Peter Lynch’s investment strategy, described in One Up on Wall Street, centers on finding companies with steady growth at fair prices, commonly known as the Growth at a Reasonable Price (GARP) approach. The method relies on fundamental analysis, selecting firms with solid earnings, low debt, and reliable growth, while steering clear of overvalued or highly leveraged businesses. By looking for stocks with a PEG ratio under 1, strong return on equity (ROE), and stable financials, Lynch’s approach seeks to identify investments that can provide lasting returns without paying too much for growth.

A company that matches this model is XPEL INC (NASDAQ:XPEL), a producer and seller of automotive paint protection films, window tints, and architectural glass products. The firm’s financials closely follow Lynch’s guidelines, positioning it as a strong option for GARP-focused investors.

Key Metrics Matching Peter Lynch’s Approach

-

Consistent Earnings Growth (EPS Growth 5Y: 26.4%)

Lynch preferred businesses with stable earnings growth, usually between 15% and 30%. XPEL’s five-year EPS growth of 26.4% fits this range, showing steady progress. The company’s revenue has also increased at a 26.48% yearly rate over the same span, confirming its ability to grow without relying on unsustainable spikes. -

Fair Pricing (PEG Ratio: 0.80)

A key part of Lynch’s strategy is the PEG ratio (Price/Earnings to Growth), which should be ≤1 to signal a stock is priced fairly relative to its growth. XPEL’s PEG ratio of 0.80 implies the market might be underestimating its growth, making it an attractive choice for growth-minded value investors. -

High Profitability (ROE: 19.03%)

Return on equity (ROE) shows how well a company turns shareholder investments into profits. Lynch looked for firms with ROE above 15%, and XPEL’s 19.03% surpasses this mark, ranking in the top 96% of its industry. This strong performance reflects efficient management and a lasting advantage. -

Solid Financial Position (Debt/Equity: ~0, Current Ratio: 4.42)

Lynch avoided companies with heavy debt, favoring those with modest borrowing. XPEL’s nearly zero debt-to-equity ratio and a current ratio of 4.42 (far above Lynch’s minimum 1.0) show excellent financial health, with enough liquidity to cover short-term needs.

Additional Strengths

Our full fundamental analysis of XPEL reveals more positives:

- Top-Tier Margins: Gross margins of 42.11% and operating margins of 13.62% exceed 96% of rivals in the auto parts industry.

- Reliable Cash Flow: Consistent positive operating cash flow and minimal debt improve financial security.

- Future Growth: Analysts forecast 22.96% yearly EPS growth ahead, indicating ongoing progress.

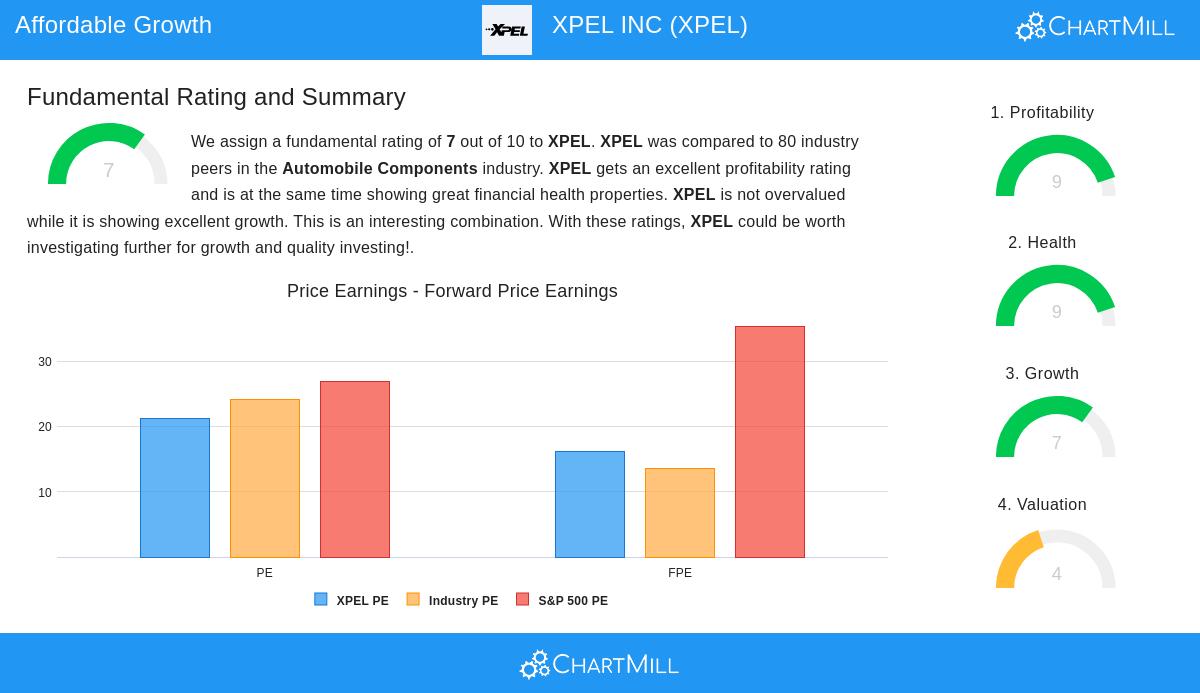

While the stock’s P/E ratio (21.22) is somewhat higher than its sector average, its strong earnings and growth potential support the premium.

Why This Fits GARP Investors

Lynch’s strategy sidesteps risky bets by concentrating on financially stable companies with clear growth paths. XPEL’s mix of steady earnings growth, fair pricing, and disciplined finances makes it a prime example of a Lynch-style pick—a business capable of delivering sustained returns without undue risk.

More Peter Lynch Screen Results

For investors looking for other stocks that meet these criteria, our Peter Lynch Stock Screener offers a filtered list of qualifying companies.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Always conduct your own research or consult a financial advisor before making investment decisions.