The Caviar Cruise stock screening strategy aims to find high-quality companies for long-term investment. Based on quality investing principles, this method looks for firms with steady revenue and profit growth, solid returns on invested capital, low debt, and reliable earnings. The approach highlights lasting competitive edges, efficient operations, and strong finances, traits that help businesses grow value over time.

One company that fits this screening model is Zoom Communications Inc (NASDAQ:ZM). The video communications provider, widely recognized during the pandemic, displays multiple traits that match the Caviar Cruise standards.

Key Strengths Based on Caviar Cruise Criteria

-

Solid Revenue and EBIT Growth

- The Caviar Cruise screen looks for at least 5% annual revenue growth over five years. Zoom meets this with a 3.06% 5-year revenue CAGR, adjusted for post-pandemic trends, while maintaining a strong long-term growth path.

- Zoom’s EBIT growth over the same period is 129.77% CAGR, far exceeding the 5% target. This shows not only revenue growth but also better operational efficiency and pricing strength, signs of a high-quality business.

-

High Return on Invested Capital (ROIC)

- ROIC, a key measure for quality investors, evaluates how well a company uses its capital to generate profits. Zoom’s ROIC excluding cash and goodwill (72.67%) is outstanding, well above the 15% minimum set by the screen. This indicates Zoom uses capital effectively, a mark of a lasting competitive edge.

-

No Debt and Strong Cash Flow

- The screen prefers companies with low debt, ideally a Debt/Free Cash Flow ratio under 5. Zoom has no debt, giving it a strong financial position.

- Its 5-year average Profit Quality (FCF/Net Income) of 371.14%, far above the 75% target, shows earnings are turning into cash at an impressive rate. This reduces the need for external funding and supports shareholder returns.

-

Better Profitability Metrics

- Zoom’s Operating Margin (18.13%) and Profit Margin (22.31%) rank in the top 15% of its software industry peers. These margins have also grown over time, reflecting scale benefits and careful cost control, key features of long-term value builders.

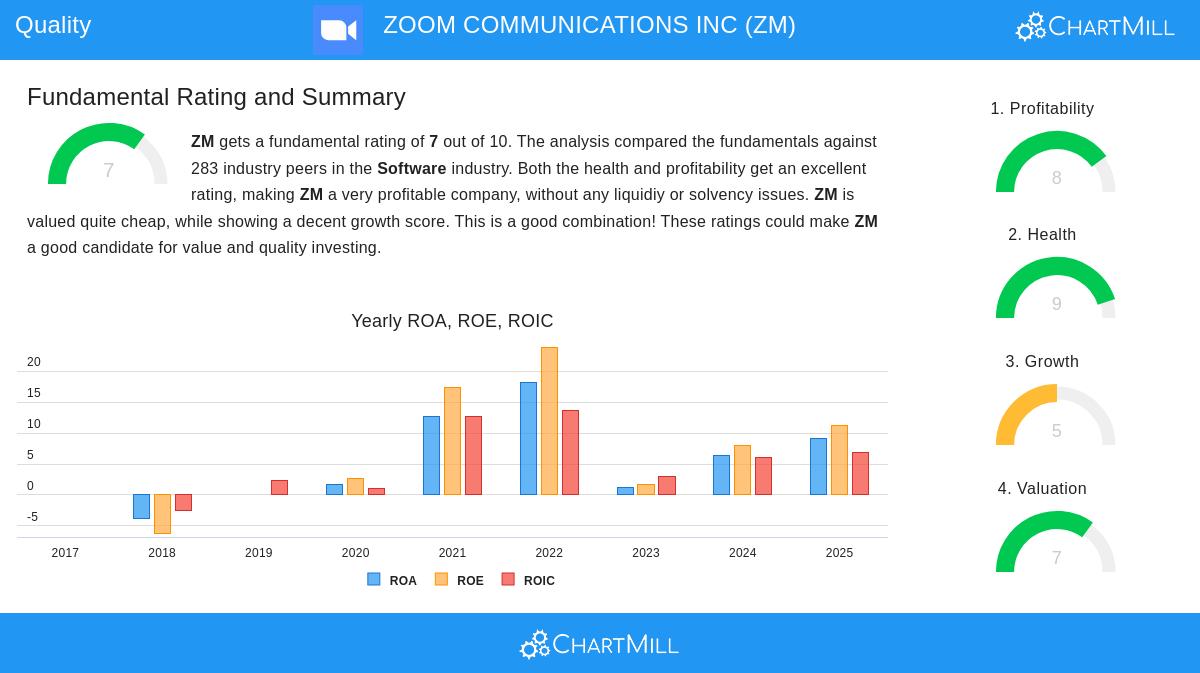

Fundamental Analysis Summary

Zoom’s fundamental report gives it a rating of 7/10, with high scores in profitability (8/10) and financial health (9/10). Key points include:

- Profitability: High margins (Gross Margin: 75.85%) and strong returns on equity (11.78%) and assets (9.57%).

- Valuation: With a P/E of 12.47, Zoom seems undervalued compared to its industry (P/E 55.70) and the S&P 500 (P/E 26.73).

- Growth: While recent revenue growth has slowed (~3% yearly), its past growth (49.60% 5-year CAGR) and rising ROIC suggest stability.

Challenges and Factors to Note

Despite its strengths, Zoom faces hurdles:

- Slower Growth: Post-pandemic demand shifts have reduced revenue growth, though profitability stays strong.

- Competition: Rivals like Microsoft Teams and Cisco Webex keep the market competitive.

Final Thoughts

Zoom Communications Inc fits the Caviar Cruise criteria with its high ROIC, debt-free balance sheet, and strong cash flows. While growth has eased from pandemic highs, its profitability, margins, and valuation make it an attractive option for quality investors looking for stable businesses.

For more stocks that pass the Caviar Cruise screen, view the full results here.

Disclaimer: This article is not investment advice. Always do your own research or consult a financial advisor before making investment decisions.