Peter Lynch’s investment strategy, described in One Up on Wall Street, centers on finding companies with steady growth at fair prices. His method combines growth and value investing, focusing on strong fundamentals, consistent profits, and low debt. The strategy steers clear of overly hyped or rapidly expanding businesses, preferring those with stable, easy-to-understand operations that can grow returns over time. One company that recently appeared in a Peter Lynch-style screen is VIPSHOP HOLDINGS LTD - ADR (NYSE:VIPS), a Chinese e-commerce platform known for flash sales of branded products.

Why Vipshop Matches the Peter Lynch Approach

-

Steady Earnings Growth

Lynch liked companies with reliable earnings growth, usually between 15% and 30% per year. Vipshop’s five-year EPS growth rate of 17.77% fits this range, showing stable progress without signs of unsustainable expansion. While recent earnings have dropped slightly (-8.73% YoY), the long-term trend holds, and analysts expect a small recovery (6.02% forward EPS growth). -

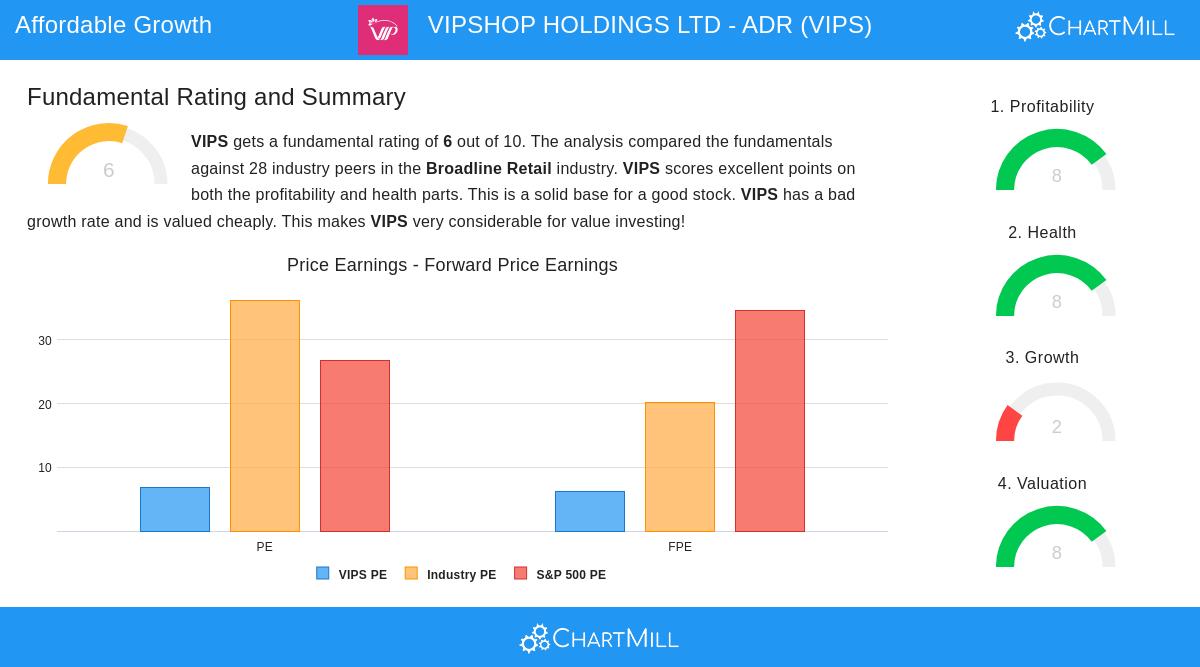

Reasonable Valuation (PEG Ratio ≤ 1)

A key Lynch measure is the PEG ratio, which accounts for growth when evaluating the P/E ratio. Vipshop’s PEG (Past 5 Years) of 0.38 suggests it is undervalued compared to its historical growth, far below Lynch’s ideal of 1. Its current P/E of 6.83 and forward P/E of 6.16 also show it is cheaper than industry peers (average P/E of 36.24) and the S&P 500 (26.73). -

High Profitability (ROE > 15%)

Return on equity (ROE) shows how well a company turns shareholder investments into profits. Vipshop’s ROE of 19.36% beats Lynch’s 15% target and is higher than 78.57% of its broadline retail competitors, indicating good use of capital. -

Low Debt (Debt/Equity < 0.6)

Lynch avoided companies with heavy debt, favoring those with Debt/Equity ratios below 0.6—or better, under 0.25. Vipshop’s ratio of 0.06 means it borrows very little, lowering financial risk. Its Altman-Z score of 3.75 also points to low bankruptcy risk. -

Solid Liquidity (Current Ratio ≥ 1)

The current ratio checks short-term financial health. Vipshop’s ratio of 1.26 meets Lynch’s standard, though it trails some peers. Still, its strong cash flow and minimal debt ease liquidity worries.

Key Strengths and Weaknesses

Our full fundamental analysis gives Vipshop a 6/10, with high scores for profitability (8/10) and financial health (8/10). Key strengths include:

- Strong ROIC (15.30%), showing efficient use of capital.

- Positive free cash flow and a steady dividend yield of 3.04%.

- Share buybacks, which have reduced shares over the past five years.

Challenges include:

- Recent revenue drop (-5.24% YoY), though long-term growth stays slightly positive.

- Lower gross margins (23.49%), below industry norms.

Final Thoughts

Vipshop fits Peter Lynch’s GARP philosophy well: it’s a profitable, undervalued company with controlled growth and little debt. While short-term challenges exist—especially in revenue—its solid fundamentals and very low price make it an interesting pick for long-term investors.

For more stocks that align with the Peter Lynch strategy, check out our pre-built screen here.

Disclaimer: This analysis is not investment advice. Always do your own research or consult a financial advisor before making investment decisions.