PILGRIM'S PRIDE CORP (NASDAQ:PPC) stands out as a potential opportunity for value investors, according to our fundamental screening criteria. The company, a major player in poultry and pork processing, combines strong profitability and financial health with an attractive valuation.

Valuation

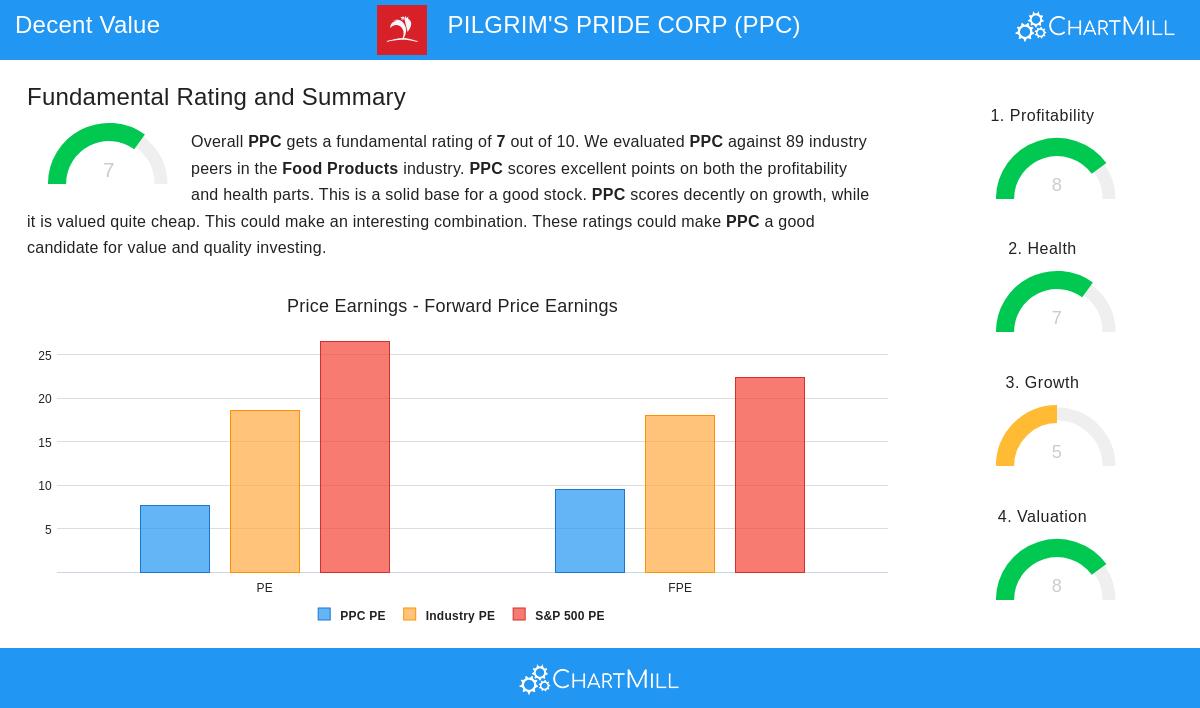

PPC appears undervalued based on key metrics:

- Price/Earnings (P/E) ratio of 7.61, well below the industry average of 18.65 and the S&P 500 average of 26.59.

- Price/Forward Earnings ratio of 9.46, indicating a reasonable outlook compared to peers.

- Enterprise Value to EBITDA and Price/Free Cash Flow ratios suggest PPC is cheaper than 85% to 92% of its industry competitors.

Profitability

The company demonstrates strong earnings power:

- Return on Equity (ROE) of 38.56%, outperforming nearly 99% of industry peers.

- Return on Invested Capital (ROIC) of 20.80%, well above the cost of capital.

- Profit Margin of 6.72%, placing it in the top quartile of its sector.

Financial Health

PPC maintains a solid balance sheet:

- Altman-Z score of 3.39, indicating low bankruptcy risk.

- Debt to Free Cash Flow ratio of 2.32, showing manageable leverage.

- While the Debt/Equity ratio of 1.02 is higher than some peers, the company’s strong cash flow mitigates concerns.

Growth

Recent performance shows mixed but promising trends:

- EPS growth of 150.42% over the past year, with a 5-year average annual growth of 27.16%.

- Revenue growth of 9.40% annually over the past five years, though near-term projections suggest slower expansion.

Dividend

PPC offers a dividend yield of 13.41%, significantly higher than both industry (4.66%) and S&P 500 (2.39%) averages. However, the company has a limited dividend history, which may warrant caution.

For a deeper look, review the full fundamental analysis report for PPC.

Our Decent Value Stocks screener lists more stocks with similar characteristics and is updated regularly.

Disclaimer

This is not investment advice. Always conduct your own research before making investment decisions.