Simpson Manufacturing Co Inc (NYSE:SSD) stands out as a potential candidate for investors seeking long-term growth at a reasonable price. The company, which specializes in building and construction solutions, meets several key criteria outlined in Peter Lynch’s investment strategy.

Why SSD Fits the GARP Approach

- Strong Earnings Growth: SSD has delivered a 5-year average EPS growth of 20.59%, aligning with Lynch’s preference for sustainable but not excessive growth.

- Reasonable Valuation: The stock’s PEG ratio of 0.97 (below 1) suggests it is reasonably priced relative to its growth trajectory.

- Healthy Financials: With a debt-to-equity ratio of just 0.19 and a current ratio of 3.17, the company maintains a solid balance sheet.

- Profitability: SSD’s return on equity (ROE) of 17.44% reflects efficient use of shareholder capital, exceeding many industry peers.

Fundamental Highlights

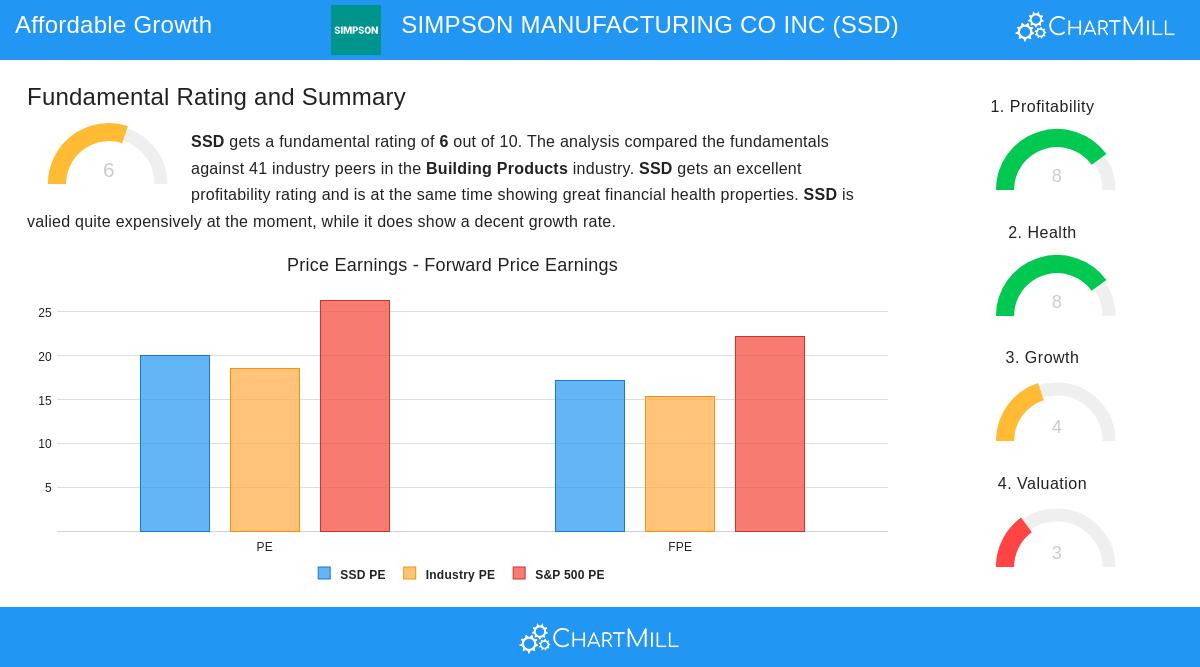

SSD’s financial health is robust, with strong margins and consistent profitability. The company’s operating margin of 19.63% outperforms 85% of its industry peers, while its gross margin of 46.12% ranks among the best in the sector. Though its valuation appears slightly expensive based on P/E ratios, its growth metrics and financial stability justify the premium.

For a deeper dive into SSD’s fundamentals, review the full analysis here.

Our Peter Lynch Strategy screener provides more stocks that fit this disciplined investment approach.

Disclaimer

This is not investing advice. The observations here are based on current data, but investors should conduct their own research before making decisions.