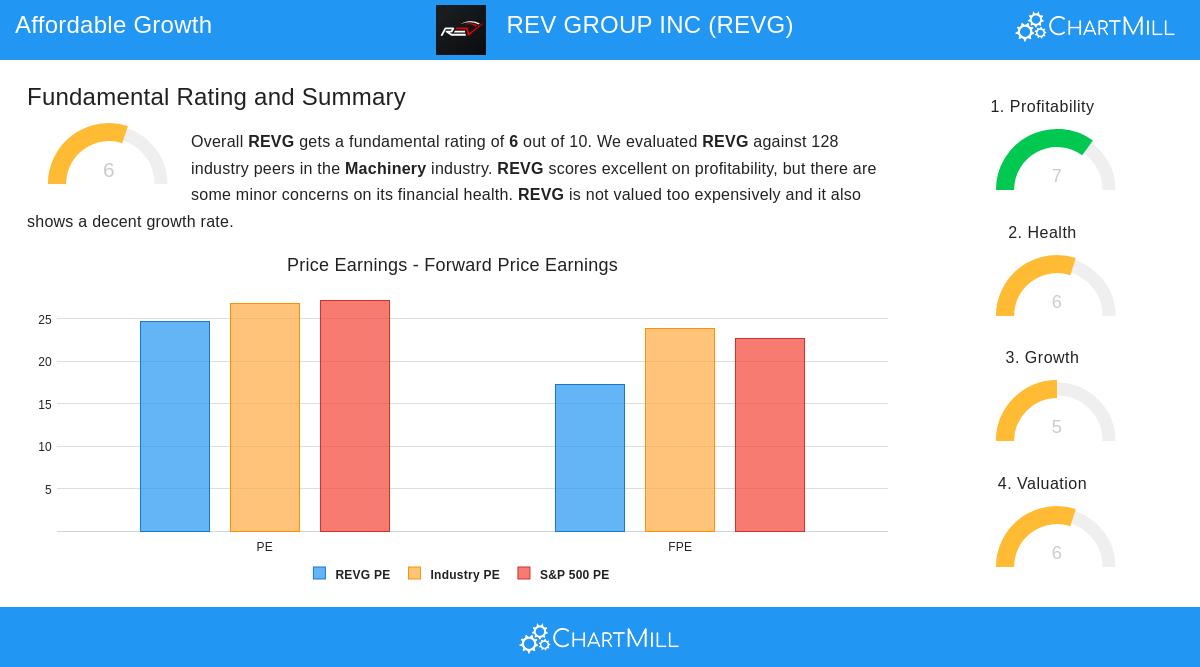

REV Group Inc (NYSE:REVG) has been identified as a candidate through a screening process based on Peter Lynch's investment philosophy, which highlights finding companies with lasting growth paths trading at sensible prices. Lynch's method, described in his book One Up on Wall Street, centers on basic measures that mix growth possibility with financial condition, steering clear of excessively promoted stocks in favor of businesses with clear operations and sound finances. This system favors companies that are not only expanding but doing so in a controlled manner, with good earnings and careful debt.

Growth and Valuation Measures

REVG displays a number of traits that match Lynch’s plan, especially regarding profit growth and price assessment. The company’s past results and future projections indicate it matches the "growth at a sensible price" (GARP) model that Lynch liked. Important measures include:

- EPS Growth (5-Year): 29.36%, inside Lynch’s ideal span of 15–30%, showing maintained instead of extreme growth.

- PEG Ratio: 0.84, under the key level of 1, suggesting the stock could be priced low compared to its growth path.

- Return on Equity (ROE): 27.89%, much higher than the 15% lowest Lynch advised, showing good use of shareholder equity.

- Debt-to-Equity Ratio: 0.23, easily under Lynch’s chosen top level of 0.25, showing a careful capital setup.

- Current Ratio: 1.63, above the lowest need of 1, which indicates enough short-term cash availability.

These measures are key to Lynch’s plan because they help find companies that are financially sound, profitably growing, and not overvalued, lowering investment risk while still gaining from growth possibility.

Basic Condition Summary

An examination of REVG’s wider basic condition, as explained in the full analysis here, backs the screening outcomes. The company receives a good total score, with specific strong points in earnings and ability to pay debts. Its return on invested capital (ROIC) of 18.41% scores well within the machinery field, and it has shown better profit margins and lower share counts in recent years. Still, there are small issues with cash ratios next to field competitors, and sales growth has been steady in the past, though experts predict faster movement in both sales and profits going ahead. Dividend investors might see the payout as fairly small, but the company’s attention on reinvestment and growth matches Lynch’s focus on building returns.

Field Standing and Forecast

REVG works in the specialty and recreational vehicles industry, producing items from fire trucks and ambulances to RVs. This variety across necessary and consumer areas offers some steadiness, while the company’s well-regarded collection of brands—including names like American Coach and E-ONE—highlights its market position. With experts predicting yearly EPS growth above 36% in upcoming years, the company seems set to carry on a growth course that does not depend on high debt or danger, matching Lynch’s requirements of clear, consistently growing businesses.

For investors curious about reviewing other companies that satisfy Peter Lynch’s investment rules, you can view the full screen here.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consider their financial situation and risk tolerance before making investment decisions.