QUALCOMM INC (NASDAQ:QCOM) stands out as a compelling candidate for investors seeking long-term growth at a reasonable price (GARP). The company, a leader in wireless technology, meets key criteria from Peter Lynch’s investment strategy, balancing solid growth, profitability, and an attractive valuation.

Why QCOM Fits the GARP Approach

- Sustainable Growth: QCOM has delivered a five-year average EPS growth of 23.5%, comfortably within Lynch’s preferred range of 15-30%. This indicates strong but manageable expansion.

- Reasonable Valuation: With a PEG ratio of 0.58 (well below Lynch’s threshold of 1), the stock appears undervalued relative to its growth prospects. The P/E ratio of 13.5 is also below industry and S&P 500 averages.

- Strong Profitability: The company boasts a return on equity (ROE) of 39.8%, far exceeding Lynch’s 15% benchmark, reflecting efficient use of shareholder capital.

- Healthy Balance Sheet: QCOM maintains a debt-to-equity ratio of 0.48, below the 0.6 limit Lynch favored, and a current ratio of 2.73, signaling ample liquidity.

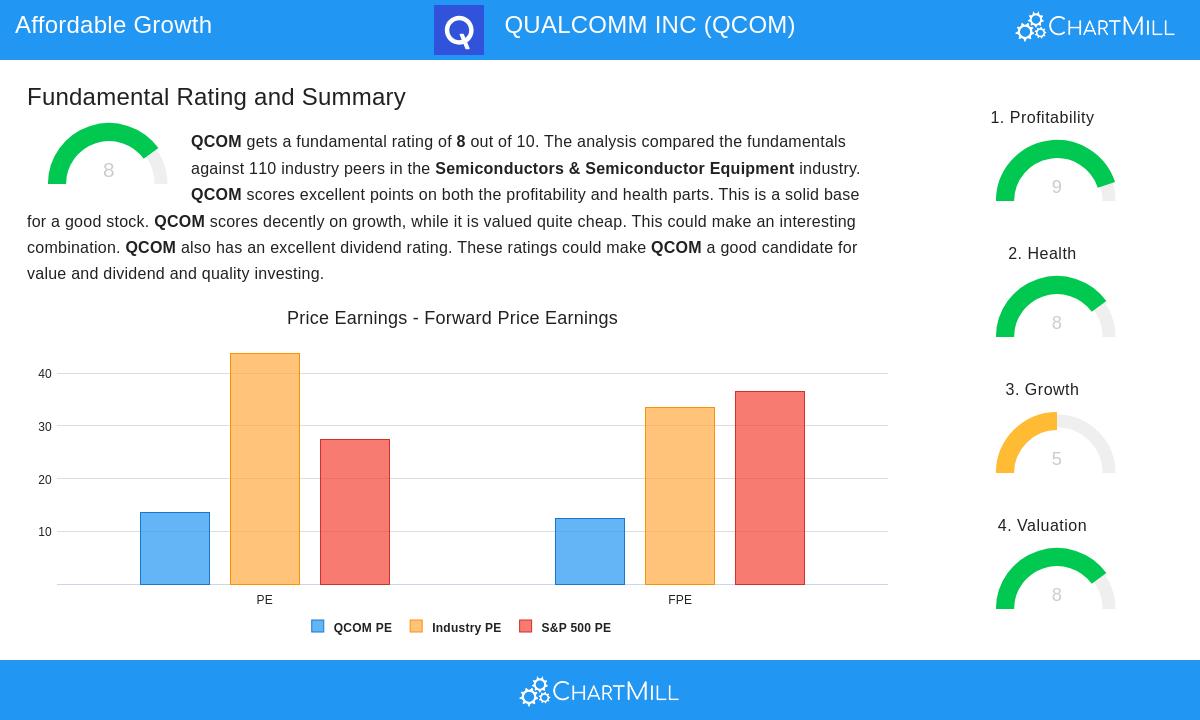

Fundamental Strength

Our fundamental analysis rates QCOM 8/10, highlighting its robust profitability, financial health, and dividend sustainability. Key takeaways:

- High Margins: Operating margins of 27.6% and gross margins of 55.7% outperform most peers.

- Dividend Reliability: A 2.2% yield with 10+ years of consistent payouts and a sustainable payout ratio.

- Efficient Capital Use: ROIC of 20.1% confirms effective reinvestment.

While future EPS growth is expected to slow to ~7%, QCOM’s established market position in 5G and IoT provides a durable growth runway.

For more stocks matching Peter Lynch’s criteria, explore our screener.

Disclaimer

This is not investing advice. Always conduct your own research before making investment decisions.