PILGRIM'S PRIDE CORP (NASDAQ:PPC) was identified as a decent value stock by our stock screener. The company shows strong profitability and financial health while trading at an attractive valuation. Below, we examine why PPC stands out as a potential opportunity for value investors.

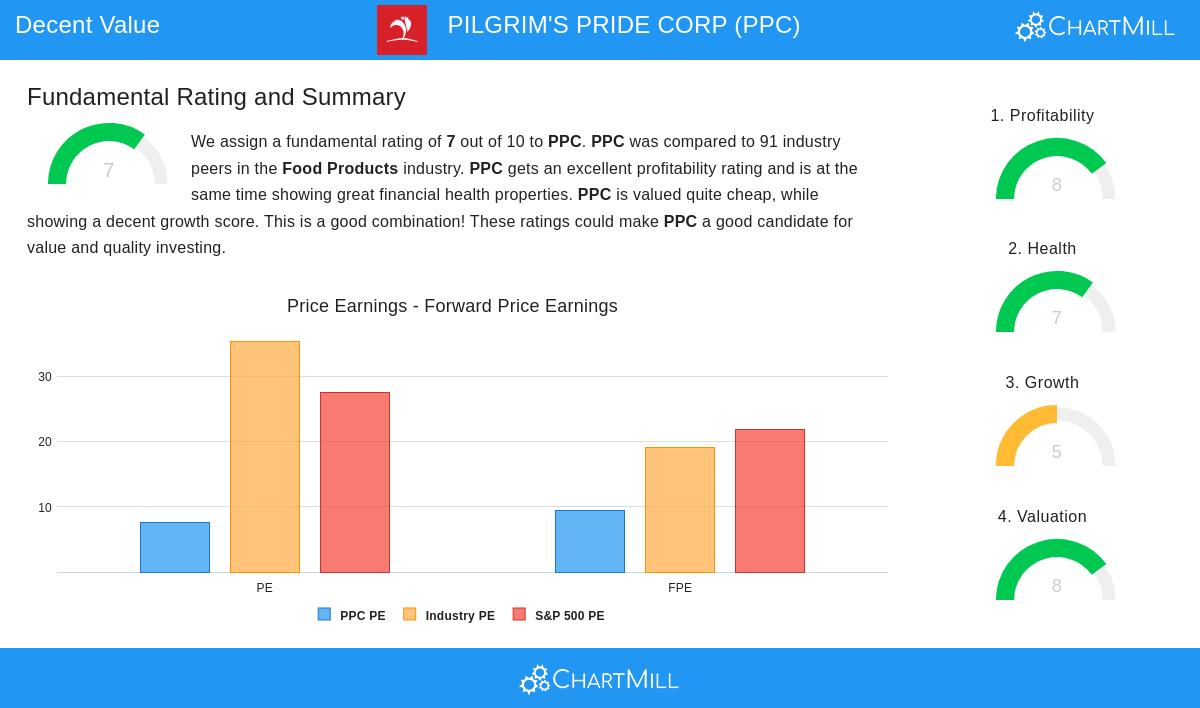

Valuation

PPC’s valuation metrics suggest the stock is priced attractively compared to peers and the broader market:

- P/E Ratio of 7.60 – Well below the industry average of 35.35 and the S&P 500’s 27.41.

- Forward P/E of 9.36 – Also favorable compared to sector and market benchmarks.

- Enterprise Value/EBITDA and Price/Free Cash Flow – Both ratios indicate PPC is cheaper than most industry competitors.

Despite a high PEG ratio, which suggests limited earnings growth ahead, the company’s strong profitability justifies the current valuation.

Profitability

PPC earns high marks for profitability, with key strengths including:

- Return on Equity (ROE) of 38.56% – Among the best in its industry.

- Return on Invested Capital (ROIC) of 20.80% – Significantly above its cost of capital, indicating efficient use of resources.

- Improving Margins – Both operating and profit margins have expanded in recent years.

Financial Health

The company maintains a solid financial position:

- Altman-Z Score of 3.39 – Suggests low bankruptcy risk.

- Debt Management – While the debt-to-equity ratio is elevated at 1.02, the company’s strong cash flow generation helps mitigate concerns.

- Liquidity – Current and quick ratios are in line with industry standards, though investors should monitor working capital trends.

Growth

While future growth expectations are modest, PPC has delivered strong historical performance:

- EPS Growth (Past Year): 150.42% – A standout figure, though partly due to cyclical factors.

- Revenue Growth (5-Year Avg.): 9.40% – Demonstrates consistent top-line expansion.

- Forward Outlook – Analysts project a slight decline in earnings but stable revenue growth.

For a deeper analysis, review the full fundamental report for PPC.

Our Decent Value Stock Screener lists more stocks with strong valuations and fundamentals, updated daily.

Disclaimer

This is not investment advice. The observations here are based on data available at the time of writing. Always conduct your own research before making investment decisions.