Peter Lynch’s investment strategy, described in One Up on Wall Street, centers on finding companies with stable growth, fair valuations, and solid financial strength, often called the Growth at a Reasonable Price (GARP) method. The approach steers clear of overly hyped or rapidly expanding businesses, preferring those with steady earnings, controlled debt, and industry advantages. Important measures include earnings growth of 15% to 30%, a PEG ratio under 1, low debt-to-equity ratios, and strong return on equity (ROE). These factors help investors locate firms that are financially healthy and priced below their growth prospects.

YETI HOLDINGS INC (NYSE:YETI) stands out as a potential match for this model. The business, recognized for its high-quality outdoor and recreation goods, has shown the type of reliable growth and fiscal responsibility that fits Lynch’s ideas. Next, we review how YETI matches these standards and why it might interest long-term GARP investors.

Key Metrics Matching Peter Lynch’s Approach

- Stable Earnings Growth: YETI’s 5-year EPS growth of 18.24% fits Lynch’s ideal range of 15% to 30%. This shows steady profits without signs of unstable rapid expansion. The company’s revenue has also increased at a solid 14.90% yearly rate over the same span, confirming its ability to grow while staying balanced.

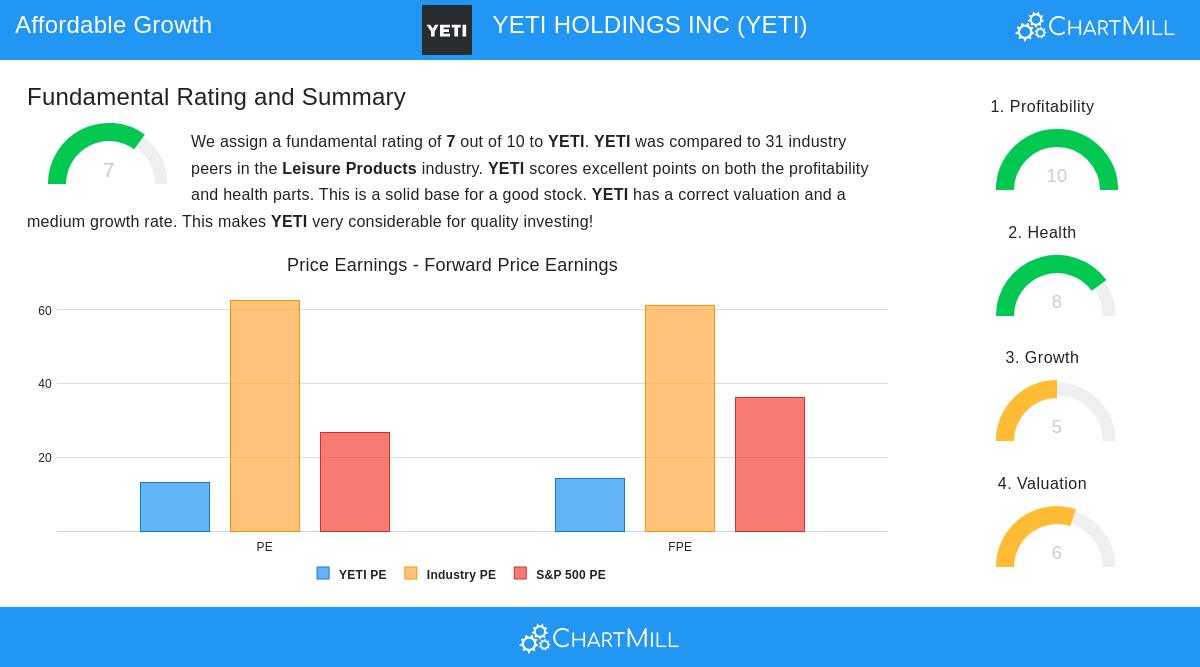

- Fair Valuation (PEG Ratio): The PEG ratio, which modifies the P/E ratio for growth, is 0.72, significantly under Lynch’s limit of 1. This implies the stock is priced below its earnings growth path. YETI’s P/E of 13.21 further reinforces this, trading lower than both the sector average and the S&P 500.

- Sound Financial Condition: With a debt-to-equity ratio of 0.09, YETI maintains cautious financing, matching Lynch’s liking for minimal debt. The current ratio of 2.58 also shows sufficient liquidity to cover short-term needs, lowering business risk.

- Strong Profitability (ROE): YETI’s ROE of 23.09% surpasses Lynch’s 15% target, showing effective use of investor funds. The company also leads its sector in margins, with a 58.18% gross margin and a 13.30% operating margin, highlighting its pricing control and expense efficiency.

Core Strengths Backing Long-Term Expansion

Our fundamental analysis report gives YETI a score of 7 out of 10, emphasizing its high profitability and reliable financial condition. Main points include:

- Profitability: YETI beats 90%+ of competitors in ROE, ROIC, and profit margins, with dependable cash flow production.

- Balance Sheet Stability: The firm’s Altman-Z score of 7.08 indicates minimal bankruptcy risk, while its low debt and healthy free cash flow (Debt/FCF of 0.32) allow room for reinvestment or shareholder benefits.

- Valuation: Even with its solid fundamentals, YETI trades below sector averages on measures like EV/EBITDA and P/FCF, providing a safety buffer.

Possible Risks and Factors

Though YETI aligns well with Lynch’s standards, investors should consider:

- Reduced Growth: Analysts forecast slower EPS and revenue growth (around 4% yearly) in future years, differing from previous patterns.

- Consumer Cyclical Sensitivity: As a premium consumer discretionary brand, YETI could encounter challenges during economic slowdowns.

Finding Additional Prospects

For investors looking for similar GARP options, our Peter Lynch Stock Screener offers a selected group of stocks meeting these requirements.

Disclaimer: This article is not investment advice. Perform your own research or seek guidance from a financial advisor before making investment choices.