Investors looking for growth chances at sensible prices often consider methods that mix expansion possibility with careful financial management. The "Affordable Growth" method focuses on companies showing solid growth paths while keeping good profitability and financial condition, all without requiring high price tags. This process works to find businesses that join effective operations with lasting growth, possibly presenting good returns for the risk taken. One firm currently matching this description is Insulet Corp (NASDAQ:PODD), a medical device maker that focuses on insulin delivery systems.

Growth Path

Insulet shows very good growth qualities that build the base of its appeal to investors. The firm's recent results show solid movement in important financial areas. Sales growth has been notable, with a 25.99% rise over the last year and a five-year average growth of 22.92%. This growth is moving successfully to profits, as shown by earnings per share growth of 24.78% per year. For the future, analysts predict ongoing solid results with estimated EPS growth of 24.27% and sales growth of 17.30% each year. While these future estimates show a slowdown from past rates, they still place Insulet much higher than industry averages and back the firm's above-average valuation.

- Revenue growth (past year): 25.99%

- Five-year average revenue growth: 22.92%

- EPS growth (past year): 24.78%

- Expected annual EPS growth: 24.27%

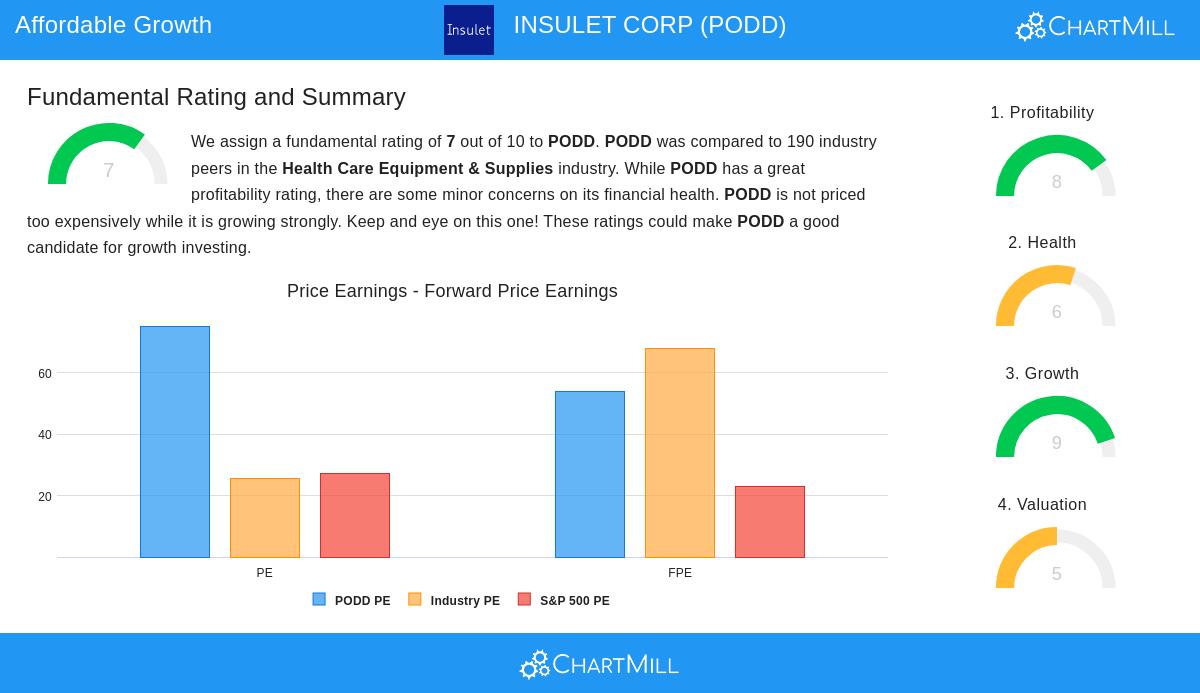

Valuation Picture

The valuation view for Insulet tells a detailed story that fits with the affordable growth idea. While common measures like the Price/Earnings ratio of 75.18 seem high next to the wider market, the full situation is important. Compared to others in the Health Care Equipment & Supplies industry, Insulet has a lower price, with 64.74% of similar firms having higher P/E ratios. More future-focused measures give more insight - the Price/Forward Earnings ratio of 53.98 is lower than 67.89% of industry firms. The Enterprise Value to EBITDA and Price/Free Cash Flow ratios also point to a sensible valuation in the sector. Most significantly, the PEG ratio, which changes the P/E for growth estimates, shows the current price may be acceptable given the company's solid growth possibilities.

- P/E ratio: 75.18 (lower than 64.74% of industry peers)

- Forward P/E: 53.98 (lower than 67.89% of the industry)

- PEG ratio shows acceptable growth compensation

Profitability and Financial Condition

Beyond growth and valuation, Insulet shows effective operational performance that supports the investment case. Profitability measures are especially strong, with the firm doing better than most industry rivals. The Return on Invested Capital of 13.08% is better than 93% of similar companies, showing good use of capital. Margins present a comparable story - the 70.74% gross margin, 17.26% operating margin, and 10.01% profit margin are all in the top group of the industry. These good profitability numbers help explain the firm's above-average valuation and point to lasting business economics.

Financial condition shows a varied but generally satisfactory view. The Altman-Z score of 8.36 shows very low bankruptcy danger and is better than 90% of industry firms. Liquidity measures seem acceptable with a current ratio of 2.26. However, the debt-to-equity ratio of 0.64 is higher than 69% of rivals, marking an area to watch. Overall, the company's financial standing allows for continued investment in growth without creating major solvency worries.

- Return on Invested Capital: 13.08% (top 7% of industry)

- Profit Margin: 10.01% (top 18% of industry)

- Altman-Z score: 8.36 (very low bankruptcy risk)

- Debt-to-Equity: 0.64 (higher than industry median)

Investment Points

For investors using an affordable growth method, Insulet is an interesting example of weighing growth possibility against valuation factors. The company's very good growth rates and strong profitability give fundamental support for its market price, especially when seen through an industry-specific view. The acceptable financial condition score suggests some care with debt, but not at levels that would usually rule out a growth option. The lack of a dividend is normal for a firm putting money back into expansion chances.

The full fundamental study available through ChartMill's detailed report gives more information for investors doing more research. This kind of organized study helps put valuation measures in the context of industry standards and growth estimates, which is important for finding reasonably priced growth chances.

Investors curious about finding similar companies that meet affordable growth standards can look at more screening results using the Affordable Growth Stock Screener. This tool allows for changes based on specific growth, valuation, profitability, and condition settings to find potential investments that match personal risk tastes and return goals.

Disclaimer: This analysis is based on fundamental data and ratings provided by ChartMill.com and is for informational purposes only. It does not constitute investment advice, a recommendation to buy or sell any security, or an offer to participate in any investment strategy. Investors should conduct their own research and consult with a qualified financial advisor before making investment decisions.