.

Moderate Growth with Historical Strength While growth has moderated from pandemic-era peaks, Zoom maintains a respectable growth rating of 5/10. Revenue increased 3.05% over the past year, with a remarkable historical average annual growth rate of 49.60% over previous years. Earnings per share grew 5.50% annually while demonstrating a strong 73.67% average annual growth over the longer term. Although future projections indicate modest single-digit growth in both revenue and earnings, the company's established market position in communications software provides a foundation for sustained expansion. Value investors typically prefer companies with reasonable growth expectations rather than speculative hyper-growth scenarios, making Zoom's current profile potentially attractive.

Investment Considerations and Potential Risks The company's transition from hyper-growth to mature growth phase brings both opportunities and challenges. While Zoom faces increased competition in the communications platform space, its profitability metrics suggest effective adaptation to market conditions. The lack of dividend payments may deter income-focused investors, though this is common among technology companies reinvesting cash flows into business development. The changing workplace communication landscape requires continuous innovation, but Zoom's strong cash position provides resources to maintain competitiveness.

Value investors seeking companies with sound fundamentals trading at reasonable valuations may find Zoom Communications worth further investigation. The full fundamental analysis report provides additional detail on these metrics and their industry comparisons.

For investors interested in discovering similar opportunities, our Decent Value Stocks screen regularly identifies companies exhibiting these characteristics of undervaluation combined with solid fundamentals.

Disclaimer: This analysis is provided for informational purposes only and does not constitute investment advice, recommendation, or endorsement of any security. Investors should conduct their own research and consult with a qualified financial advisor before making investment decisions.