Customer experience automation company Verint Systems Inc (NASDAQ:VRNT) offers an interesting case for investors using a value investing strategy. This method, established by Benjamin Graham and famously used by Warren Buffett, involves finding companies trading for less than their intrinsic value. Value investors look for securities where the market price does not completely represent the company's fundamental worth, offering a potential safety buffer. The process centers on detailed fundamental analysis of many areas to find these opportunities.

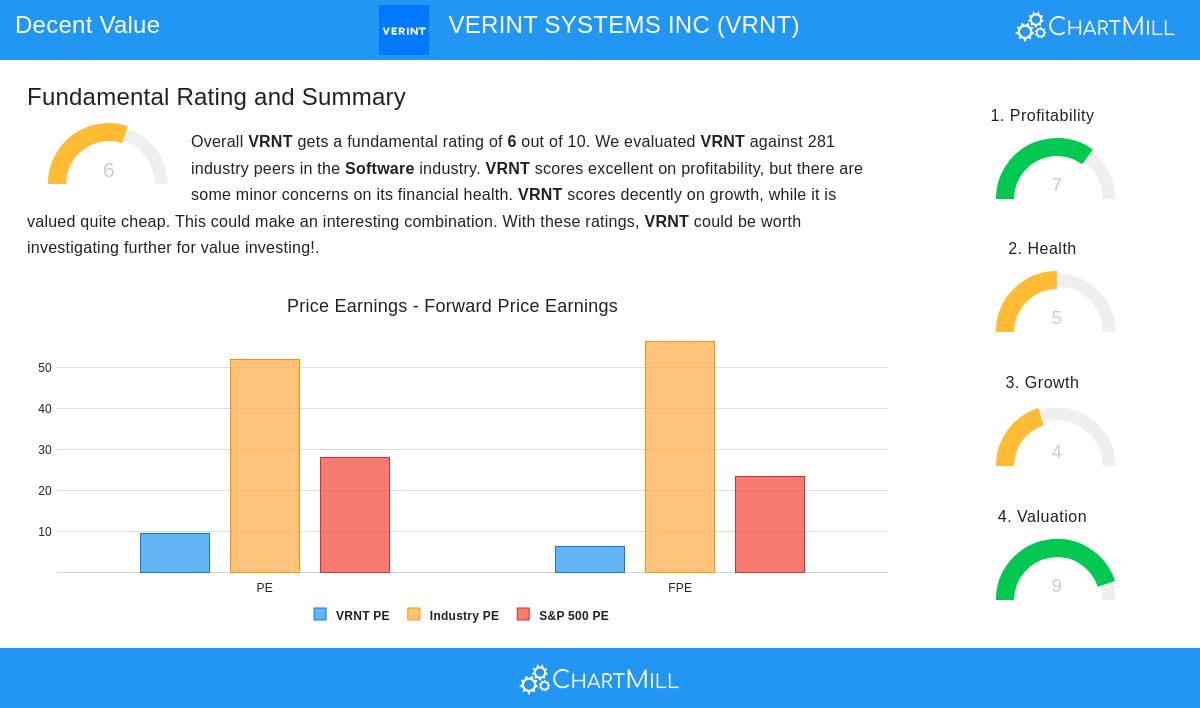

Valuation Measurements

Verint's most notable feature is its appealing valuation measurements, which are the foundation of value investing ideas. The company trades at large discounts on several valuation measures when judged against both industry competitors and wider market indexes.

• Price/Earnings Ratio: 9.43 versus industry average of 51.79 and S&P 500 average of 27.86 • Forward P/E Ratio: 6.18 compared to industry average of 56.37 • Enterprise Value/EBITDA: Within the least expensive 10% of software industry companies • Price/Free Cash Flow: Less expensive than 94.66% of industry rivals

These valuation measurements indicate the market might be placing too low a value on Verint's business fundamentals. For value investors, such reduced multiples offer that important safety buffer Graham highlighted, the difference between market price and calculated intrinsic value that guards against calculation mistakes or unexpected difficulties.

Financial Condition Evaluation

While Verint displays some financial positives, the condition rating of 5/10 shows parts needing thoughtful review. The company's balance sheet presents a mixed picture that value investors should assess carefully.

• Debt Situation: No existing debt, putting Verint in a top position in its sector for debt management • Share Reduction: Steady share buybacks over one and five-year spans • Current Ratio: 0.65 points to possible near-term liquidity issues • Altman-Z Score: 1.22 puts the company in the "distress zone" for bankruptcy risk

The lack of debt is especially significant for value investors, as it lowers financial risk and interest costs. However, the liquidity measurements and Altman-Z score indicate a requirement for close watching of the company's short-term liabilities and general financial soundness.

Profitability Review

Verint's profitability picture shows a more positive view, scoring 7/10 and displaying operational effectiveness that value investors usually look for in undervalued companies. The company sustains good margins and returns that stand up well within the competitive software industry.

• Profit Margin: 5.08%, doing better than 67.62% of industry companies • Operating Margin: 8.80%, higher than 72.95% of rivals • Return on Invested Capital: 4.02%, displaying recent gains • Gross Margin: 69.91% with upward trending movement

These profitability measurements are important for value investors because lasting profits are what finally determine intrinsic value. The improving margin directions and competitive standing suggest the company has operational positives that may not be completely represented in its current market valuation.

Growth Outlook

With a growth rating of 4/10, Verint displays moderate but quickening growth forecasts that value investors could see as acceptable considering the large valuation discount. The company's growth path seems to be moving toward better performance.

• Revenue Growth: Predicted to increase to 6.30% each year • EPS Growth: Estimated to achieve 12.05% yearly growth • Historical Performance: Recent drops showing indications of a turnaround • Growth Quickening: Both revenue and EPS growth rates are getting better

For value investors, sensible growth forecasts paired with large valuation discounts can create interesting opportunities. The expected quickening in both revenue and earnings growth indicates the company might be set for better performance, possibly reducing the difference between market price and intrinsic value as time passes.

Investment Points

Verint Systems represents the kind of opportunity value investors have historically looked for, a company with acceptable fundamentals trading at reduced valuations. The mix of good profitability, no debt, and heavily reduced multiples creates a situation where the market could be undervaluing the company's intrinsic value. However, the financial condition worries, especially about liquidity and the Altman-Z score, justify thoughtful review and emphasize the importance of that safety buffer idea.

The company's position in the customer experience automation market gives contact with the increasing digital transformation movement, while its open platform method and AI-supported solutions provide competitive distinction. As businesses keep focusing on customer engagement technologies, Verint's specialized knowledge could lead to better financial performance.

For investors curious about similar opportunities, our Decent Value Stocks screen frequently finds companies meeting these value investing standards. A more in-depth fundamental analysis of VRNT is accessible for additional study.

Disclaimer: This analysis is based on fundamental data and does not constitute investment advice. Investors should conduct their own research and consider their risk tolerance before making investment decisions. Past performance does not guarantee future results, and all investments carry inherent risks including potential loss of principal.