VIPSHOP HOLDINGS LTD - ADR (NYSE:VIPS) surfaced in our Peter Lynch-inspired screen, which identifies stocks with sustainable growth and reasonable valuations. The Chinese e-commerce company stands out for its profitability, financial health, and attractive valuation metrics, making it a potential fit for long-term investors seeking growth at a reasonable price (GARP).

Why VIPS Fits the Peter Lynch Strategy

- Strong Historical Growth: VIPS has delivered a 5-year average EPS growth of 17.77%, aligning with Lynch’s preference for companies with steady but not excessive growth.

- Attractive Valuation: With a PEG ratio of 0.37 (well below 1), the stock appears undervalued relative to its earnings growth.

- Healthy Balance Sheet: A debt-to-equity ratio of 0.06 indicates minimal reliance on borrowing, a key factor in Lynch’s strategy.

- Solid Profitability: The company’s return on equity (ROE) of 19.36% reflects efficient use of shareholder capital.

- Liquidity Check: The current ratio of 1.26 suggests sufficient short-term financial stability.

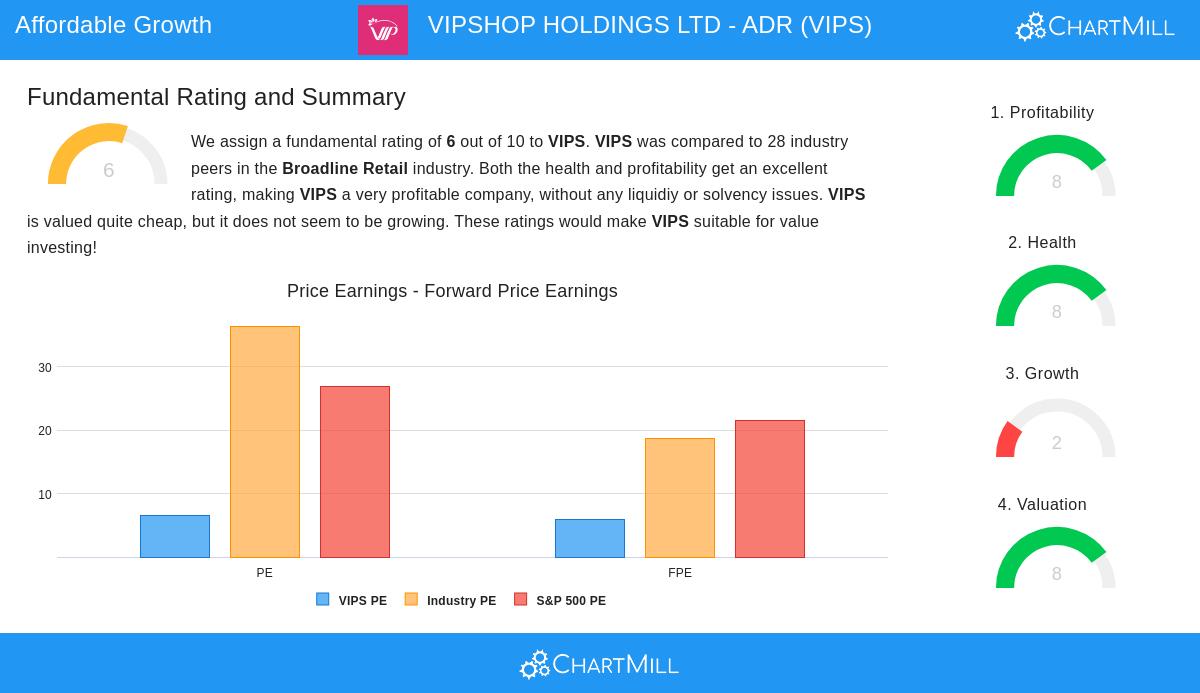

Fundamental Strengths

Our fundamental analysis highlights:

- Profitability: High scores in ROE (19.36%) and ROIC (15.30%) place VIPS ahead of most peers in the broadline retail sector.

- Financial Health: A low debt load and strong cash flow generation reduce bankruptcy risk.

- Valuation: Trading at a P/E of 6.57, VIPS is cheaper than 93% of industry competitors.

Potential Risks

- Slowing Growth: Recent declines in revenue (-5.24% YoY) and EPS (-8.73% YoY) warrant caution.

- Margins: Gross margins (23.49%) lag behind industry averages, though operating margins remain competitive.

For investors drawn to undervalued growth stocks, VIPS presents an intriguing case. The full list of Peter Lynch-style picks can be found in our stock screener.

Disclaimer

This is not investing advice. Always conduct your own research before making investment decisions.