In value investing, finding stocks that trade below their intrinsic value while having good basic fundamentals is a key strategy. This method, based on the ideas of Benjamin Graham and later made famous by Warren Buffett, aims to find chances where the market might have incorrectly priced a security because of near-term feelings or neglect. One way to simplify this hunt is by using fundamental ratings that judge companies on important areas like valuation, financial condition, earnings, and expansion. A stock that gets a high mark on valuation, meaning it might be inexpensive compared to others, while also showing good marks in condition, earnings, and expansion, could be an interesting pick for value-focused investors. RIGEL PHARMACEUTICALS INC (NASDAQ:RIGL) appears from this kind of screening, showing traits that may deserve more examination from those following this strict investment approach.

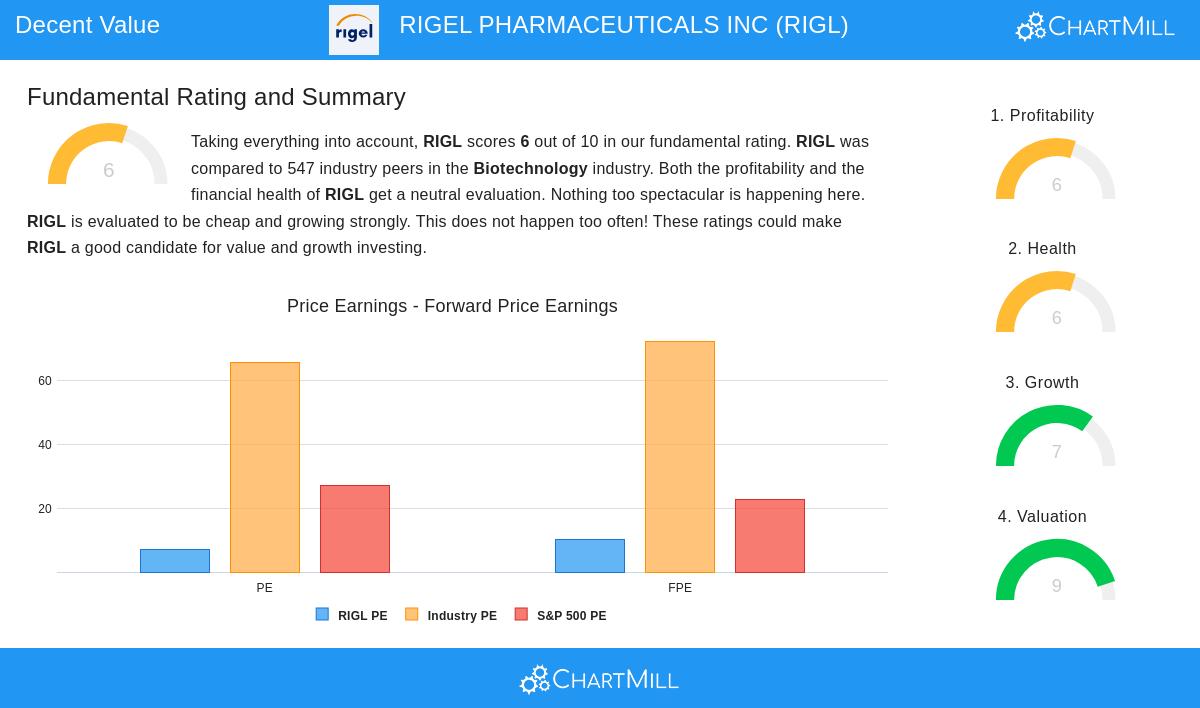

Valuation Strengths

Rigel Pharmaceuticals is notable in the valuation group, getting a strong score of 9 out of 10. This is especially important for value investors, since a good valuation is frequently the main starting point for such plans, it hints the stock might be priced under its inherent value, offering a possible safety buffer. Important numbers back this view: the company's Price/Earnings ratio of 7.18 is not only much under the industry average but also notably lower than the S&P 500's average, suggesting the market might be underestimating its earnings ability. In the same way, the Price/Forward Earnings ratio of 10.08 and Enterprise Value to EBITDA numbers further support that RIGL is trading at a lower price than most others in the biotechnology field. For value investors, these numbers are key because they lower the danger of paying too much for assets and raise the chance of value gains as the market fixes its pricing with time.

Financial Condition and Earnings

While valuation gets first notice, lasting investment needs a company to be financially secure and profitable, points that lessen the danger of value traps and confirm operational steadiness. Rigel's financial condition rating of 6 shows a varied but mostly okay standing. On the good side, the company shows a sound current ratio of 2.02, meaning enough cash to cover near-term debts, and its debt amounts are workable, with a Debt to FCF ratio of 0.91 hinting at solid free cash flow to handle liabilities. Still, an Altman-Z score of -2.06 brings some worry, as it indicates financial strain compared to industry standards; this is somewhat balanced by the point that this score is similar to many biotechnology peers, which often work with higher risk levels because of R&D needs. Earnings, rated at 6, displays notable strong points: Return on Assets (47.32%), Return on Equity (119.39%), and Profit Margins (36.51%) all place in the top parts of the industry, pointing to efficient use of money and good profit creation. These parts are important for value investors, as they hint the company is not just inexpensive but also basically able to maintain and build its operations, lowering the risk that low valuation comes from permanent fall.

Expansion Path

Expansion is another needed piece for value plans, as it backs the idea that inherent value might rise with time, leading to price gains. Rigel's expansion rating of 7 is supported by outstanding past results and good future outlooks. Revenue increased by 105.62% over the last year, with an average yearly growth rate of 24.77% in recent years, while Earnings Per Share jumped by 729.07%, a strong sign of speeding operational wins. Looking forward, analysts predict continued expansion with EPS expected to rise by 29.86% each year and revenue by 14.40%. For value investors, this expansion story is key because it offers a reason for the market to reprice the stock higher, closing the distance between current price and inherent value. It also fits with the thought that underpriced companies with good expansion possibilities are more likely to give large returns as their promise is achieved.

Conclusion and Further Research

Rigel Pharmaceuticals offers a detailed profile that fits well with value investing measures: greatly underpriced based on earnings numbers, financially steady with some notes, very profitable compared to peers, and backed by energetic expansion patterns. Investors should note, though, that the biotechnology field has built-in risks, like regulatory blocks and pipeline reliabilities, which call for complete personal checking. The company's focus on treatments for blood disorders and cancer, with sold products like TAVALISSE and REZLIDHIA, adds a bit of speculative interest but also highlights the need to watch clinical and business progress. For those wanting to find like chances, more stocks fitting this "Decent Value" profile can be located using this screening tool.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consult with a financial advisor before making any investment decisions.