In the search for dependable income from stocks, many investors choose dividend-focused methods that look for not only high yields, but also the durability and quality of those payments. One typical method uses filters for companies with good dividend scores, sound profitability, and acceptable financial condition, criteria meant to find businesses able to keep and increase their dividends over time. This technique helps sidestep the dangers of high-yield traps, where unmaintainable payments might point to fundamental business problems. Altria Group Inc (NYSE:MO) recently appeared from this type of filtering process, matching well with these careful measures.

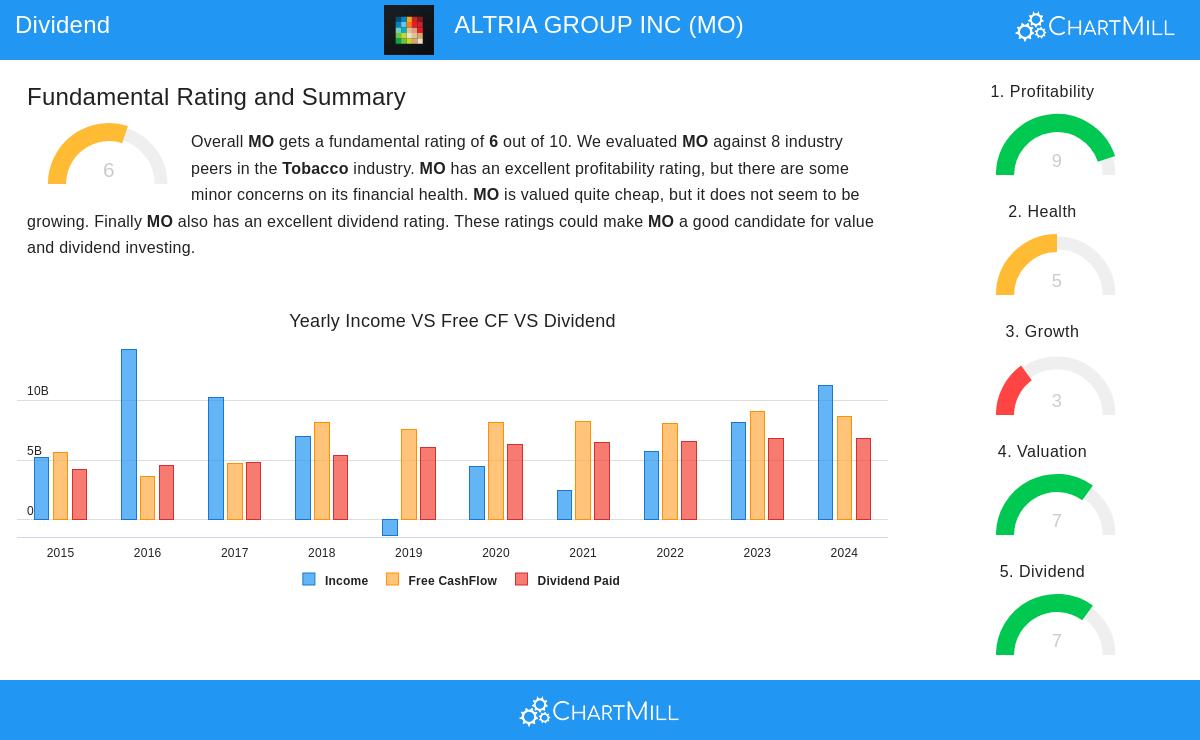

A closer examination of Altria’s fundamental profile shows why it is notable for dividend-focused portfolios. The company’s dividend numbers are especially noteworthy: it now provides a yield of 6.38%, much higher than the industry average of 3.72% and the S&P 500’s average of about 2.32%. Most significantly, Altria has built a record of consistency, having paid dividends without interruption for more than ten years and without a cut. This past performance of reliable payments is a foundation of dividend investing, as it shows a corporate dedication to giving capital back to shareholders.

However, yield and history by themselves are not enough. Durability is vital, and here Altria shows a varied but controllable situation. The payout ratio is at 78.52%, which is high and indicates that a big part of earnings is used for dividends. While this is above the preferred level for some cautious investors, it is balanced by the company’s very strong profitability. Altria’s return on invested capital (ROIC) of 37.1% and profit margins over 37% are some of the top in its sector, showing efficient use of capital and solid earnings ability. High profitability offers an important cushion, allowing the company to maintain its dividend even with a higher payout ratio.

Financial condition, another important filter standard, is sufficient though not perfect. Altria’s solvency is good, with an Altman-Z score showing low bankruptcy risk and an acceptable debt-to-free-cash-flow ratio. However, liquidity measures like the current and quick ratios are lower than industry standards, which needs observation. Even so, the total health score stays satisfactory, backed by the firm’s steady cash flows and history of careful capital management.

Growth expectations for Altria are moderate, with revenue patterns showing small decline and earnings growth expected in the low single digits. This is typical in established sectors, but it highlights the need for dividend durability over fast price increases in this kind of investment. For income-focused investors, the mix of high yield, tested dividend reliability, strong profitability, and adequate financial condition forms a convincing argument.

For those wanting to investigate other businesses that fit similar standards, more outcomes from this dividend filter are available here.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consider their financial situation and risk tolerance before making investment decisions.