Investors looking for growth opportunities at fair prices often consider strategies such as Growth At Reasonable Price (GARP) or "Affordable Growth" screening. This method focuses on companies with promising growth, steady profitability, and sound financials, while steering clear of overvalued stocks. The aim is to find businesses capable of sustained earnings growth without the need to pay excessive premiums. One stock that meets these standards is UNIVERSAL DISPLAY CORP (NASDAQ:OLED), a key player in organic light-emitting diode (OLED) technologies.

Why UNIVERSAL DISPLAY CORP Matches the Affordable Growth Approach

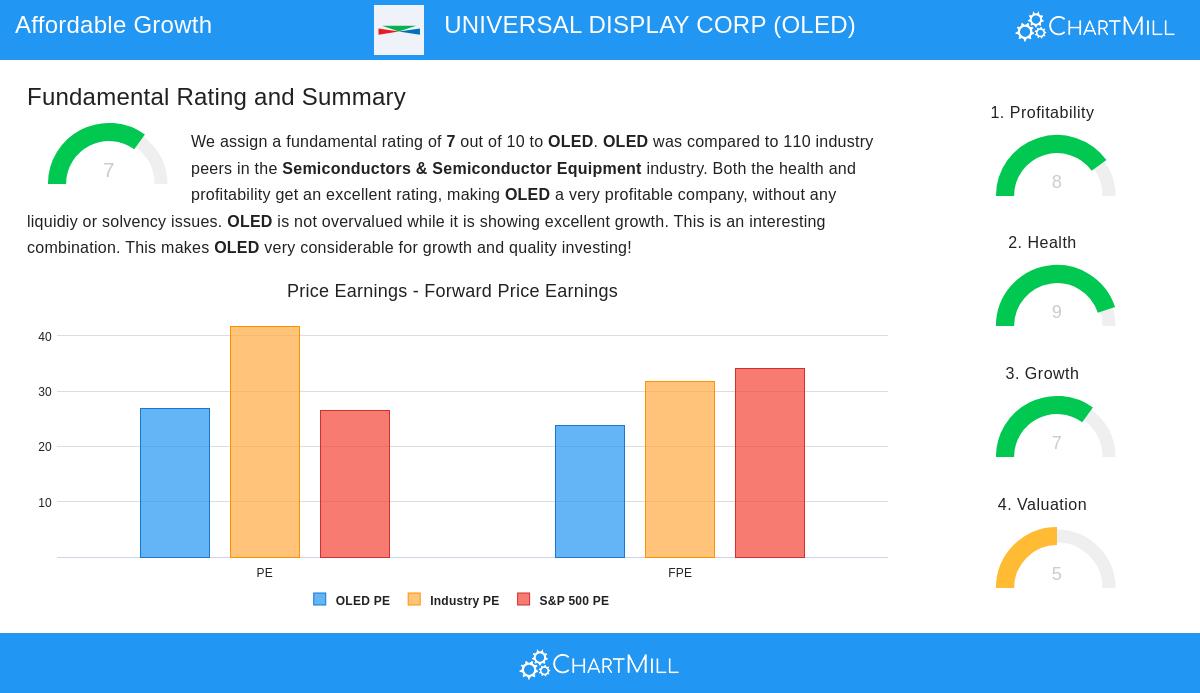

1. Solid Growth Potential

The company holds a Growth Rating of 7/10, indicating both past and future expansion. Key points from the fundamental analysis report include:

- Earnings Per Share (EPS) Growth: OLED has achieved a 9.75% annualized EPS growth over recent years, with analysts predicting a rise to 20.56% yearly growth in the near term.

- Revenue Trends: While revenue fell -16.04% last year, the long-term outlook stays positive, with a 9.83% annual revenue growth rate historically and an anticipated 17.10% increase ahead.

- Improving Momentum: Both EPS and revenue growth rates are expected to climb, indicating the company is entering a more dynamic phase.

For GARP investors, this mix of historical performance and upward growth revisions is essential—it shows the company is growing in a sustainable way.

2. Fair Valuation

OLED’s Valuation Rating of 5/10 suggests it is priced reasonably compared to its growth prospects, avoiding the high premiums common in many tech stocks. Key valuation measures include:

- P/E Ratio (26.88): Slightly higher than the S&P 500 average (26.48) but more affordable than 67% of industry peers in semiconductors.

- Forward P/E (23.72): Lower than the S&P 500’s 34.04, implying the market has not overestimated expectations.

- Price/Free Cash Flow: OLED is priced below 64.55% of its industry, further highlighting its fair value.

The balanced valuation, combined with solid growth, makes OLED an attractive option for investors seeking tech exposure without overpaying.

3. Profitability and Financial Stability

While growth and valuation are central to the Affordable Growth strategy, profitability and financial strength are equally vital—OLED performs well here:

- Profitability (8/10): The company maintains high margins, including a 77.19% gross margin (better than 96% of peers) and a 38.93% operating margin.

- Financial Health (9/10): OLED carries no debt, with a current ratio of 8.05 and a quick ratio of 6.39, placing it among the most financially secure firms.

These strengths lower risk and reinforce the idea that OLED’s growth is sustainable, not driven by debt or unstable earnings.

Conclusion

UNIVERSAL DISPLAY CORP fits the Affordable Growth strategy well, providing a mix of strong growth, fair valuation, and solid fundamentals. Its role in the OLED market—a sector with long-term potential from displays, AR/VR, and automotive uses—enhances its appeal.

For investors seeking more stocks that meet similar criteria, the Affordable Growth screener offers additional options.

Disclaimer: This article is not investment advice. Always conduct your own research or consult a financial advisor before making investment decisions.