Peter Lynch’s investment strategy, described in One Up on Wall Street, centers on finding companies with steady growth at fair prices. His method combines value and growth investing, focusing on key financial measures like earnings growth, profitability, and financial stability. The strategy steers clear of highly speculative or overly fast-growing firms, preferring those with consistent, controlled growth backed by solid financials. Important benchmarks include a PEG ratio under 1 (showing undervaluation compared to growth), a debt-to-equity ratio below 0.6, and a return on equity exceeding 15%. These factors help identify businesses likely to provide long-term gains without undue risk.

TORM PLC-A (NASDAQ:TRMD), a product tanker firm focused on transporting refined petroleum, stands out as a potential match for Lynch’s criteria. The company’s financials align with many of his key ideas, positioning it as an option for investors looking for growth at a fair price (GARP).

Why TORM PLC-A Matches the Peter Lynch Approach

-

Steady Earnings Growth

- Lynch prefers firms with reliable but not extreme earnings growth. TORM’s 5-year EPS growth of 23.29% fits within Lynch’s preferred range (15–30%), indicating a mix of growth and stability.

- However, recent EPS drops (-40.15% YoY) and expected future declines (-48.86%) call for caution. Investors should evaluate whether this slump is temporary (linked to oil market shifts) or long-term.

-

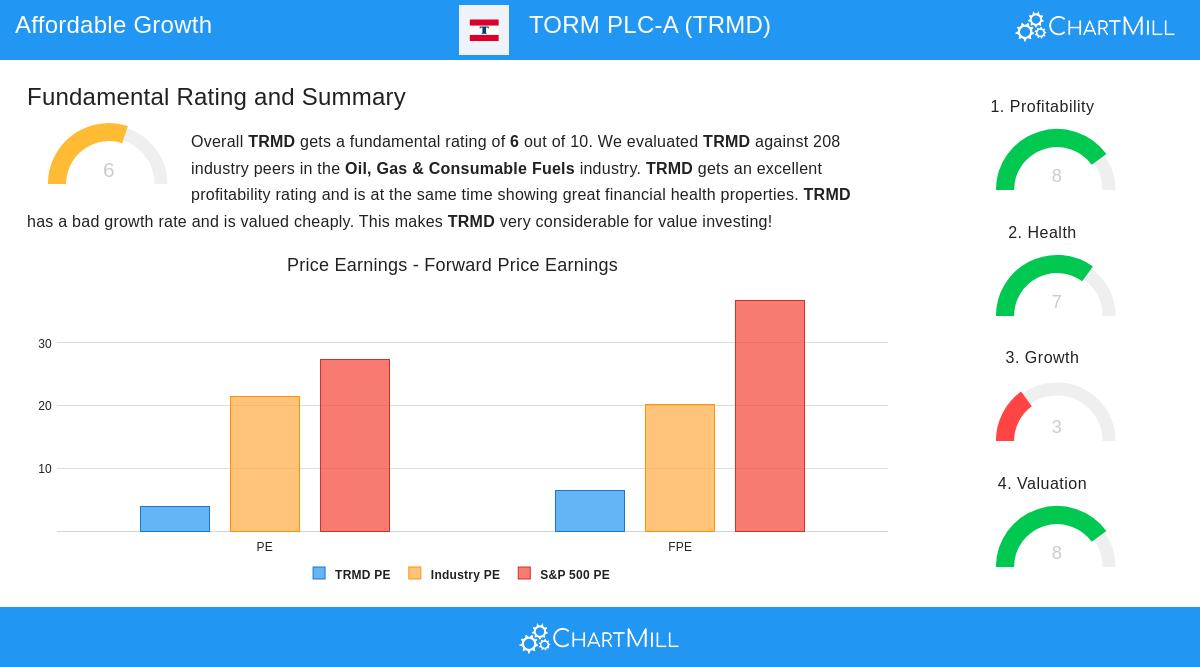

Fair Valuation (PEG Ratio)

- A PEG ratio under 1 suggests a stock may be priced below its growth potential. TORM’s PEG of 0.17 (based on past 5-year growth) is far below Lynch’s benchmark, pointing to notable undervaluation.

- This metric balances the company’s high profitability (ROE of 21.71%, beating 86% of peers) and solid margins (32.2% net margin).

-

Strong Balance Sheet

- Lynch favors minimal debt. TORM’s debt-to-equity ratio of 0.48 is under the screen’s 0.6 limit and near Lynch’s stricter target of below 0.25.

- Liquidity is solid, with a current ratio of 2.55, ensuring short-term debts are easily manageable.

-

Profitability and Efficiency

- The firm’s ROE and ROIC (11.67%) exceed most industry competitors, showing effective capital use—a Lynch priority.

- Operating margins (32.87%) and gross margins (71.15%) rank in the top tier of the oil and gas sector.

Financial Strengths and Concerns

TORM’s fundamental analysis report notes its solid financial health (rating: 7/10) and profitability (8/10), balanced by worries about falling earnings and revenue. Key points:

- Dividend Yield of 21.3% is appealing but unlikely to last with a 119% payout ratio, hinting at possible reductions.

- Valuation is low (P/E of 3.88, below 96% of peers), but earnings forecasts are weak.

- Industry Leadership: TORM scores well in solvency and liquidity metrics within its sector.

Final Thoughts

TORM PLC-A offers a mixed yet interesting case for GARP investors. Its valuation, profitability, and financial strength match Lynch’s ideas, but uncertainty around future earnings requires careful analysis. For investors at ease with cyclical sectors, the stock’s deep discount and high margins could support a long-term holding.

Find More Peter Lynch Screen Picks

For other stocks meeting these standards, check the full Peter Lynch Strategy Screen.

Disclaimer: This article is not investment advice. Do your own research or consult a financial advisor before making investment decisions.