Growth investing often focuses on companies with strong revenue and earnings expansion, but valuations can sometimes reach levels that are hard to justify. The "Affordable Growth" strategy balances these factors by finding stocks with good growth potential while keeping valuations reasonable, backed by solid profitability and financial strength. This method helps investors avoid paying too much for growth while still benefiting from companies set for long-term success.

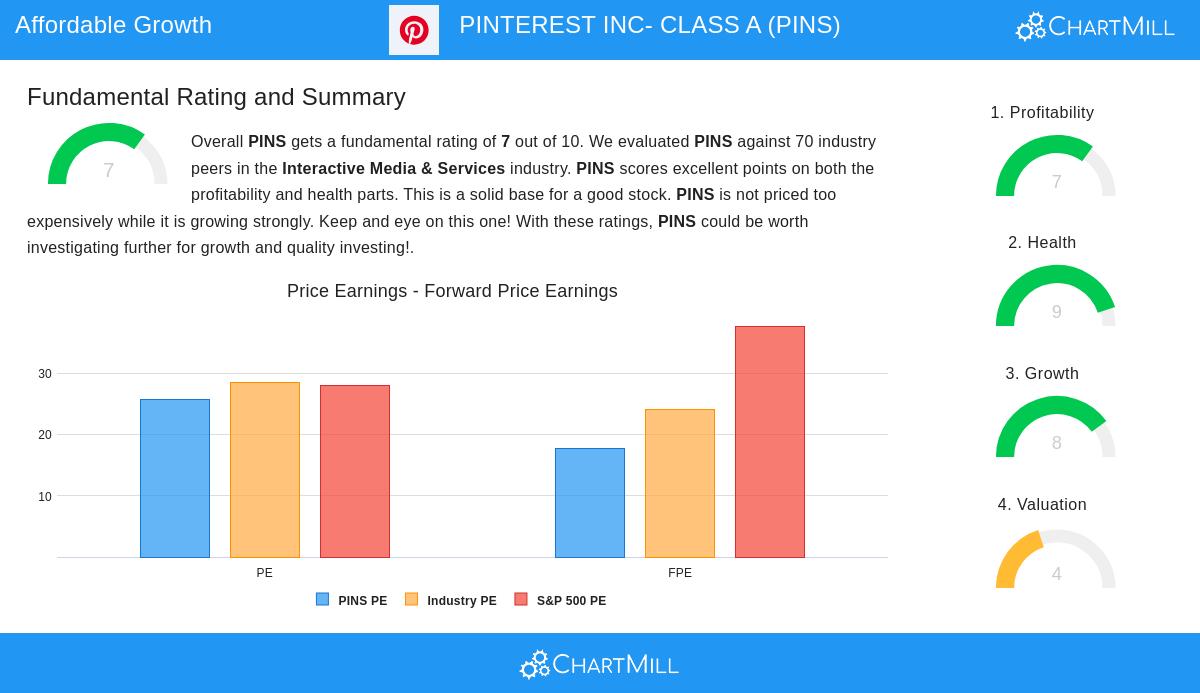

PINTEREST INC-CLASS A (NYSE:PINS) aligns with this strategy, as shown in its fundamental analysis report. The stock has an overall rating of 7 out of 10, with high scores in growth (8/10) and financial health (9/10), along with decent profitability (7/10) and a fair valuation (5/10).

Growth: A Key Factor

The company’s growth metrics are impressive, with revenue rising by 17.81% year-over-year and a five-year average revenue growth rate of 26.12%. Earnings per share (EPS) have also grown by 21.31% over the past year, with an annualized five-year growth rate of 8.67%. Forward estimates indicate continued progress, with EPS expected to grow at 18.63% annually and revenue at 14.34%. This upward trend places Pinterest well within the Interactive Media & Services industry.

Valuation: Fair for the Growth Potential

While Pinterest is not inexpensive in absolute terms, trading at a P/E ratio of 25.61, its valuation seems reasonable given its growth outlook:

- Its forward P/E of 17.73 is below the S&P 500 average (37.67) and lower than 67% of industry peers.

- The PEG ratio, which considers earnings growth, suggests the stock is fairly priced, especially with its strong profitability margins.

- Unlike many growth stocks, Pinterest has no debt, lowering financial risk and supporting its valuation.

Profitability and Financial Health: A Solid Base

Profitability is another strong point, with a 50.41% gross margin (better than 74% of peers) and a net margin of 5.28%. The company’s return on equity (ROE) of 40.44% ranks in the top 2% of its industry, showing efficient use of capital. Financially, Pinterest is in excellent shape, with a current ratio of 8.41 (indicating strong liquidity) and no debt, earning it a near-perfect health rating of 9/10.

Why These Criteria Matter for Affordable Growth

The strategy favors companies like Pinterest because:

- Growth supports future earnings potential.

- Fair valuation limits exposure to overvalued stocks.

- Strong profitability and health reduce risk during market declines.

For a closer look at Pinterest’s fundamentals, see the full analysis here.

Finding More Affordable Growth Options

Pinterest is one example of a stock that fits the Affordable Growth criteria. Investors looking for similar opportunities can use the predefined screen to find other stocks with good growth, fair valuations, and strong fundamentals.

Disclaimer: This article is not investment advice. Always conduct your own research or consult a financial advisor before making investment decisions.