Watsco Inc (NYSE:WSO) has appeared as a notable candidate via the Caviar Cruise stock screening method, a tactic built on quality investing ideas. This process focuses on finding businesses with lasting competitive strengths, sound financial condition, and reliable growth, qualities that render them appropriate for extended, buy-and-hold investment plans. The Caviar Cruise screen uses numerical filters to separate companies showing high operational results, earnings, and financial soundness, acting as a beginning for more thorough fundamental review.

A number of important measures place Watsco well inside the quality investing structure. The business shows a 5-year revenue compound annual growth rate (CAGR) of 6.81%, easily above the screen’s 5% minimum. More notably, its EBIT growth across the same timeframe hit 16.07%, greatly exceeding revenue growth. This difference points to better operational effectiveness and possible pricing strength, as the business creates larger earnings from each dollar of sales, a sign of high-grade businesses that can reach economies of scale or have firm market placement.

Watsco’s return on invested capital excluding cash, goodwill, and intangibles (ROICexgc) is at 21.97%, much higher than the 15% minimum needed by the screen. This shows effective use of capital and a capacity to create large returns from main activities, matching the quality investing focus on capital allocation superiority. The business also displays impressive financial control, with a debt-to-free-cash-flow ratio of only 0.04, much under the screen’s 5.0 limit. This implies Watsco could pay off all existing debt in under a month using present cash flows, giving major financial adaptability and lowering risk in economic declines.

Profit quality, calculated as the 5-year average free cash flow to net income ratio, is at a high 129.41%. This not only exceeds the 75% requirement but shows Watsco creates more cash than accounting earnings, a good sign that profits are supported by real cash creation instead of accounting changes. This sound cash conversion backs dividend distributions, share buybacks, or investment into the business without needing outside funding.

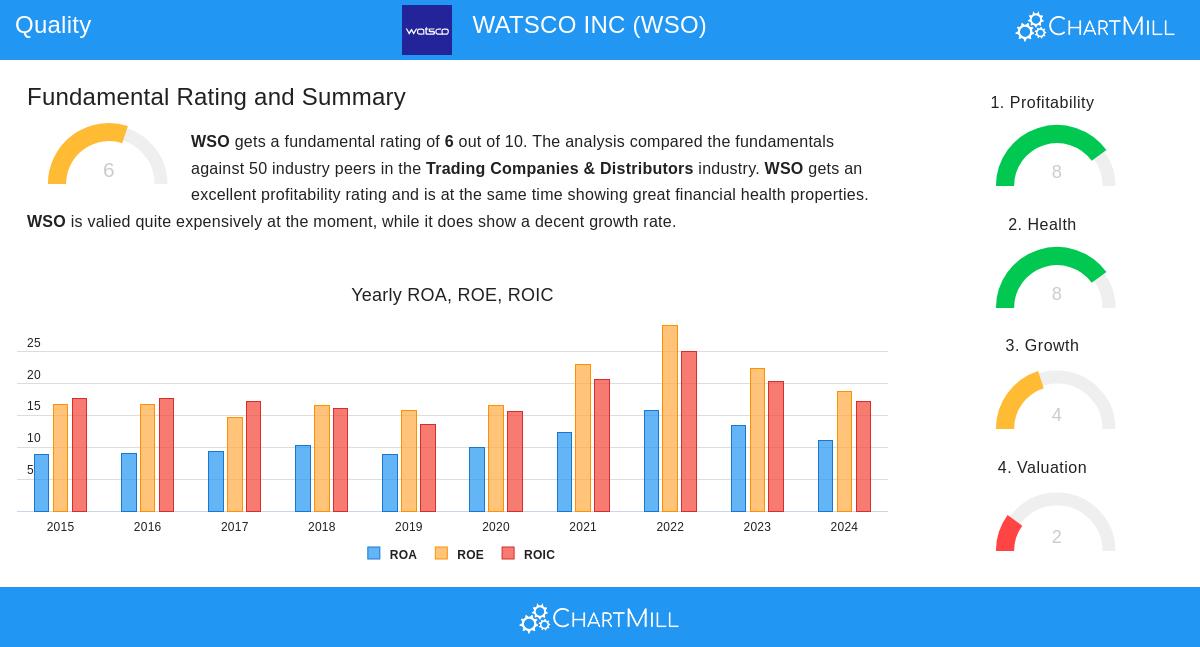

The wider fundamental review report gives Watsco a good rating of 6 out of 10, highlighting excellent results in both financial condition and earnings compared to industry rivals. The business displays high returns on assets and invested capital relative to most competitors, together with better profit margins and a sound balance sheet. While the price seems high on common measures, this is typical for high-grade businesses that have premium prices because of their sound business traits. The complete fundamental review offers more detailed views on these measures and can be seen here.

Outside the numerical elements, Watsco functions in the crucial HVAC-R distribution sector, supplying items and services that have consistent need irrespective of economic situations. The business’s wide distribution system, connections with leading producers, and geographical spread add to its competitive strength. These non-numerical aspects, joined with its financial measures, make it a candidate deserving of more study for investors looking for high-grade assets.

For those wanting to examine other businesses that satisfy the Caviar Cruise conditions, the full screen outcomes can be found here.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any securities. Investors should conduct their own research and consult with a qualified financial advisor before making investment decisions.