TAYLOR MORRISON HOME CORP (NYSE:TMHC) was identified as a decent value stock by our screening process. The company operates in the residential homebuilding sector, serving markets across 12 U.S. states. With strong profitability metrics and an attractive valuation, TMHC presents a compelling case for value investors.

Valuation

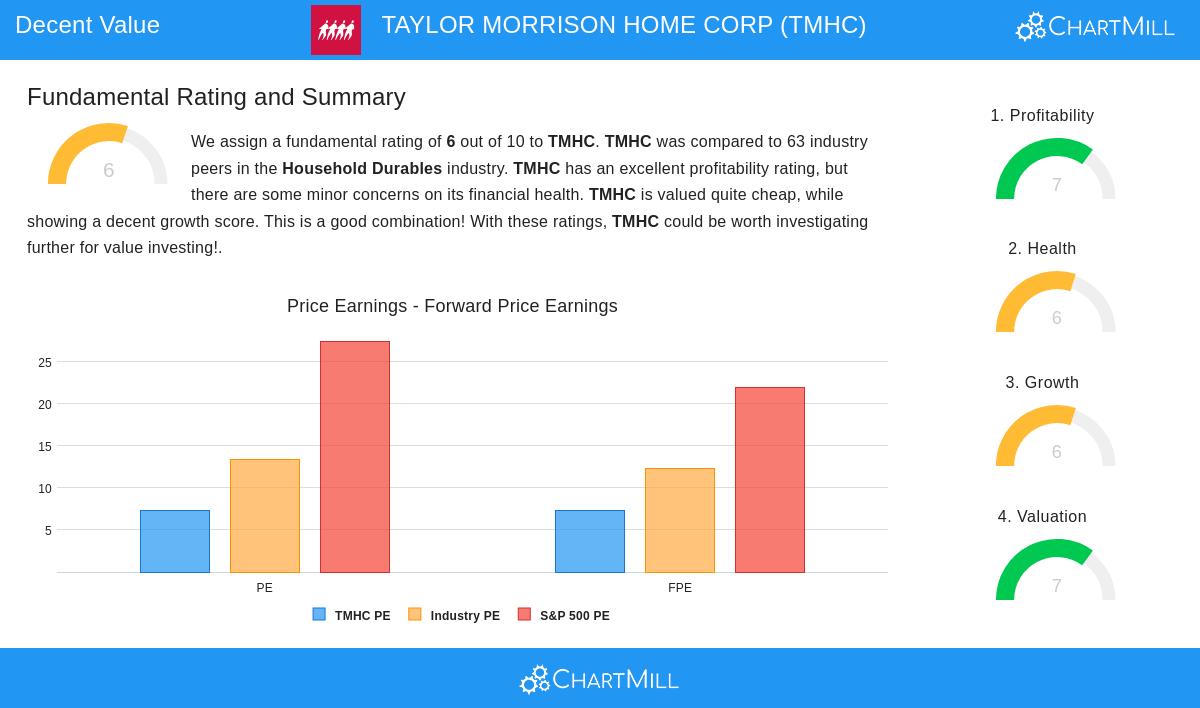

TMHC stands out with a Price/Earnings (P/E) ratio of 7.28, significantly lower than both the industry average (13.36) and the S&P 500 (27.45). This suggests the stock is priced cheaply relative to its earnings. Key valuation highlights:

- Forward P/E of 7.30, indicating continued undervaluation.

- Enterprise Value/EBITDA and Price/Free Cash Flow ratios are also favorable, placing TMHC in the lower-cost segment of its industry.

Profitability

The company earns a Profitability Rating of 7/10, supported by:

- Strong margins: Operating Margin of 15.01% (outperforming 85.71% of peers) and Profit Margin of 10.84% (beating 84.13% of competitors).

- Consistent earnings: Positive earnings and cash flow over the past five years.

Financial Health

TMHC holds a Health Rating of 6/10, with strengths including:

- Solid balance sheet: Debt/Equity ratio of 0.35, indicating manageable leverage.

- Liquidity: Current Ratio of 5.98, well above industry standards.

Growth

While growth is moderating, TMHC still shows resilience:

- Past EPS growth of 23.42% annually and Revenue growth of 11.39%.

- Future EPS growth is projected at 8.92%, though revenue expansion may slow.

Our Decent Value screener lists more stocks with similar characteristics. For a deeper dive, review the full fundamental report on TMHC.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should conduct your own analysis before making investment decisions.