In the world of long-term investing, few strategies have earned as much respect as the approach supported by Peter Lynch, the famous manager of Fidelity’s Magellan Fund. His method focuses on finding companies that show lasting growth, good financial condition, and fair prices, often called Growth at a Reasonable Price, or GARP. Lynch thought investors could find good chances by using basic analysis to locate businesses increasing steadily but not too much, with healthy balance sheets and good profit measures. This organized system helps prevent overhyped, expensive stocks while focusing on lasting competitive strengths and operational effectiveness.

YETI HOLDINGS INC (NYSE:YETI) appears as a good candidate when looked at with Lynch’s standards. The company, which designs and sells high-end outdoor and recreation products like coolers, drinkware, and equipment, shows several traits that match well with the Lynch investment view.

-

Earnings Growth and Lasting Power: Lynch stressed the need for good, but not extreme, earnings growth, usually between 15% and 30% each year over five years. YETI’s EPS has increased at an average rate of 18.24% over the last five years, putting it right within this goal area. This shows a business that is growing at a steady speed, lowering the chance of burnout or unmaintainable growth. Lynch often cautioned against companies increasing too fast, as they might deal with operational problems or more competition. YETI’s steady growth shows operational control and good scaling.

-

Valuation Matched to Growth: The PEG ratio, which changes the P/E ratio for growth, is a key part of Lynch’s valuation method. He liked companies with a PEG ratio of 1 or lower, meaning the stock could be fairly priced compared to its growth path. YETI’s PEG ratio of 0.73 implies the market might be pricing its growth chances too low, giving a possible safety buffer for investors. This is important in Lynch’s plan because it helps find companies where the market has not completely added in future earnings potential.

-

Financial Condition and Low Debt: Lynch preferred companies with healthy balance sheets, especially those with low debt-to-equity ratios. YETI’s debt-to-equity ratio of 0.09 is not only much lower than the screen’s limit of 0.6 but also fits with Lynch’s stricter liking for ratios below 0.25. This shows a careful capital structure and lowers money risk, making sure the company can handle economic drops without being weighed down by interest costs. Also, YETI’s current ratio of 2.52 shows strong short-term cash flow, another sign of money stability that Lynch liked.

-

Profit and Effectiveness: Return on equity (ROE) is a main measure of how well a company makes profit from shareholder equity. Lynch wanted ROE above 15%, and YETI’s ROE of 22.07% is much higher than this mark. High ROE often suggests a lasting competitive edge and effective management, traits Lynch saw as key for long-term growth.

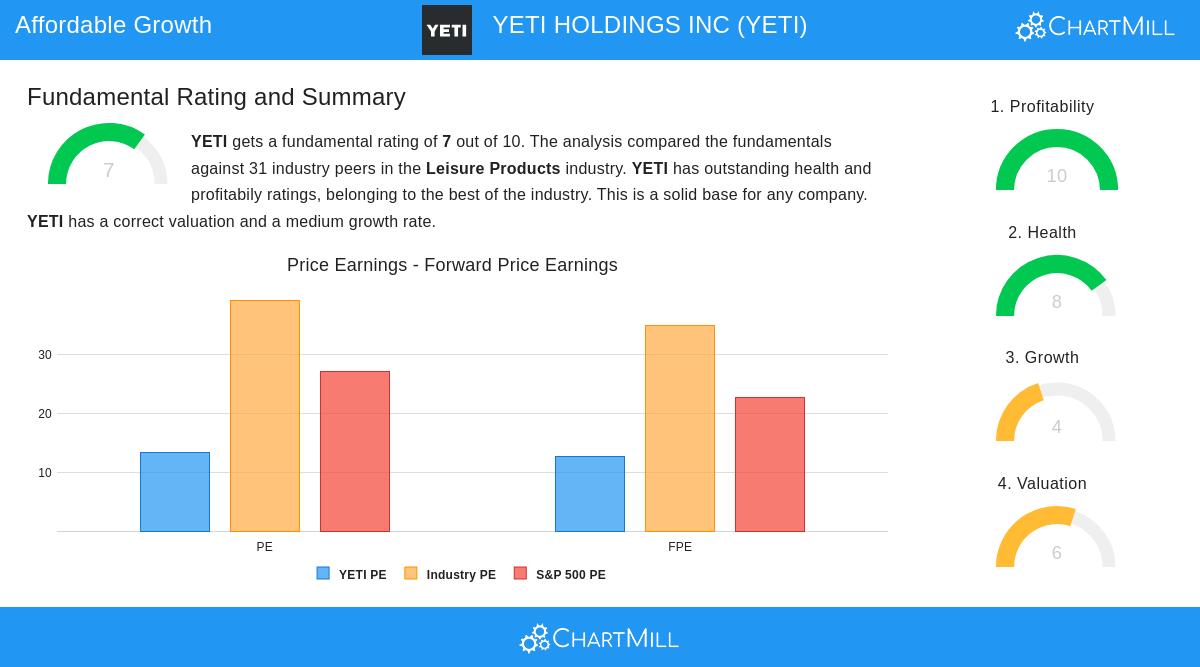

A look at YETI’s fundamental analysis report further supports its positives. The report gives YETI a good score of 7 out of 10, pointing out very good profit and strong financial condition. The company does better than most others in its field on measures like return on invested capital, profit margins, and ability to pay debts. Its valuation is also seen positively, with P/E and forward P/E ratios under industry averages. While growth is predicted to slow a bit soon, the main business stays healthy and well-set in the outdoor products market.

For investors wanting to look into other companies that fit Peter Lynch’s investment standards, more screening results can be found using this custom stock screener.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consider their financial situation and risk tolerance before making any investment decisions.