Value investing focuses on finding stocks priced below their true worth while having solid financial foundations. The approach, based on Benjamin Graham’s ideas, looks for firms with steady earnings, strong balance sheets, and reasonable growth potential, all at a lower price. One stock that fits this "Decent Value" screen is YETI HOLDINGS INC (NYSE:YETI), which offers a good price along with strong financials and earnings.

Valuation: An Attractive Opportunity

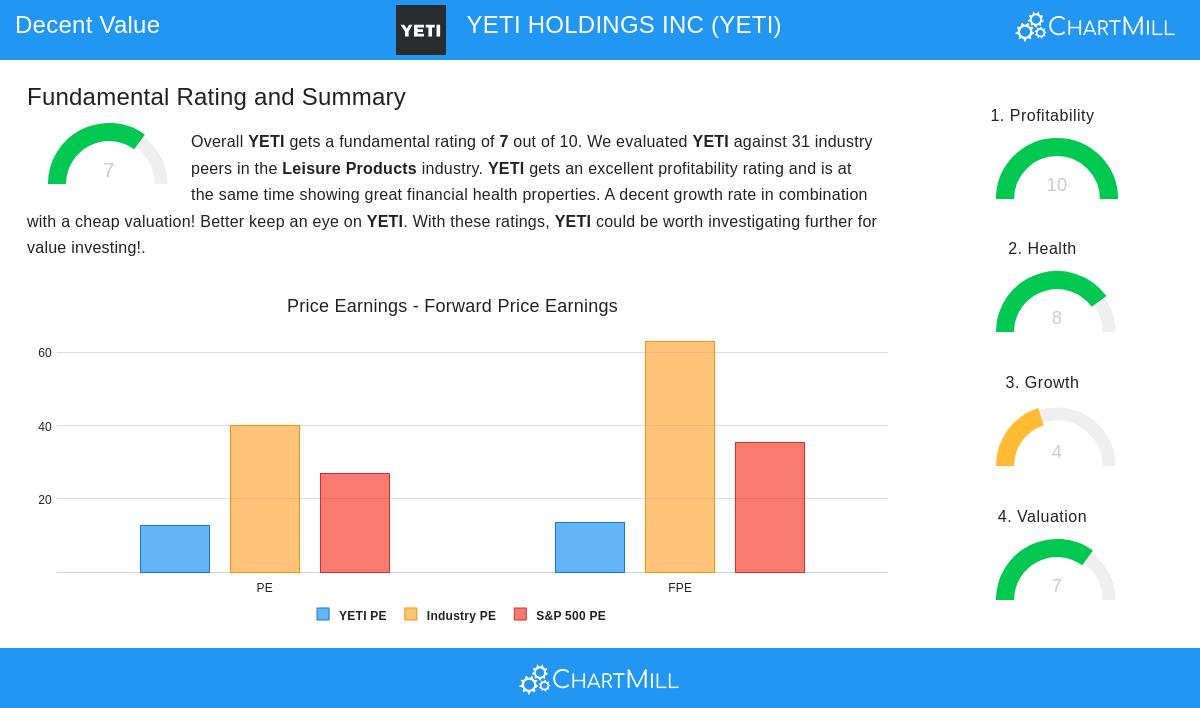

YETI’s valuation numbers show it is priced lower than its industry and the broader market:

- Price/Earnings (P/E) Ratio: At 12.68, YETI’s P/E is much lower than the industry average of 40.00 and the S&P 500’s 26.84. This makes it more affordable than 90% of similar companies in the Leisure Products sector.

- Price/Forward Earnings: A forward P/E of 13.51 further highlights its lower price, well below the S&P 500’s 35.29 and the industry’s 63.07.

- Enterprise Value/EBITDA and Price/Free Cash Flow: Both ratios suggest YETI is priced cautiously, with 77% and 81% of peers trading at higher levels, respectively.

For value investors, these numbers indicate a safety net—a key part of Graham’s strategy. The stock’s low multiples compared to earnings and cash flow imply the market may not fully recognize the company’s financial strength.

Profitability: Strong Performance

YETI’s earnings are impressive, earning a perfect 10/10 in ChartMill’s review:

- Return Metrics: A Return on Assets (ROA) of 13.60% and Return on Equity (ROE) of 22.07% place it in the top 7% of the industry. Its Return on Invested Capital (ROIC) of 18.50% beats the industry average (7.51%) and shows effective use of capital.

- Margins: Gross margins of 58.37% and operating margins of 13.13% are some of the best in the sector, with steady improvement in recent years.

High profitability matters to value investors because it shows a company can maintain and increase its true worth over time—essential for long-term gains.

Financial Health: A Stable Base

With a Health score of 8/10, YETI’s balance sheet is strong:

- Solvency: A Debt-to-Equity ratio of 0.09 and Debt-to-Free Cash Flow of 0.31 (meaning it could pay off all debt in less than four months) show little debt risk. Its Altman-Z score of 6.57 suggests very low bankruptcy risk.

- Liquidity: A Current Ratio of 2.52 and Quick Ratio of 1.48 confirm it has enough short-term assets to cover obligations.

Financial strength ensures the company can handle downturns and fund growth—a must for value investors who prioritize safety.

Growth: Consistent, Though Slowing

YETI’s Growth score (4/10) points to steady but slower expansion:

- Historical Growth: Revenue and EPS grew at 14.90% and 18.24% yearly over the past three years, though recent yearly growth has dipped to 3.62% (revenue) and 5.51% (EPS).

- Forward Estimates: Analysts expect 3.67% revenue and 5.72% EPS growth yearly—slower, but still positive.

While not a fast-growing stock, YETI’s stability fits value investing’s emphasis on reliable earnings over trends. The slowdown is worth watching, but its earnings and valuation offer some protection.

Conclusion: A Strong Value Pick

YETI’s mix of low price, excellent earnings, and financial stability makes it a strong choice for value-focused investors. The stock’s margins and returns suggest it is fundamentally better than its price indicates, while its balance sheet lowers risk. For those looking for undervalued stocks with lasting strengths, YETI deserves attention.

Find more stocks filtered by the same "Decent Value" criteria here.

Disclaimer: This analysis is not investment advice. Always do your own research or consult a financial advisor before making investment decisions.