QUALYS INC (NASDAQ:QLYS) emerged from our Peter Lynch-inspired screen as a stock with attractive growth potential at a reasonable valuation. The company, a provider of cloud security and compliance solutions, demonstrates solid financial health, profitability, and sustainable growth—key traits for long-term investors seeking quality at a fair price.

Why QLYS Fits the GARP Approach

- Strong Earnings Growth: Over the past five years, QUALYS has delivered an average annual EPS growth of 21.24%, well above the minimum 15% threshold in our screen. This indicates consistent and sustainable expansion.

- Healthy Profitability: The company boasts a Return on Equity (ROE) of 36.40%, far exceeding the 15% benchmark, reflecting efficient use of shareholder capital.

- Sound Financial Health: With zero debt and a current ratio of 1.37, QUALYS maintains a strong balance sheet, reducing risk for long-term holders.

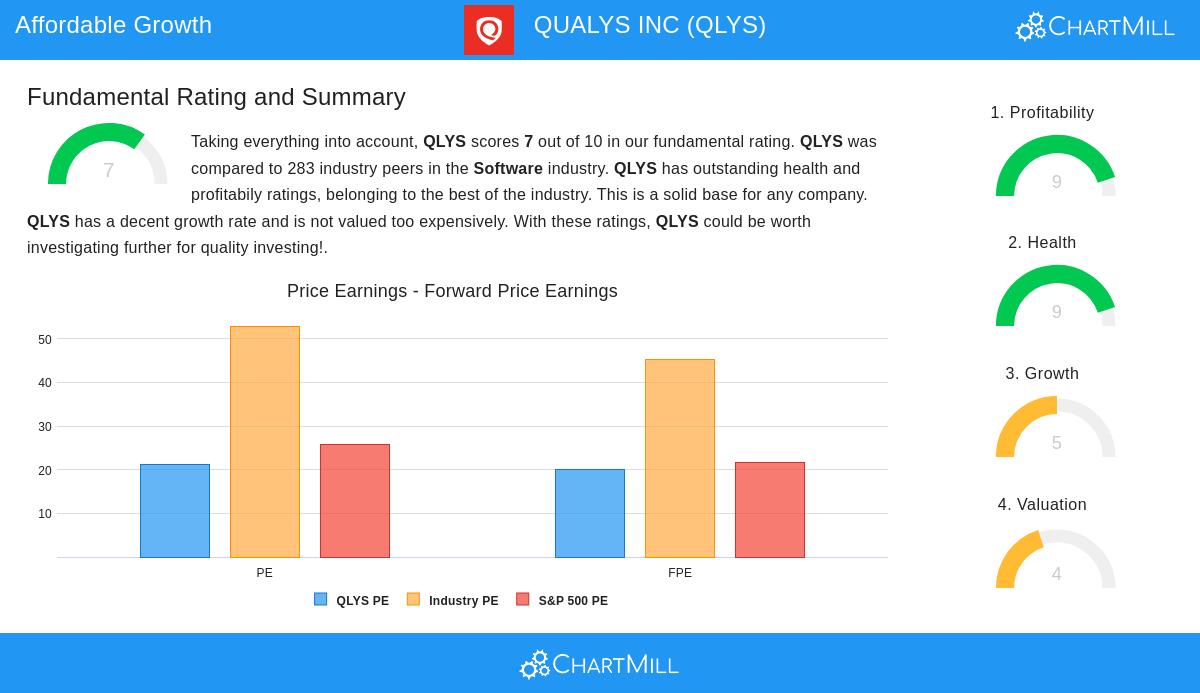

- Reasonable Valuation: While the PEG ratio based on past growth appears elevated at 6.32, the company’s high profitability and industry-leading margins (e.g., 81.65% gross margin) may justify a premium.

Fundamental Highlights

Our fundamental analysis report assigns QLYS a rating of 7 out of 10, citing excellent profitability and financial health. Key takeaways include:

- High Margins: Operating margin of 30.81% and profit margin of 28.59% rank in the top tier of the software industry.

- Efficient Capital Use: Return on Invested Capital (ROIC) stands at 28.78%, well above the cost of capital.

- Growth Consistency: Revenue has grown at 13.57% annually over the past five years, with positive cash flow throughout.

For investors aligned with Peter Lynch’s philosophy—focusing on understandable businesses with durable growth—QUALYS presents a compelling case.

Our Peter Lynch Strategy screener lists more stocks meeting these criteria and is updated regularly.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should always conduct your own analysis before making investment decisions.