Pilgrim's Pride Corp (NASDAQ:PPC) was identified using a "Decent Value" screening strategy, which seeks out companies with strong fundamental valuation scores, typically above 7 on a 10-point scale, while also maintaining reasonable ratings in profitability, financial health, and growth. This approach aligns with core value investing principles, where investors look for securities trading below their intrinsic value without sacrificing operational strength or future potential. The goal is to find undervalued names that still exhibit fundamental quality, reducing the risk of value traps while positioning for potential price appreciation as the market corrects mispricings over time.

Valuation Metrics

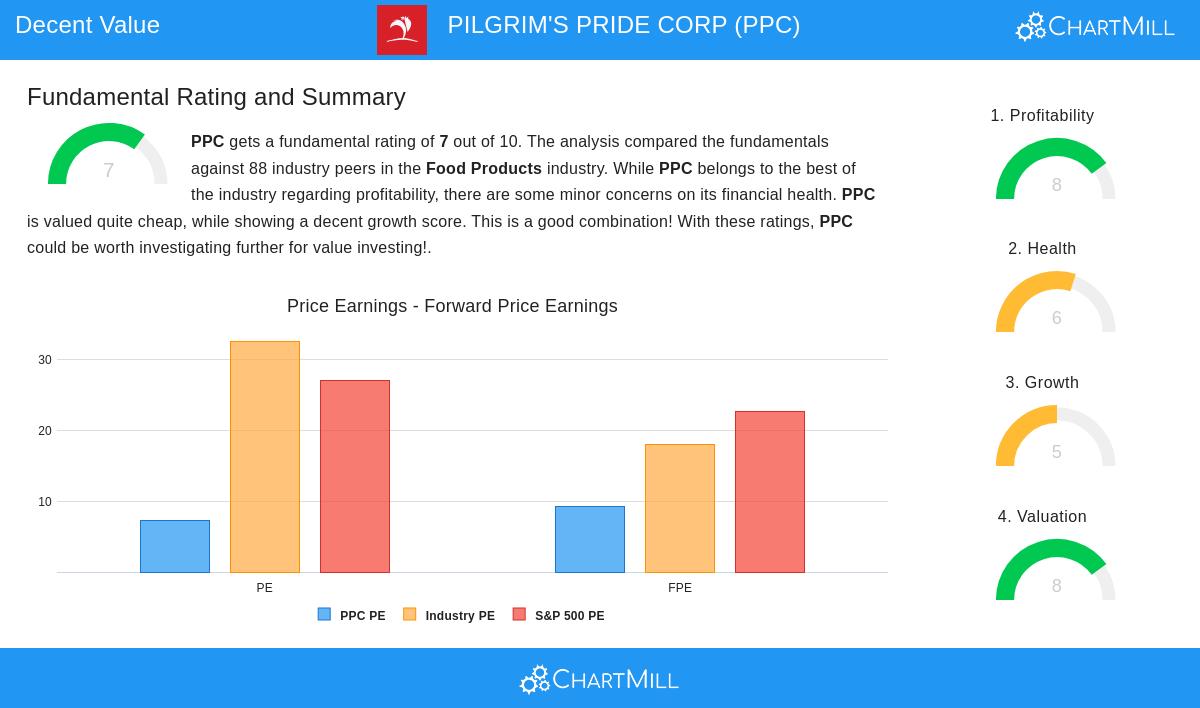

Pilgrim's Pride stands out immediately for its attractive valuation metrics, which are a central consideration for value investors seeking a margin of safety. According to the fundamental analysis report, the company’s valuation rating is a solid 8 out of 10, reflecting several strong figures:

- A Price/Earnings (P/E) ratio of 7.29, significantly below the industry average of 32.56 and the S&P 500 average of 27.07

- A Forward P/E of 9.28, also well beneath broader market and sector comparables

- An Enterprise Value to EBITDA multiple that places it cheaper than 82.95% of industry peers

- A favorable Price/Free Cash Flow ratio, outperforming 85.23% of companies in the food products sector

These metrics suggest the market may be undervaluing PPC relative to both its current earnings power and its industry, offering what value investors often describe as a “cheap entry point” for a company with sound operations.

Profitability Strength

Profitability is a key indicator of a company’s ability to generate returns, and it plays a critical role in value investing by signaling operational efficiency and competitive advantage. Pilgrim’s Pride earns a high profitability rating of 8, supported by:

- A Return on Equity (ROE) of 33.10%, outperforming 97.73% of industry competitors

- A Return on Invested Capital (ROIC) of 19.77%, ranking above 96.59% of peers

- A solid Profit Margin of 6.81%, better than 78.41% of companies in the sector

- Consistently positive earnings and operating cash flow over the past five years

These figures not only reflect efficient management and a strong market position but also reduce the risk that the low valuation is warranted by poor performance—a crucial check in the value investor’s process.

Financial Health

A company’s financial health determines its resilience during economic downturns and its capacity to sustain operations without excessive leverage—another vital filter for value investors who prioritize durability. PPC receives a health rating of 6, with notable strengths and some areas for caution:

- An Altman-Z score of 3.87, indicating low bankruptcy risk and outperforming 77.27% of the industry

- A manageable Debt to Free Cash Flow ratio of 2.83, suggesting the company can pay down debt relatively quickly

- A moderate Debt/Equity ratio of 0.83, though this is higher than 62.50% of industry peers

- A Current Ratio of 1.63, showing adequate short-term liquidity, though the Quick Ratio of 0.88 may warrant attention

Overall, the company appears financially stable with enough strength to manage market fluctuations, an important trait for investors focused on long-term value realization.

Growth Considerations

While growth is often secondary to valuation in pure value strategies, a baseline of growth can help ensure that the company is not in irreversible decline. PPC’s growth rating of 5 reflects mixed but acceptable trends:

- Strong historical EPS growth, averaging 27.16% annually over recent years

- Revenue growth of 9.40% per year over the same period, indicating expanding operations

- Expected decreases in future EPS growth, which may partly explain the discounted valuation

- A projected revenue growth rate of 1.59%, which, while modest, still suggests stability rather than contraction

For value investors, the historical growth provides confidence in the company’s ability to capitalize on opportunities, while the tempered future expectations help justify the current low multiples.

Conclusion

Pilgrim’s Pride Corp represents a strong case study in applied value investing principles, combining low valuation multiples with high profitability, reasonable financial health, and a track record of growth. These attributes align well with a strategy that seeks undervalued companies with fundamental strength, reducing the risk of a value trap while positioning for potential market reassessment.

For investors interested in exploring similar opportunities, more screened results based on these criteria can be found using this Decent Value Stocks screen.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consider their financial situation and risk tolerance before making any investment decisions.