Dividend investors often look for a balance between high yield, sustainability, and financial stability. One way to find such stocks is by using a screening method that focuses on a high ChartMill Dividend Rating while checking the company’s profitability and financial health. This approach helps remove companies with unsustainable payouts or weak finances. ROBERT HALF INC (NYSE:RHI) appears as a stock worth considering under this method, offering a good mix of yield, growth, and stability.

Dividend Strength: High Yield and Steady Growth

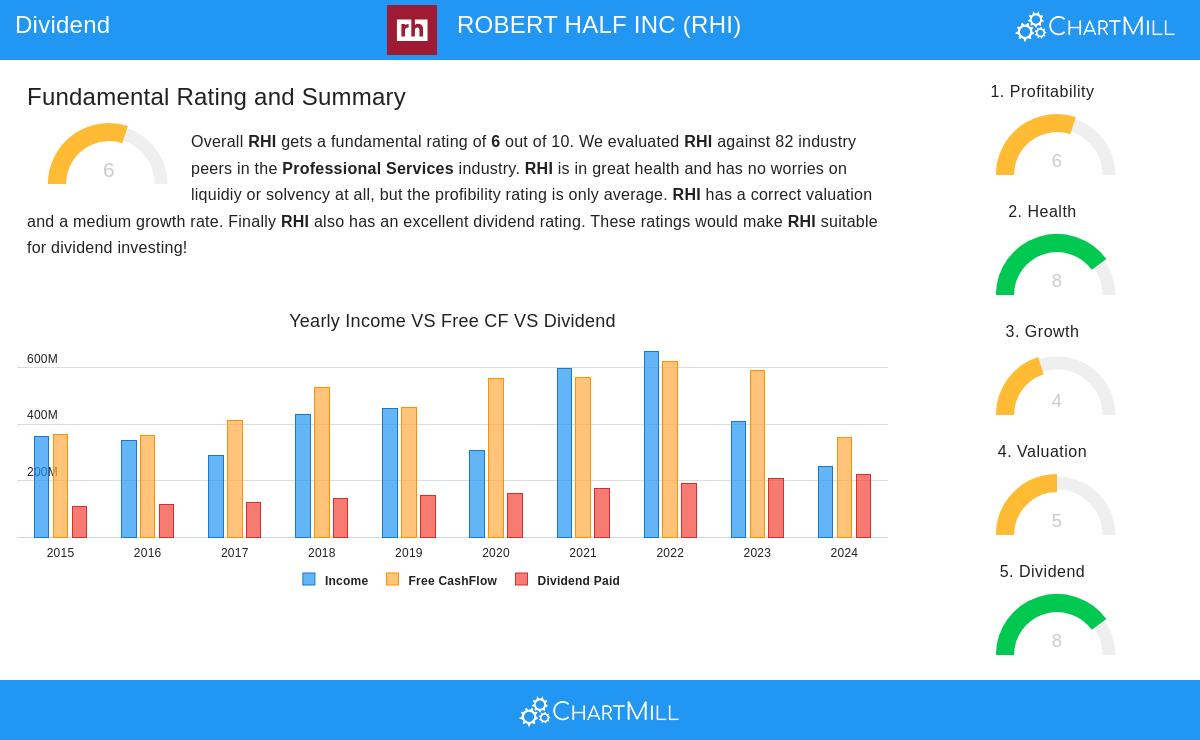

RHI stands out with a 5.57% dividend yield, well above the industry average (2.11%) and the S&P 500’s 2.36%. This makes it appealing for income-focused investors. However, yield is only part of the story—sustainability is key. Here, RHI performs well:

- Steady Growth: The dividend has increased at an annual rate of 11.32% over the past five years, showing management’s focus on shareholder rewards.

- Long History: The company has paid dividends for at least 10 straight years without cuts, a sign of dependability.

The main concern is the payout ratio of 109.23%, which is higher than earnings. While this raises questions about sustainability, RHI’s strong balance sheet (discussed below) and expected earnings growth (28.18% annually) could help bring the ratio down.

Profitability: Solid but Could Be Better

RHI’s Profitability Rating of 6/10 shows average but acceptable metrics for a dividend stock:

- ROIC (11.26%) and ROE (15.63%) are better than most peers, indicating efficient use of capital.

- Margins have dipped recently, with operating margins at 4.22% (similar to the industry). This needs watching, but the company’s history of positive cash flow supports continued dividends.

Financial Health: A Stable Base

With a Health Rating of 8/10, RHI’s balance sheet is a strong point:

- No Debt: Unlike many peers, RHI has no debt, avoiding interest costs and bankruptcy risk.

- Liquidity: A current ratio of 1.65 and quick ratio of 1.65 show enough short-term asset coverage.

- Altman-Z Score (4.51): This indicates low bankruptcy risk, putting RHI in the top tier of its industry.

Valuation and Growth Outlook

RHI trades at a forward P/E of 14.73, lower than the S&P 500 (37.54) and most peers. While past revenue and earnings have slowed, analysts expect a rebound:

- EPS Growth: Projected to rise to 28.18% annually, easing payout ratio worries.

- Revenue Growth: Forecast at 8.52%, suggesting room for dividend increases.

Conclusion

RHI’s high yield, steady growth, and debt-free balance sheet make it a strong choice for dividend investors. While the high payout ratio is a concern, improving earnings and solid finances provide support. For those seeking income with moderate risk, RHI deserves closer review.

Find More Dividend Ideas: For other screened results, visit the Best Dividend Stocks screener.

Disclaimer: This article is not investment advice. Do your own research or consult a financial advisor before making decisions.