REV Group Inc (NYSE:REVG) surfaced in our Peter Lynch-inspired screen, which identifies companies with strong growth potential at reasonable valuations. The manufacturer of specialty and recreational vehicles demonstrates solid fundamentals, making it a candidate for long-term investors seeking growth at a reasonable price (GARP).

Why REVG Fits the GARP Approach

- Earnings Growth: REVG has delivered a 5-year average EPS growth of 29.4%, comfortably within Lynch’s preferred range of 15-30%. This suggests sustainable expansion rather than overheated growth.

- Attractive Valuation: With a PEG ratio (5Y) of 0.72, well below the ideal threshold of 1, the stock appears undervalued relative to its earnings growth.

- Strong Profitability: The company’s return on equity (ROE) stands at 27.1%, significantly above the 15% minimum Lynch favored, indicating efficient use of shareholder capital.

- Healthy Balance Sheet: A debt-to-equity ratio of 0.36 reflects conservative financing, aligning with Lynch’s preference for companies with manageable leverage.

- Liquidity Position: The current ratio of 1.66 suggests REVG can comfortably cover short-term obligations, reinforcing financial stability.

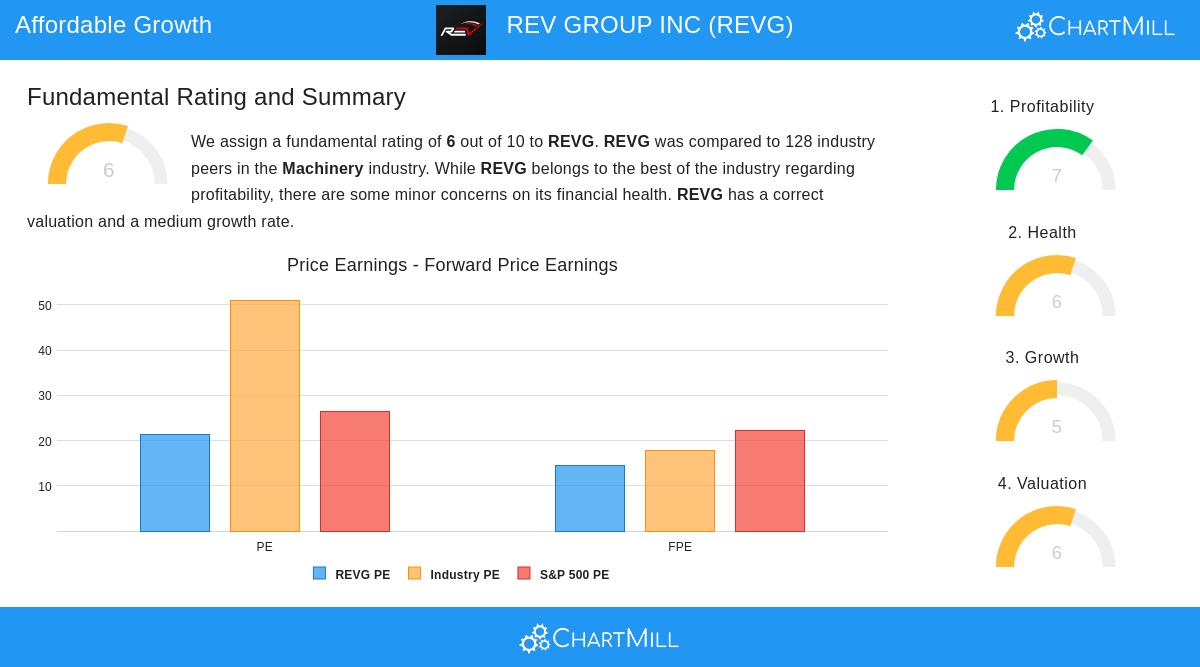

Fundamental Snapshot

Our fundamental analysis report assigns REVG a rating of 6/10, noting strengths in profitability and valuation but flagging minor concerns in liquidity metrics. Key takeaways:

- Profitability: High ROE (27.1%) and improving margins signal efficient operations.

- Valuation: While the P/E ratio (21.2) appears elevated, the low PEG ratio justifies the premium given expected earnings growth.

- Financial Health: A solid Altman-Z score (4.38) and manageable debt levels reduce bankruptcy risk.

Final Thoughts

REVG’s combination of steady earnings growth, reasonable valuation, and strong profitability makes it a compelling option for GARP-focused investors. While revenue growth has been sluggish recently, improving margins and a favorable industry outlook could support future performance.

For more stocks matching this strategy, explore our Peter Lynch Screen.

Disclaimer

This is not investing advice. Always conduct your own research before making investment decisions.