Roku and Amazon Ads: A Game-Changer or a Fleeting Hype?

Roku (NASDAQ: ROKU) surged over 10% on June 16, 2025, following news of a new strategic partnership with Amazon Ads. This reaction wasn’t purely speculative, it was the market pricing in a potentially pivotal development in Roku’s trajectory.

But what does this mean for long-term investors like myself?

Let’s dig deeper into the fundamentals, evaluate the recent deal, and analyze Roku’s strategic position, including both strengths and vulnerabilities.

The Amazon Deal: A Closer Look

On June 16, Roku and Amazon Ads jointly announced an exclusive integration giving advertisers access to the largest authenticated Connected TV (CTV) footprint in the U.S. via Amazon DSP. In simple terms, this means advertisers can now deterministically target logged-in users across both Roku and Amazon’s platforms, reaching over 80 million U.S. households.

Key highlights:

-

40% more unique viewers reached in early tests with 30% lower ad frequency overlap.

-

The deal enables full-funnel performance tracking and better return on ad spend (ROAS).

-

Available to advertisers using Amazon DSP starting Q4 2025.

Why it matters:

CTV advertising is exploding, but its Achilles heel has been fragmented identity tracking and limited ad performance data. This deal bridges that gap. Roku, which already controls about half of U.S. streaming hours, is now aligned with Amazon’s unparalleled e-commerce data and advertising muscle.

As Bloomberg Intelligence puts it, this helps Roku scale more effectively in a “very competitive and fragmented” CTV ad market .

Business Fundamentals: Strong Core, but Still a Work in Progress

Highlights from Q1 2025: Q1 Shareholder Letter

-

Total Revenue: $1.02 billion (+16% YoY)

-

Platform Revenue: $881 million (+17% YoY)

-

Gross Profit: $445 million (+15% YoY)

-

Streaming Hours: 35.8 billion (+17% YoY)

-

The Roku Channel: Now the #2 most engaged app on Roku in the U.S.

Roku continues to shift its business model toward high-margin platform revenues (ads + subscription billing), while device sales (though still meaningful) generate losses due to aggressive pricing strategies.

Positives:

-

Free Cash Flow: $298 million over the last 12 months

-

Platform Gross Margins: ~52.7%

-

New revenue streams: Shoppable ads (e.g. “Roku Recipes”) and AI-powered content suggestions

Cautions:

-

Operating losses remain substantial (-$57.7 million in Q1)

-

Hardware margins remain deeply negative

-

Competition from Amazon Fire TV, Apple TV, and smart TV manufacturers is fierce

Risks and Vulnerabilities

1. Platform Dependency and Ecosystem Control

Roku’s primary competitive edge lies in its control of the TV operating system. But unlike Apple or Amazon, it doesn't own the broader ecosystem (e.g., hardware, content, and retail). It relies heavily on ad revenue and partner platforms, which can become a strategic bottleneck if partners shift priorities.

2. Rising Competition

Amazon and Google are deeply embedded in the CTV space. Roku’s edge lies in its user interface, ad tech, and first-mover advantage, but that moat could shrink rapidly. If OEMs like Samsung or LG improve their native OS or if Amazon pushes Fire OS more aggressively, Roku could face share erosion.

3. Device Segment Drag

Roku’s devices segment consistently posts losses (e.g., -$19M gross profit in Q1 2025), a trend unlikely to reverse soon. While these losses may be strategic (growing the install base), they weigh on the bottom line and limit near-term profitability.

4. Ad Market Volatility

CTV ad budgets are sensitive to macro conditions. While Roku is outperforming broader OTT trends, a downturn in ad spending could hurt its platform revenue, especially as it still operates at an adjusted EBITDA margin of just 5.5%.

The Long-Term Investment Case

Why We Remain Interested (but Cautious):

For long-term investors, Roku presents a compelling story:

-

Secular tailwinds: Cord-cutting and the rise of ad-supported streaming are irreversible trends.

-

Platform leverage: The ad platform is becoming more sophisticated, especially with data partnerships like Amazon DSP and Adobe.

-

Strategic flexibility: Acquisitions like Frndly TV point to a long-term vision of bundling and owning more of the value chain.

Yet we should be honest about the risks. Roku’s lack of profitability, continued reliance on partners, and competitive threats from tech giants are significant. The company has the tools to succeed but must execute flawlessly to justify a long-term position.

Verdict on the Amazon Deal

This deal is not just marketing fluff. It’s a real, strategic catalyst that strengthens Roku’s position in three critical ways:

-

Reach: Extends advertiser access to one of the largest authenticated TV audiences in the U.S.

-

Targeting Precision: Amazon's data graph brings unparalleled ad targeting to Roku’s platform.

-

Measurement and ROI: Improved attribution is key for winning performance-driven ad dollars.

This could unlock new demand for Roku ad inventory, improve ROAS, and reduce churn among advertisers, all while making Roku more appealing to both SMBs and enterprise brands.

But the impact will be gradual. The integration rolls out in Q4 2025, and the full financial effects might only show in 2026 and beyond. In the meantime, Wall Street will expect consistent execution and improved profitability.

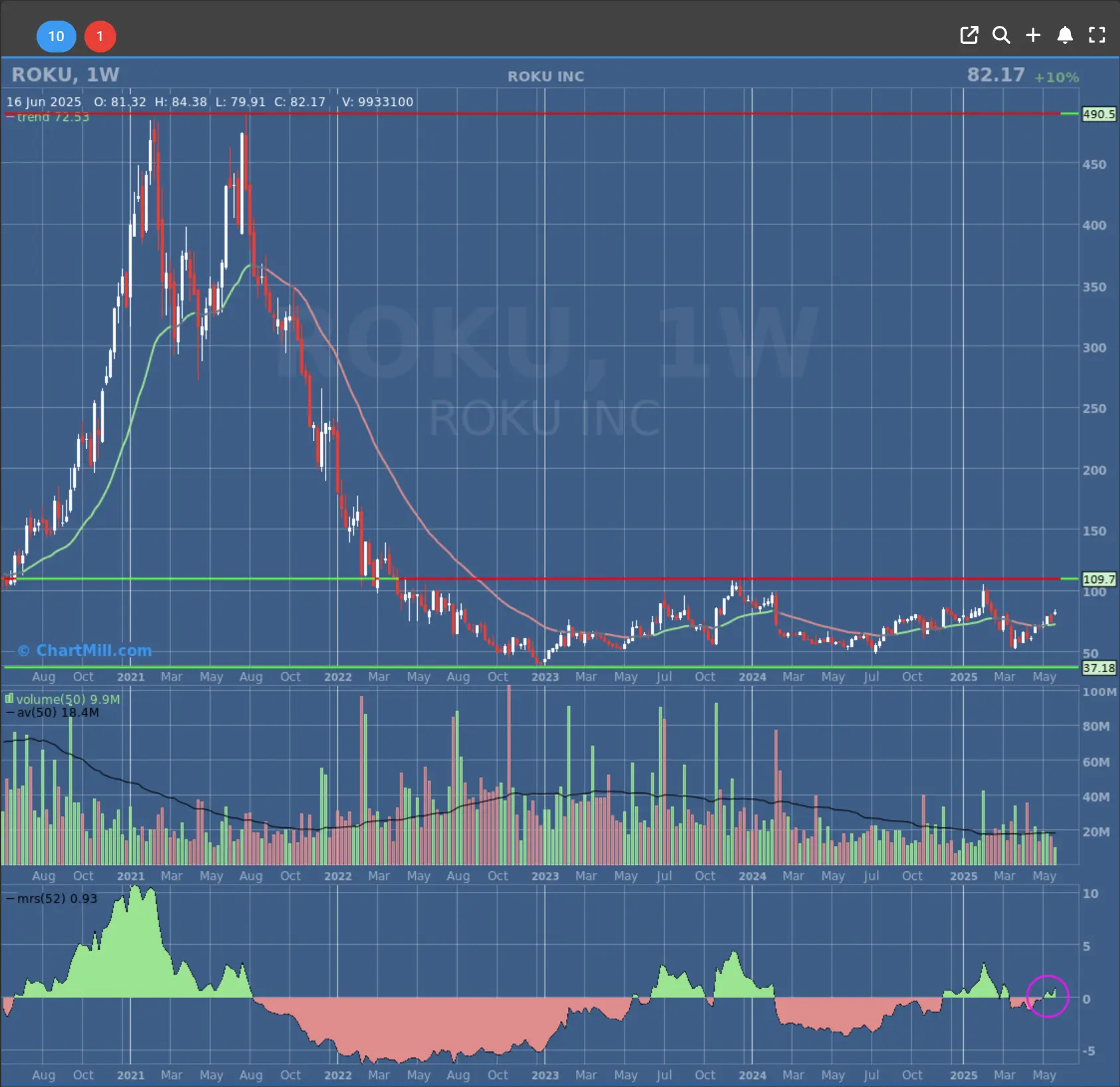

A View on Technicals, the Weekly Chart

Roku’s long-term weekly chart shows signs of a potential turnaround after a prolonged downtrend from its 2021 highs. Over the past two years, the stock has been forming a broad base between roughly $57 and $110. This type of consolidation pattern often precedes a longer-term reversal if confirmed by a breakout.

The recent move up to $82.17, along with a 10% weekly gain following the Amazon Ads partnership news, suggests renewed investor interest. Volume is starting to pick up modestly, indicating possible early accumulation.

Importantly, the Mansfield Relative Strength (RS) indicator, which compares Roku’s performance to the S&P 500, has turned positive again. This shift means Roku is beginning to outperform the broader market, which is often an early signal in long-term trend reversals.

To confirm a true breakout and long-term uptrend, Roku would need to convincingly clear the $110 resistance level on strong volume. Until then, it remains in a constructive base-building phase.

For long-term investors, this setup is promising, but patience is still required, as the breakout above the long term resistance level hasn’t happened yet.

Final Thoughts

Roku’s collaboration with Amazon Ads is a powerful step forward, not just tactically but strategically. It signals that Roku remains relevant and innovative in a space increasingly dominated by trillion-dollar players. For long-term investors, this enhances the bull case, but doesn’t eliminate the risks.

Roku still needs to improve operational efficiency, monetize international growth and make its hardware segment less of a financial drag.

As a long-term investor with a focus on secular growth trends and durable moats, Roku deserves a spot on the watchlist, if not a small allocation in a diversified portfolio.

We’ll be watching Q3 and Q4 earnings closely to confirm that this Amazon partnership is translating into real numbers.

Walter Shares, ChartMill