The Caviar Cruise stock screening method represents a systematic way to identify quality investments, focusing on companies with lasting competitive strengths, sound financial condition, and steady expansion. This approach, based on Luc Kroeze's "The Caviar Formula," stresses long-term ownership of businesses with excellent operational traits instead of short-term trading chances. The method uses strict quantitative filters to find companies with established sales and profit expansion, high returns on capital put to work, acceptable debt, and good earnings that turn into free cash flow.

PAYCOM SOFTWARE INC (NYSE:PAYC) appears as a strong candidate from this screening process, showing several traits that fit with quality investment ideas. The Oklahoma City-based company providing online human capital management solutions presents a profile that satisfies the strict needs of the Caviar Cruise method.

Financial Performance Measurements

The company's past results indicate solid operational performance in several areas:

- Sales expansion (5Y CAGR): 8.57%

- EBIT expansion (5Y CAGR): 22.90%

- Return on Invested Capital (excluding cash, goodwill, intangibles): 26.50%

- Debt to Free Cash Flow ratio: 0.0

- Profit Quality (5-year average): 84.82%

These numbers show that Paycom not only meets but also goes beyond the minimum requirements of the Caviar Cruise screen, especially in EBIT expansion and return measurements. The large EBIT expansion rate exceeding sales expansion points to better operational efficiency and possible pricing strength, both important signs of quality businesses.

Profitability and Efficiency

Paycom's operational strength is seen in its margin results and capital use effectiveness. The company reaches a notable profit margin of 21.21% and operating margin of 28.10%, putting it in the highest group of its industry competitors. More significantly, these margins have improved over recent years, suggesting continuing operational improvements. The 26.50% return on invested capital is much higher than the 15% level needed by the Caviar Cruise method, showing outstanding capital use effectiveness and a strong competitive position in the professional services field.

The company's profit quality score of 84.82% shows its capability to turn accounting profits into real cash flow, a key factor for quality investors who value lasting financial results over accounting numbers alone. This conversion rate is well above the 75% level set in the screening rules.

Financial Condition and Stability

Paycom's balance sheet strength gives more assurance for long-term investors. The company functions with no debt, leading to a debt-to-free-cash-flow ratio of zero. This absence of debt removes interest rate concerns and offers important financial options for handling economic slowdowns or chasing strategic possibilities. The Altman-Z score of 4.95 shows very low bankruptcy risk and does better than 83.72% of industry competitors, further supporting the company's financial steadiness.

Expansion Path and Future Outlook

While past results build the base for quality investing, future outlooks stay important points to think about. Paycom shows solid expansion momentum with experts forecasting:

- Earnings per share expansion: 12.55% each year

- Sales expansion: 8.57% each year

Even though these forecasted expansion rates show a slowdown from past levels, they remain large and match the method's need for lasting business growth. The company's place in the increasing human capital management software market, together with its online delivery model, provides structural expansion supports that help continued growth.

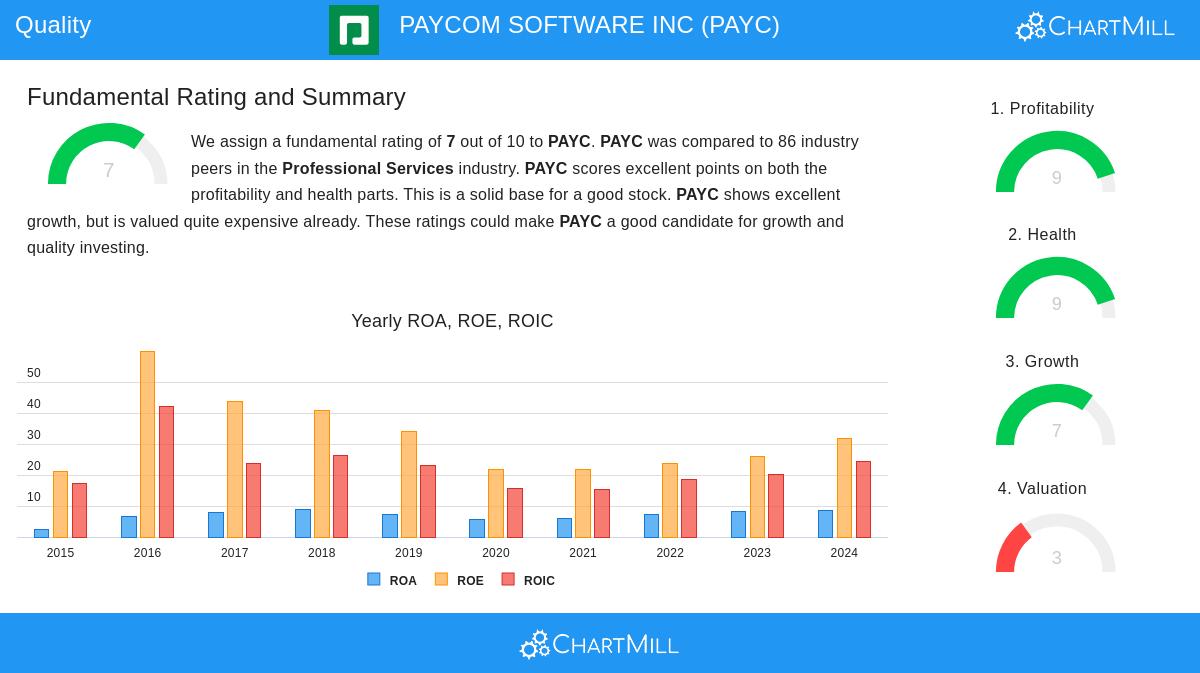

Complete Fundamental Evaluation

According to the detailed fundamental analysis report, Paycom gets an overall rating of 7 out of 10, with especially high marks in profitability (9/10) and financial condition (9/10). The company does very well in several fundamental areas while showing some price premium that might be acceptable given its quality traits. The report mentions that Paycom's mix of great profitability, sound financial condition, and good expansion makes it fitting for quality and growth investment methods.

Valuation Points

While the Caviar Cruise method does not include strict price filters, quality investors must still think about price compared to business basics. Paycom trades at a price-to-earnings ratio of 23.37, which seems fair compared to both industry averages and the S&P 500. The PEG ratio, which changes the P/E for expansion, indicates a suitable price given the company's expansion outlook and quality traits.

For investors wanting to look at more companies that fit the Caviar Cruise rules, the full screening results offer a wider group of possible quality investments.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice, recommendation, or endorsement of any security. Investors should conduct their own research and consult with financial advisors before making investment decisions. Past performance does not guarantee future results.