XPEL INC (NASDAQ:XPEL) stands out as a potential fit for investors seeking growth at a reasonable price (GARP). The company, which specializes in automotive paint protection films and window tints, meets several key criteria from Peter Lynch’s investment strategy, combining solid growth with sound financial health and reasonable valuation.

Why XPEL Fits the GARP Approach

- Strong Earnings Growth: XPEL has delivered a 5-year average EPS growth of 26.4%, well above the 15% minimum threshold in Lynch’s strategy. While recent earnings dipped slightly (-7.57% YoY), long-term trends remain robust.

- Reasonable Valuation (PEG Ratio): With a PEG ratio of 0.81, XPEL trades below the Lynch-preferred threshold of 1, indicating its earnings growth justifies its current valuation.

- Healthy Profitability: The company boasts a Return on Equity (ROE) of 20.14%, exceeding the 15% benchmark, and maintains strong margins, including a 10.92% net profit margin.

- Low Debt & Strong Liquidity: XPEL’s Debt/Equity ratio is near zero (0.0006), and its Current Ratio of 4.29 reflects ample liquidity to cover short-term obligations.

- Industry Leadership: XPEL outperforms most peers in profitability metrics like ROIC (19.29%) and operating margin (14.06%).

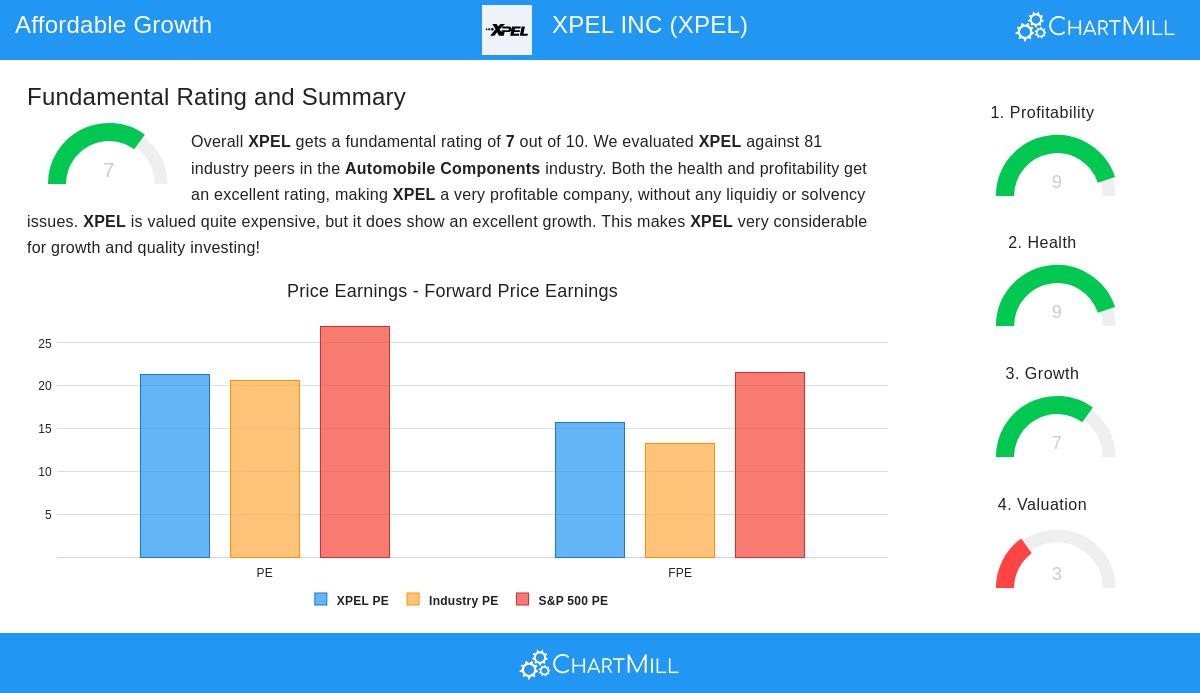

Fundamental Snapshot

XPEL’s fundamental report highlights its strengths:

- Profitability Score: 9/10 – Consistently profitable with industry-leading margins.

- Financial Health Score: 9/10 – Minimal debt and high solvency (Altman-Z score: 13.78).

- Valuation Score: 3/10 – P/E (21.28) is slightly above industry average, but growth prospects may justify it.

- Growth Score: 7/10 – Revenue growth (26.48% CAGR over 5 years) remains strong, with expected EPS growth of 22.96% annually in coming years.

For investors following a disciplined GARP approach, XPEL presents a compelling case with its balance of growth, profitability, and reasonable pricing.

Our Peter Lynch Strategy screener lists more stocks matching these criteria and is updated daily.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should always conduct your own analysis before making investment decisions.