Market Monitor News June 02 (Ulta Beauty, ZScaler UP - GAP, Regeneron DOWN)

By Kristoff De Turck - reviewed by Aldwin Keppens

Last update: Jun 2, 2025

Wall Street Wraps Up Strong May with Caution as Trade Tensions Resurface

A Cautious Finish to a Strong Month

U.S. stock markets closed the final trading session of May on a mixed note. The S&P 500 slipped slightly, the Dow Jones edged up by 0.1%, and the Nasdaq declined by 0.3%.

Despite the hesitation at the end, May delivered exceptional results overall, the S&P 500 gained more than 6%, marking its best May since 1990, while the Nasdaq climbed over 9%.

Still, the major indices remain just below their record highs, with fresh concerns over global trade policy keeping investors on edge.

The “TACO Trade” and Trade Tensions

Renewed friction between the U.S. and China dominated headlines once again. President Donald Trump accused China of violating a recent trade truce that included temporary tariff reductions.

In a sharp statement on Truth Social, he declared that China had "completely broken" the agreement and that he was done playing "Mr. Nice Guy."

That comment sent markets lower earlier in the day, but stocks recovered somewhat after Trump expressed optimism about future talks with Chinese President Xi Jinping. This back-and-forth dynamic has been dubbed the “TACO trade”, short for "Trump Always Chickens Out", a reference to the belief that the president often retreats from aggressive policies under market pressure.

Meanwhile, the administration is reportedly considering expanding export restrictions on Chinese tech firms, potentially increasing friction.

Earlier this week, a U.S. judge briefly blocked Trump's tariffs, though the ruling was swiftly overturned by the White House.

Economic Data Sends Mixed Signals

On the economic front, data released Friday was mixed.

-

The core PCE inflation rate, the Federal Reserve’s preferred inflation measure, cooled to 2.5% in April from 2.7% in March. Headline inflation came in at 2.1%, with both monthly figures rising just 0.1%.

-

Personal incomes rose by 0.8% in April, well above the 0.3% expected, while consumer spending increased by 0.2%, matching forecasts.

-

A preliminary trade report showed a sharp narrowing of the U.S. trade deficit by 46% to $87.6 billion.

-

The Chicago PMI dropped to 40.5 from 44.6, suggesting deepening weakness in Midwest manufacturing.

-

Consumer confidence showed slight improvement in May, according to the University of Michigan, though the survey was completed before the latest trade flare-ups.

-

Inflation expectations also eased somewhat. Yet many consumers remain uneasy about the future, with 83% of CEOs in a Conference Board poll predicting a recession within 12 to 18 months.

Standout Stocks: Winners and Losers

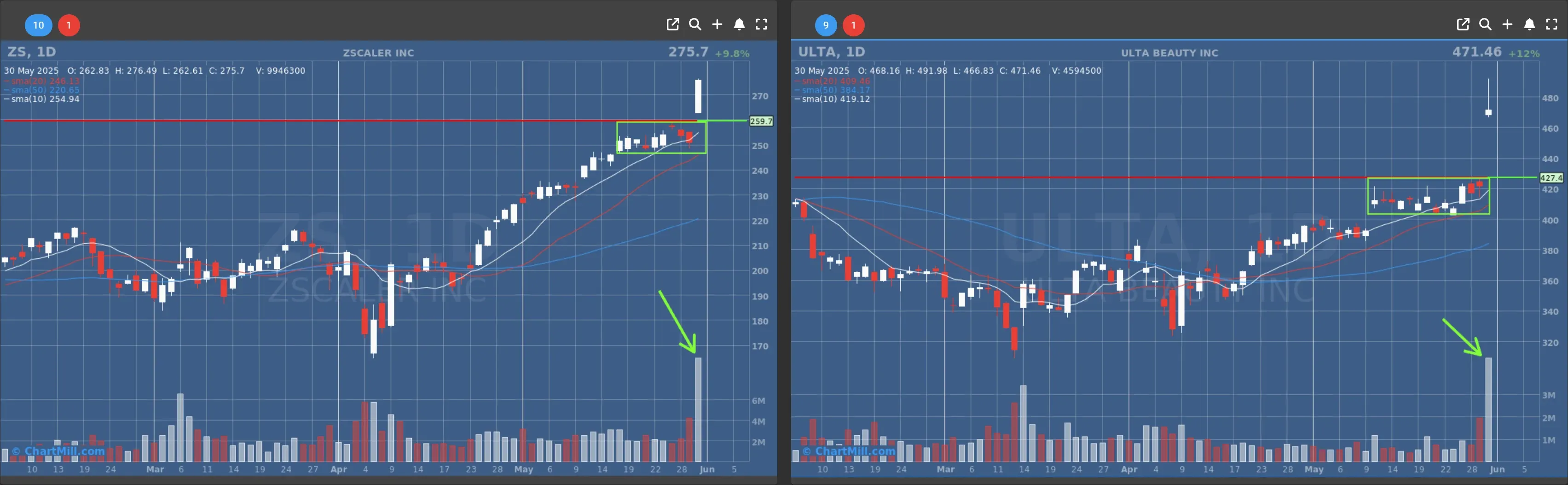

Ulta Beauty (ULTA | +11.78%) surged after the beauty retailer beat revenue expectations and raised its full-year forecast. CEO Kecia Steelman noted that spending on beauty remains strong as a form of escape during economic uncertainty.

ZScaler (ZS | +9.79%) also impressed, with better-than-expected quarterly revenue and an improved outlook.

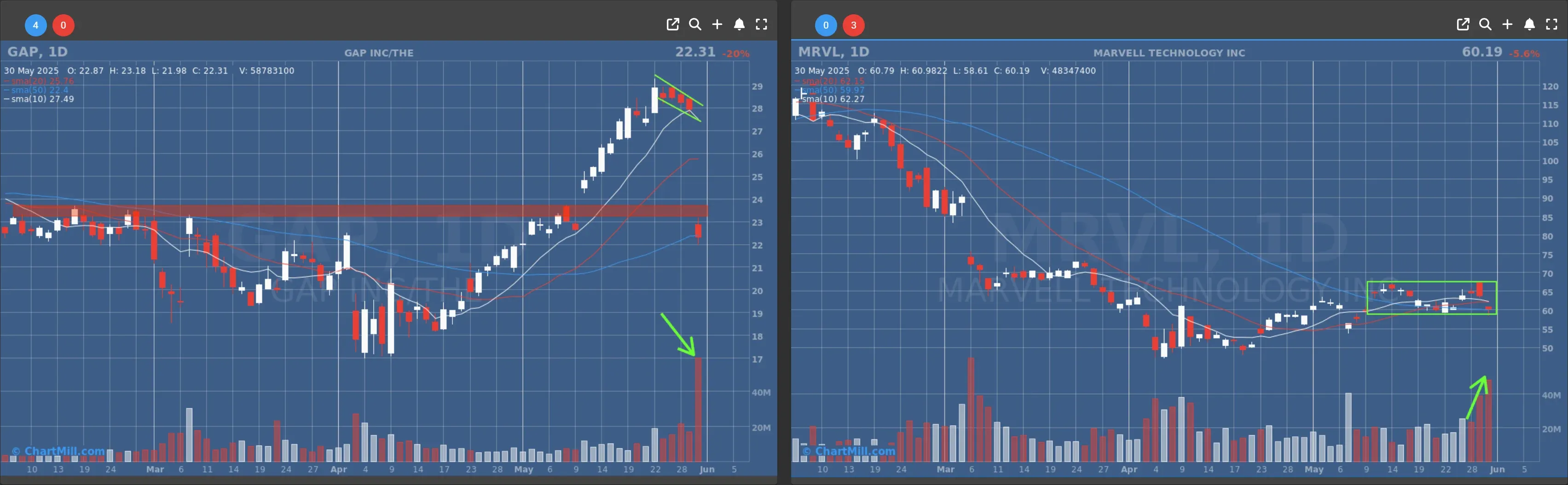

In contrast, Gap (GAP | -20.18%) posted its biggest single-day drop in three years. Although earnings and revenue beat expectations, the company warned that tariffs could cost up to $300 million.

Marvell Technology (MRVL | -5.55%), despite solid AI-driven growth and a 63% increase in revenue, disappointed investors with a cautious forecast and lower-than-expected gross margins.

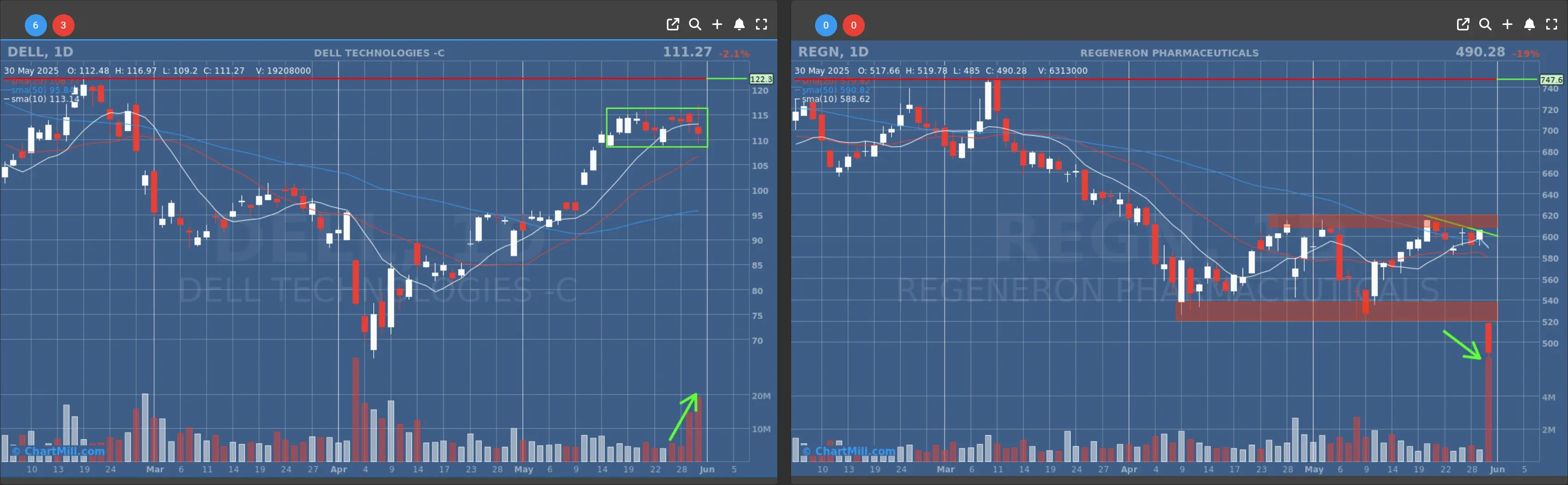

Dell Technologies (DELL | -2.08%) fell on weaker forward guidance, while Regeneron (REGN | -19.0%) dropped sharply after mixed results in a late-stage drug trial.

Palantir (PLTR | + 7.73%) shares rose more than 7% and closed on the high of day with sharply increased volume.

Steel Stocks Soar on Tariff Boost

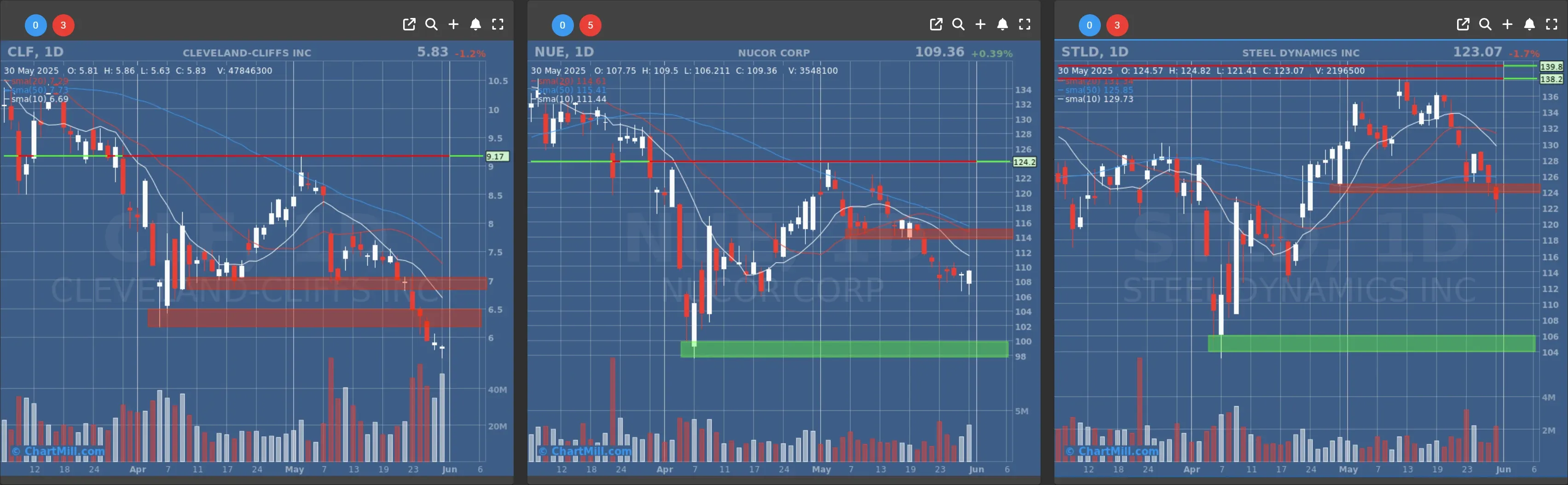

In a surprise late-Friday announcement, President Trump revealed that tariffs on imported steel and aluminum will double from 25% to 50% starting June 4. The move is intended to protect the domestic industry, especially after the recent US Steel deal with Nippon Steel.

The news sparked a rally in steel-related stocks. Cleveland-Cliffs (CLF | +33.44% after hours) soared in post-market trading, while Nucor (NUE | +13.39% after hours) and Steel Dynamics (STLD | +11.53% after hours) also jumped.

Looking Ahead

While the broader market has posted strong gains in May, the path forward remains uncertain. Investors will be closely watching how U.S.-China relations evolve, whether tariffs escalate further, and how inflation trends shape the Federal Reserve’s policy stance in the coming months.

The “TACO trade” may be back in full swing, but the long-term impact of trade policy remains far from settled.

Next to read: Market Monitor Trend Analysis & Breadth, June 02

7.6

+0.18 (+2.43%)

129.54

-1.89 (-1.44%)

128.01

-3.2 (-2.44%)

525

+4 (+0.77%)

24.55

+24.55 (+Infinity%)

467.82

+9.55 (+2.08%)

122.6

-1.39 (-1.12%)

77.4

+0.24 (+0.31%)

313.94

-1.38 (-0.44%)

136.32

+5.58 (+4.27%)

Find more stocks in the Stock Screener